How investor psychology drives the next five years

29th January 2021 |

As usual, below is Akhil Patel’s latest monthly market commentary update. In Akhil’s monthly updates he covers some of the key events in the markets that he thinks are relevant to investors based on his views that markets move in very distinct cycles, which if you know how to read properly, can help develop a much deeper understanding of how assets move in value.

Akhil’s views are his own and are designed to provide you with a more rounded, comprehensive view of the markets and investment assets.

If you’re new to Akhil’s work and enjoy what you read, you can find previous monthly reports from him within your Frontier Tech Investor subscription. You can find his latest, January update below.

Regards,

Sam Volkering

Editor, Frontier Tech Investor

A very happy new year to you!

I very much hope that 2021 brings with it much joy, freedom and a relative return to normality – though after almost a year of enduring the strange circumstances in which we now find ourselves, it’s hard to imagine that things will ever quite be the same again.

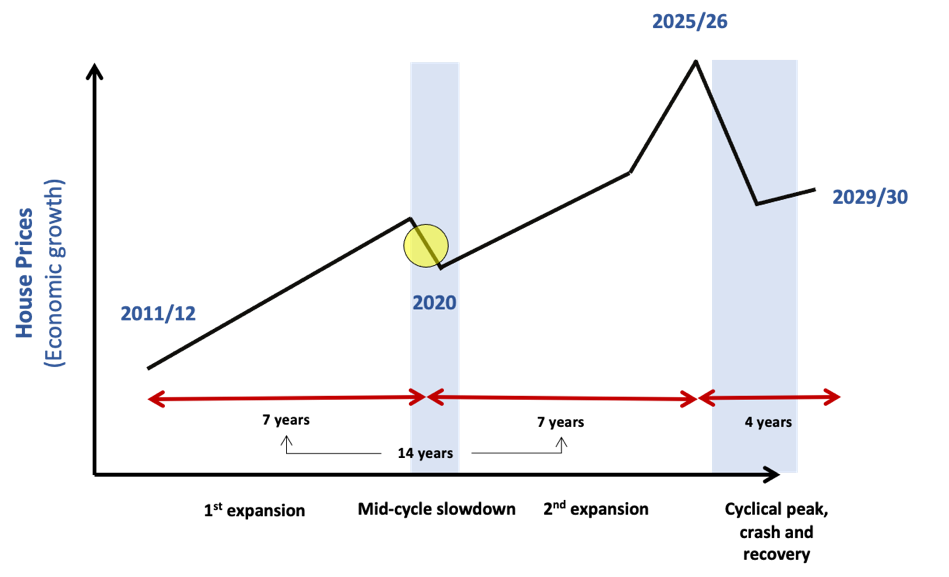

But one thing that hasn’t changed, or been altered, is our progression through the cycle. The diagram below illustrates where we are presently, indicated by the yellow dot – we are moving through the mid-cycle slowdown or recession.

Source: Ascendant Strategy

Source: Ascendant Strategy

Those of you who have been following my work for some time will know that the mid-cycle is a key moment within each overall cycle, even though it is the lesser of the two main recessionary periods. In last November’s update, I discussed how the mid-cycle played the same role as the the midpoint within the structure of a successful Hollywood movie – the scene at the mid-cycle is the pivot upon which the movie turns and the point at which the stakes for participants in the drama are raised significantly.

The story of each real estate cycle is similar. The mid-cycle turns our attention forward to the more consequential half. And from my reading of history, it seems that it is precisely because the mid-cycle is difficult and challenging that we behave, paradoxically, more bullishly in the second half of the cycle. I will come back to this point shortly.

But for the time being we will still be in the mid-cycle recession unless things open up pretty sharpish. But given the latest news on the spread of the virus, I think it will take some time for that process to even begin. And there will be a lot of economic pain to process this year, so expect the news to reflect that.

But this year will begin the second half of the cycle. Setting aside the rather significant moves in the stock market we have seen in past few months, the economic action starts slowly, but builds inexorably.

