A moment of truth for cryptocurrencies

20th April 2020 |

We have a special bumper edition of Coin Confidential today. Last week’s edition was delayed due to some technical hitches caused by the lockdown. We’re back on track, to help you understand what could be an historic time for cryptocurrency in the coming weeks.

Will the $12 trillion “global stimulus” make or break bitcoin?

I saw an interesting tweet the other day, showing that governments have injected $12 trillion into the global economy since the start of the coronapocalypse.

Source: Twitter

I don’t know about you, but when I hear numbers over a few thousand, I find it hard to comprehend them.

So a couple of years ago, I decided to try think of a way to make big numbers seem more real.

I basically translated them into distance. And when you do that, you realise just how impossibly massive 1 trillion is. Let alone 12 trillion.

So let’s take a look at that, and then think about what this impossibly large amount of stimulus means for crypto… or any investment you may hold going forward.

Here’s how I visualised it back in 2018 (writing in Exponential Investor about… aliens):

Picture a pound coin, one of the round ones. Not the new angular one.

Got it? Good.

Now picture 100 £1 coins lying end to end.

How long would that line be?

It would be a little over two metres long. I’m guessing you got that roughly right.

Now try 1,000 £1 coins. It’s harder, isn’t it? But not impossible.

A line of 1,000 £1 coins would be 22.5 metres long.

This is where our concept of numbers really starts to fall away. Much over this, and our minds just don’t know what to do.

Let’s try a £1 million line. That would be 22.5km long – a little over a half marathon.

The difference between 1 million and 1 billion is colossal. But because our brains find it hard to conceptualise either, we can’t really grasp just how much bigger 1 billion is than 1 million.

1 billion £1 coins would reach from London to New York and back, twice.

And the difference between 1 billion and 1 trillion? On paper, it doesn’t look like much. But in reality, it is…

A line of 1 trillion £1 coins would be 22.5 million km long.

We’ve now hit the point where we can’t even comprehend the distance, let alone the number of coins.

If you split that 1 trillion £1 coin line into 58 smaller lines, each line would reach to the moon.

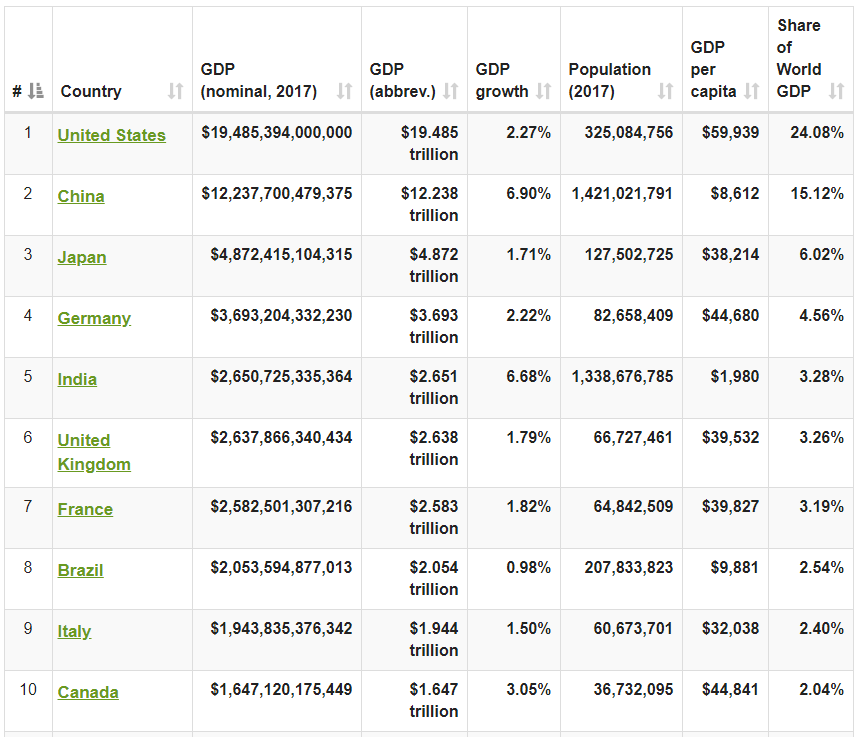

Or to put it another, less fun, way, $12 trillion is the equivalent of China’s entire economy, which is the second biggest on the planet.

Source: Worldometer

And that’s how much money was just injected into the global economy in the space of one month.

With millions upon millions of people now unemployed thanks to the worldwide lockdown, governments need to create money out of thin air.

If they don’t, the entire system will grind to a halt and their citizens will be forced to steal what they need to survive.

It would be a full-on dystopian nightmare.

And as much as the “preppers” may say they want that, the reality would be no fun for anyone. Not even them. I mean, have you seen or read The Road?

This time round, will it just be the banks who win again, or will ordinary people benefit too?

Now, if you remember the good ol’ 2008 financial crisis, you’ll no doubt remember the massive money printing and bank bailouts that came with it.

“Too big to fail” became a catchphrase in the wake of that era.

And many people got sick of it.

Why should the banks and the corrupt people that run them be bailed out of the mess they created?

Simple: they were too big to fail.

Ordinary people would have to shoulder the burden of bailing out the banks for generations.

Meanwhile, the banks – buoyed by billions in taxpayers’ money – bounced back fast. And pretty soon it was business as usual for them.

As the Guardian wrote back in March 2019:

While helping keep borrowing costs low, low rates and QE drove up asset prices. As well as the anniversary of the rate cut, this week also marks 10 years since the FTSE 100 hit its post-financial crisis nadir of 3,512, before going on one of the biggest bull runs in history, doubling to more than 7,000.

Wealth inequality has soared. The least wealthy 10% of households saw their real wealth rise by £3,000 between 2006-08 and 2012-14, versus £350,000 in gains for the wealthiest 10%.

…

Blanchflower, who will publish a book this summer, Where Have All the Good Jobs Gone?, on the cost of the policy reaction to the crash, said: “It made people think: ‘Those bastards, they got rescued.’ The banks raised asset prices and the stocks that fell suddenly came back up. If I don’t have assets, what’s happened is I’m pissed off.”

Was it fair?

No. But what could any ordinary person do about it?

(Spoiler alert: it starts with “bit” and ends in “coin”, as you’ll see in just a minute.)

This time around, sentiment is entirely different.

There have been numerous calls for “QE for the people” not for the banks.

I covered this briefly back in March. And since then, more money has been promised to the people… most of it in the form of loans.

But as City AM reported on 7 April, those loans aren’t reaching over 99% of businesses that need them:

Just 2,022 loans have been made to the UK’s small and medium-sized firms through the government’s coronavirus business lending scheme.

There have been around 300,000 applications so far. That means a paltry 0.65 per cent of enquiries have resulted in coronavirus business loans.

And over in the US, things aren’t any better, with The Hill reporting on 3 April that 24% of small businesses expect to close permanently within the next two months.

Just think about that for a second. A quarter of small businesses will soon be gone forever.

What kind of knock-on effect is that going to have on our lives going forward?

The entire situation is perfectly summed up by this screengrab that’s been doing the rounds this week:

Source: CNBC, Mad Money

Is that screengrab real? I would probably say no, given you can’t see the channel’s branding in it anywhere. However, what it’s saying is factually correct. So it may well be.

The Dow Jones Industrial Average did just have its best week since 1938 (source: CNN).

And more than 16 million Americans have filed for unemployment in the last three weeks (source: The Guardian).

Looking into it all a little more deeply, we can see the main reason the Dow (and other stockmarkets) are up recently is largely because of a $2.3 trillion relief package the US government signed in at the end of March.

Reuters reports, among other things, the package:

- Gives direct payments of up to $1,200 to Americans earning $99,000 or less, with additional payments of $500 per child.

- Increases unemployment payments by $600 per week for up to four months.

- Writes off loans to small businesses.

- Creates a $4.5 trillion loan package to big businesses…

(Companies tapping the fund would not be able to engage in stock buybacks and would have to retain at least 90% of their employees through the end of September. They would not be able to boost executive pay by more than $425,000 annually, and those earning more than $3 million a year would see their salaries reduced.) - Creates grants for airlines – possibly in return for equity.

- Gives: $100 billion to hospitals and healthcare, $150 billion to state and local governments, $45 billion in disaster relief, $32 billion for education, $25 billion for transport, $10 billion to the post, $1billion to rail and $10 billion to airports.

- Cuts $4 billion in airline ticket, cargo and fuel taxes.

- Cuts 50% of payroll tax.

- Gives $25 billion more for food stamps.

- Gives $12 billion more to housing programs.

- And gives $5 billion more to child and family services.

So, it seems this time around, real people are getting relief, too.

But the big question is, how will this all play out in six, 12 or 24 months’ time?

Will it be more of the same with ordinary people ending up in a worse position than before the lockdown and banks and institutions doing great?