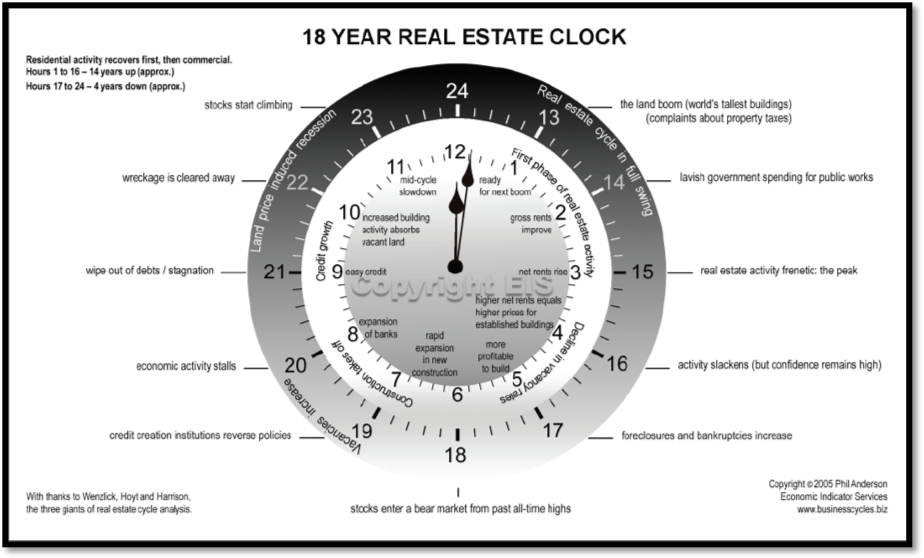

How it does so is set out in the 18-year real estate clock below, hours 12 to 15.

Source: Phil Anderson, Secret Life of Real Estate and Banking

Source: Phil Anderson, Secret Life of Real Estate and Banking

We are currently at around 12 o’clock of the clock, about to move on to 13 o’clock, and the beginning of the land boom.

Let’s turn to how things should play out from here, if history is to repeat. If 2021 gets the second half underway and we work through the economic adjustments that take place after every recession, by 2023 things will be humming along again rather nicely. Having seen off the mid-cycle, and returned to growth and better times, by then the mood should be approaching optimistic, perhaps even with a touch of over-optimism, certainly as we move into 2024.

This is in part driven by an expansion in bank credit. Bank lending has been largely unaffected by the present recession. The reason? Because property prices have largely been unaffected. Even though rents have come down in certain areas, prices on the whole have remained stable and in some cases have increased.

Part of the response to the pandemic has been to loosen banking regulations in the US, Europe and Australia, allowing banks to dip into capital buffers to expand lending. The combination of banking resilience and more available capital means that as economies open up, banks have plenty of headroom to expand lending. Combined with lavish spending on infrastructure that inevitably raises land prices (14 o’clock) and after solid growth in loan books into 2024, the cycle will go into overdrive.

Expect bank lending to be leading the charge: to maximise profits banks need to be fully loaned up and as lending is a profitable activity (despite ultra low interest rates, the key variable for bank earnings is the difference between what they pay on deposits or borrow short term in the money markets, and what rate they lend out on: this is still positive) there will be increasingly fierce competition to lend to people. The biggest element of this activity is of course lending to real estate.

The period of 2024 and 2025 should see intense competition and frenetic activity (15 o’clock). This does not necessarily mean very high GDP numbers, but it does mean rampant speculation and an investor mood that goes from over-optimistic and euphoric into mania. It’s when everyone is fully in that peak; the first sign of this will be a slowdown in the property market even while everything else is seemingly unstoppable. The peak should arrive around 2026, approximately 14 years from the lows in the land market around 2012.

This is how the next few years will play out, should history repeat, and this process will get started some time this year.

Investor psychology during the second half of the cycle

When it comes to it, events might on the face of it seem different to the way I have described above. Lending may seem fairly “prudent” on the whole, or at least we will be led to believe that. Perhaps the investment fad may be seemingly unrelated to property, such as something like green energy or cryptocurrency.

This is why no one really sees the economic events for what they are – a repetition of the real estate cycle. But the underlying psychology will be exactly the same, swinging from fear during the mid-cycle to the euphoria/mania of the peak. And the mania is always founded upon speculation in rent-based assets (for a reminder of the importance of economic rent to the cycle, see this issue here).

The celebrated investor/market commentator, Howard Marks of Oaktree Capital (and author of a very interesting series of memos about markets – which can be found here) often discusses investor psychology and how it seems to swing between the extremes of depression and euphoria. A good distillation of his ideas about market cycles and how they play out can be found in his new book, Mastering the Market Cycle.

He likens the general investment mood to a pendulum that swings between these two extremes. And as with any pendulum it’s precisely the extremity of the swing in one direction that determines the strength of the swing back to the other extreme: in other words, the further the pendulum swings in one direction, the further it will go in the other. It is also for this reason, Marks sagely notes, that investors rarely spend any time in the middle (the place at which there is emotional balance).

What Marks does not explain is what causes the pendulum to swing in one direction or the other, or change direction. I believe the real estate cycle supplies the missing piece. Our psychology turns because of the story that builds around the mid-cycle.

Elements of the mid-cycle “story”

In essence, the elements of pretty much any story are the same.

All good stories involve a hero, who leads or drives the action forward. He or she is confronted by a challenge, often involving some sort of internal or external conflict. How the hero overcomes that challenge is the main part of the story; and this generally resolves itself into a victory. And as a result of the victory, the hero, and by extension the world (and the audience), has expanded its awareness.