And if it does, will people put up with it this time around?

Or will things turn out differently?

This is the entire reason for bitcoin’s existence

The last time the world went into a global recession, we saw the creation of bitcoin.

Many people believe bitcoin was created as a direct response to the failings of the financial system.

After all, its first transaction had this headline written into its code: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.”

This was no accident, they say.

It was a statement of intent.

Bitcoin was designed to give power back to the individual and take it away from the central authorities.

As I said in my What is DeFi feature:

The idea you don’t need to rely on a central authority to make things work – be they financial transactions, data transactions, contracts, proof of ownership, proof of identity… anything – is what crypto is all about.

To go back to basics, bitcoin allows two people to exchange money without the need to trust each other.

In traditional finance, you need to either trust the person you’re exchanging money with, or you need to trust in a central authority to oversee the transaction.

For example, if you send money to someone through your bank, you’re trusting your bank to make sure the money gets there.

If the person denies the money reached them, your bank can step in and prove it did.

With bitcoin, you can prove the money reached them without any need for a bank. You simply look up the transaction on the bitcoin network, and there it is, for anyone to see.

So bitcoin basically creates a whole new monetary system. One that can’t be controlled, manipulated or corrupted by big banks, the government or anyone else.

(At least, in theory.)

And because of that, many crypto proponents believe now is the time when crypto – and bitcoin in particular – will prove itself.

As the value of currencies are eroded all around the world through money printing and relief packages, bitcoin’s supply remains unchanged.

This is the exact scenario it was created for.

And after an initial capitulation at the beginning of the pandemic, it’s actually one of the few assets that’s up year to date (YTD).

Today it’s around 1% down YTD. Which, as you know, in crypto, could change in minutes.

Meanwhile…

The Dow is down 15% YTD.

The S&P 500 is down 11% YTD.

And the FTSE 100 is down a whopping 23%.

As the global fiscal stimulus continues in the months that come, it will be very interesting to see what happens to those figures.

Especially as we’re now just weeks away from the bitcoin halving.

But all this does kind of throw up a counterargument to bitcoin.

I mean, if governments weren’t able to print more money and prop up the economy right now, millions upon millions of people would be going hungry.

And to quote an old band I used to listen to religiously as a teenager: “Hungry people don’t stay hungry for long.”

We’d soon see riots, revolutions and countless deaths in developed countries around the world.

So maybe money printing isn’t so bad after all. Who knows?

Something to think about.

PS If, after reading all this, you want to know the cheapest, easiest and safest way to buy bitcoin in the UK, you can read my free guide here.

This article originally appeared on coinconfidential.com.

The bitcoin halving happens in less than one month, but will it change anything?

I’m changing things up on our format for this piece.

Instead of the usual narrative-style article, I’m going to give you a round-up of some recent crypto-related stories I’ve been following.

Every time I see an interesting article or comment thread, I save it into my notes to use in an upcoming issue.

However, a lot of these discoveries don’t really fit together in a nice, narrative way, so they end up being left out of my usual issues… which is why today, we’re having a bit of a mashup.

So let’s get on with it.

T-minus 24 days to the bitcoin halving

In all the furore of recent weeks, the bitcoin halving has hardly made any headlines.

But, it’s fast approaching. And the jury is still out on what effect it will have on bitcoin’s price.

I’ve written before about how this could affect bitcoin’s price. But to summarise: if the supply decreases and demand stays the same, you would expect prices to rise.

However, that’s assuming the halving hasn’t already been priced in, which it may well be.

So… bitcoin’s price may go up, down or stay the same. No one really knows.

But whatever happens, it will have a big impact on how bitcoin is viewed as an investment going forward – for better or worse.

However, there is something else to consider.

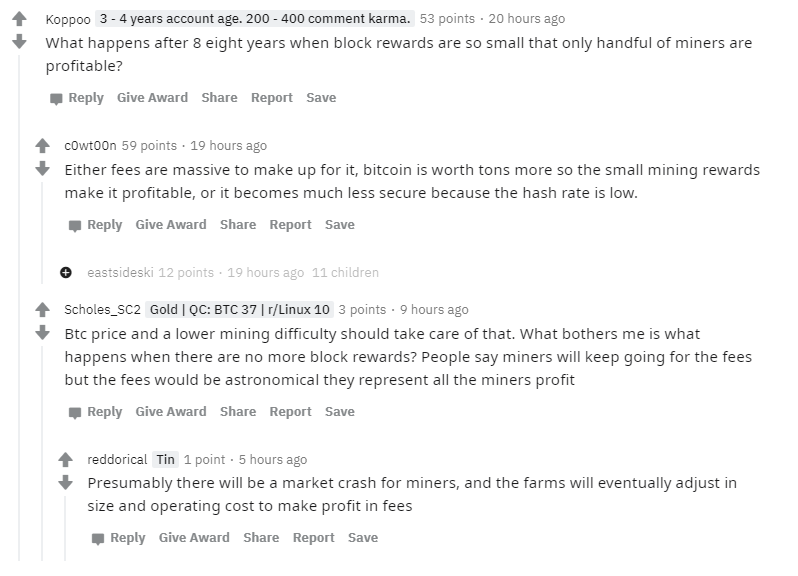

When bitcoin’s block rewards halve on 12 May… what if its price or network activity doesn’t increase enough to make mining profitable?

I thought this was an interesting thread exploring that idea:

Source: Reddit

Blockchain may provide the answer to coronavirus “immunity passports”

As much as I try to avoid commenting on the coronapocalypse, it’s pretty hard to completely ignore it.

A few weeks ago – near the beginning of the frenzy – I read an article in The Economist which summed up the entire situation extremely well, and without the usual hype or sensationalism we see in the media.

As I said to some friends at the time, you could basically just read this article and then ignore all the other news stories until the world returns to normal.

(Which I would love to do, but that’s proving to be near impossible. It’s a golden age for groupthink and media hysteria… which is then endlessly forwarded around every social circle you’ve ever had contact with.)

If you’re interested in the full Economist article, you can read it here.

Here’s its conclusion paragraph:

Suppression strategies may work for a while. But there needs to be an exit strategy—be it surveillance, improved treatment, vaccination or whatever. If governments impose huge social and economic costs and the virus cuts a swathe through the population a little later, they will discover that when politicians disappoint the people over something this serious there is hell to pay.

Basically what it was saying was that without “surveillance, improved treatment, vaccination or whatever” some form of lockdown will continue indefinitely – or at least until society shuns it.

Clearly a vaccine would be the best way to do this. But as I’m sure you’ve heard repeated ad nauseam, that is likely “12 to 18 months away”.

So the next best solution is immunity passports. If you can prove you’ve had the virus, you can regain your freedom.

But how can you create a programme like this while maintaining some semblance of privacy and ensuring authenticity of the passports?

Sounds like the perfect application for a blockchain solution. And that’s exactly what’s happening.

From CoinDesk:

The COVID-19 Credentials Initiative (CCI) is working on a digital certificate, using the recently approved World Wide Web Consortium (W3C) Verifiable Credentials standard. The certificate lets individuals prove (and request proof from others) they’ve recovered from the novel coronavirus, have tested positive for antibodies or have received a vaccination, once one is available.

Over 60 organizations in the SSI space are participating, such as Evernym, Streetcred, esatus, TNO, Georgetown University and others. The initiative also has a global spread including Consulcesi in Italy, DIDx in South Africa, TrustNet in Pakistan and Northern Block in Canada.

These digital certificates would be issued by health care institutions but controlled by the user and shared in a peer-to-peer manner. (A common misconception is that self-sovereign means self-attested, which removes the need for governments and other authorities; trust in the issuer of the credential is critical, said a spokesman for Evernym.)

…

It’s a system that puts the holder at the center of things, rather than (an often tedious) back-and-forth directly between the issuer and verifier. It also gives the holder power to choose what they want to share and with whom.

Whether it will amount to anything or not, I guess we’ll have to wait and see.