The most common story we tell is one of a hero battling a monster that threatens the life of the family or community. At first the hero is innocent of the danger, but in the background lurks a monster that reveals itself. There are some initial clashes, in which the hero does well, but at the midpoint of each story something happens (usually an action by the monster) to ensure the stakes get higher.

The extent of the threat posed by the monster is fully revealed. The hero battles gamely on, often having to persevere through a series of reverses and losing battles. And just when things seem darkest, and he is on the edge of defeat, he arms himself for one final battle, from which he emerges victorious. And in the ensuing celebration or relief, the hero and community are forever changed.

These are the basic elements of any story – but the particular form it can take is virtually infinite. But the key point is that there is a struggle and there is victory. We tell variations of such stories to ourselves about everything and you can find this same basic structure in stories as varied as the earliest epics told by bards in ancient Sumer and modern-day television dramas on Netflix. But we also tell these stories about our economies – and perhaps the most potent telling of them all comes out at the mid-cycle of each real estate cycle.

Think back to the mid cycles of previous real estate cycles to see what I mean. In 2001 the US economy was slowing into the mid-cycle; then 9/11 occurred. In response to both, then Federal Reserve chairman Alan Greenspan – who was already widely feted for his ability to “manage” the business cycle – lowered interest rates and held them low for some time. President Bush initiated a round of tax cuts; and he told Americans it was their patriotic duty, in response to the attacks on the World Trade Center, to go out and spend in order to safeguard the American economy and maintain the American way of life.

To hear the story told back then, it became a tale of enlightened policymaking, allied to collective effort, that moved the economy out of recession and into a new decade. Given what happened in 2008, the story no longer holds up. However, at the time it was a credible story and it served its purpose: there was renewed confidence in the economy that ultimately resulted in the boom of the 2000s.

In the early 1980s, the enemy was inflation. Again, the hero was the then chairman of the Federal Reserve, Paul Volcker, who raised interest rates to around 20% to combat inflation. It worked (albeit at the cost of a very significant recession which created many social problems) and inflation was defeated “permanently”.

The fact that Volcker was prepared to allow the market to (temporarily) dictate the rate of interest, fed into the other dominant story of the 1980s – that the market should be left alone and that the government should step out the way. In some ways, the story is incorrect; government deficits exploded in the US during the 1980s. Furthermore, it was because interest rates were reduced during the 1980s (starting with the response to the Latin American debt crisis) that really helped bull market to get underway. But the story helped the US and the world move on from the turbulence of the late 1970s and early 1980s into the boom of the 1980s.

A similar story could be told about the mid-cycle of 1921: one physical enemy (Germany and the Central Powers) had been defeated by the Allied Powers; a public health enemy was also overcome (the Spanish flu); and the economic challenge posed by the commodity price collapse of 1919/20, as well as the ensuing post-war recession, was bested. The final act of this story was the heady optimism of the 1920s, a new beginning if ever there was one.

In our own time, economies were slowing in 2019 and the yield curve went negative, indicating the possibility of a recession (something I pointed out for you in the issues and updates from that year). But no one really paid much heed; the real monster arrived in the form of a deadly virus that has caused our economies to freeze up.

You can see the story building – after some initial skirmishes and setbacks, the government is making unprecedented efforts to combat it; citizens are making “extraordinary” sacrifices (in the UK, deliberately channeling the spirit of the Blitz); our heroes in the health services are battling to keep us alive; and our scientists have developed a vaccine in record time. We are fast rushing towards the climax of this story: the point at which the virus is defeated for good and we get back to living our lives, albeit that we will all be changed forever.

And here is the interesting bit: the more severe the mid-cycle challenge that has been overcome, in other words, the deadlier the monster, the greater the victory and the boom story of the subsequent years (similar to the old adage that the darker the night the brighter the dawn).

The key function of the mid-cycle story, as I suggested above, is to get investors looking forward, with renewed confidence that a challenge has been overcome, that policy is supportive and that the boom-bust cycle has been overcome. This gets the pendulum to swing in the opposite direction.

Marks also notes that the swing to the extreme of euphoria does not take place immediately. For a bull market to hold sway, the investment environment has to be characterised for some time by a combination of greed, optimism, exuberance, confidence, credulity, daring, risk tolerance and aggressiveness. The psychology of most market participants has to move in the same direction, and this takes time to happen. But once in place, the bull market psychology persists. This is why years of strong returns in the market tend to cluster together.

So, my argument here is that a particularly severe mid-cycle recession, rather than hindering the cycle, actually reinforces it. Isn’t that a paradox? But it seems to be the means by which we forget that there is a cycle in the first place, one that invariably ends with a major bust.

And around and around the cycle we go.

Yours sincerely,

Akhil Patel

PS Follow me on Twitter (@AkhilGPatel, @Propertysharem1).