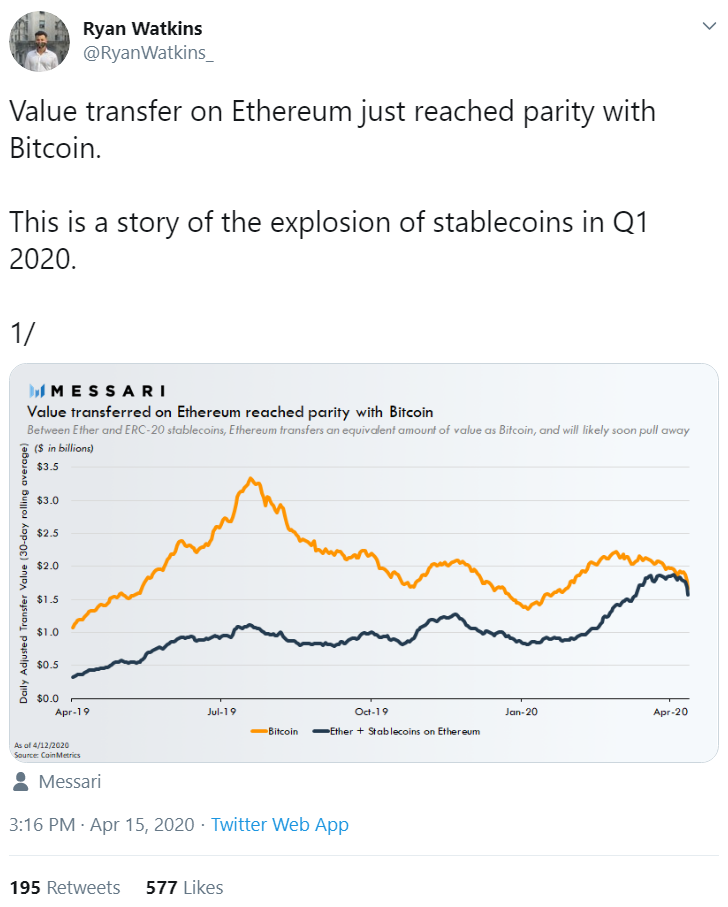

Ethereum now transfers just as much value as bitcoin – could the flippering be back on the cards?

Well, the inevitable finally happened. Ethereum’s network is now moving around just as much money as bitcoin’s.

Source: Twitter

Given how many more applications can be built on Ethereum, it’s no surprise this has happened. It’s just, no one really expected it to happen so soon.

The reason for this move is mainly down to… yes, you guessed it… coronavirus. (Really not doing well avoiding coronavirus in this week’s issue am I?)

As Ryan Watkins explains in a series of tweets: So we now have another important metric for which Ethereum has equalled bitcoin.

I wrote about another, much smaller “flippering” event late last year: Ethereum finally flips bitcoin. And if you’re not familiar with the idea of the flippering, I can recommend reading that article.

When will Ethereum complete the actual flippering? That’s anyone’s guess. But I’m convinced it will happen eventually… given how much more can be build on Ethereum than bitcoin. Especially once Ethereum 2.0 launches.

The US was on the cusp of creating a digital dollar to combat the coronavirus recession

Okay, now my attempts to avoid mentioning coronavirus are completely out of the window. I’ve accepted that.

So on to our last story of the week.

Actually, this story isn’t all that new. It’s just I couldn’t find an article to fit it into up until now. But it made some pretty big waves at the time.

When the US first proposed its economic measures against coronavirus, it first included a recommendation to create a digital dollar.

From CoinDesk:

Proposed legislation meant to shore up the U.S. economy during the coronavirus pandemic includes a recommendation to create a digital dollar.

This virtual greenback would help individuals and families survive the shutdown of businesses and series of “shelter-in-place” orders which resulted in skyrocketing unemployment claims and a potential severe recession.

Under the draft bills shared last week, dubbed the “Take Responsibility for Workers and Families Act” and the “Financial Protections and Assistance for America’s Consumers, States, Businesses, and Vulnerable Populations Act,” the Federal Reserve – the nation’s central bank – could use a “digital dollar” and digital wallets to send payments to “qualified individuals,” consisting of $1,000 for minors and $2,000 to legal adults.

Both bills employ identical language around the digital dollar suggestion.

“The term ‘digital dollar’ shall mean a balance expressed as a dollar value consisting of digital ledger entries that are recorded as liabilities in the accounts of any Federal Reserve bank; or an electronic unit of value, redeemable by an eligible financial institution (as determined by the Board of Governors of the Federal Reserve System),” the bills read.

In the end the US decided not to go down this route and later versions of the “Take Responsibility for Workers and Families Act” had the “digital dollar” section removed.

But either way, that was major news from a crypto point of view.

Of course, the digital dollar wouldn’t be a true cryptocurrency, just like the other Central Bank Digital Currency (CBDC) programmes around the world won’t be.

But it shows how seriously CBDCs are now being taken, even by the US.

And eventually, it seems, all currencies will become digitised.

For more on what that will look like, and what it will mean for us, check out my article: Central Bank Digital Currencies are set to shake up the financial world in 2020.

Okay, that’s all for this week.

Thanks for reading.

Harry Hamburg

Editor, Coin Confidential

This article originally appeared on coinconfidential.com.