Important: cannabis reorientation

21st March 2018 |

Cannabis is referred to as the “green rush” with good reason. It represents the opening up of legitimate investment in a market that was once wholly illegal, which already has a widespread following and is now progressing steadily towards to market permeability.

The legalisation movement is akin to the opening up of the alcohol business after the prohibition era and fortunes are being made by the growers and retailers of cannabis all over the world as the barriers to legitimate market participation fall. Initially that is where the primary money is going to be made.

Medium-term, the pharmaceutical industry is rapidly moving towards commercialisation of treatments that are based on cannabis’ renowned ability to help people relax, escape chronic pain and manage epileptic seizures.

I had a brother who was plagued by epileptic fits and to think that there was a potential avenue for research that could have eased his experience of life which was not fully exploited is galling to my family and I.

Chronic pain in particular is a massive global market. As we age, it is just a simple fact that more things go wrong with our bodies and our various appendages, joints and backs start to hurt. The treatments we have today just aren’t that effective for these kinds of pain. Opioids and other pain killers are addictive and additionally they don’t tend to be all that effective against long-term sources of pain. If cannabis can deliver on this area of the human experience then it has potential to become a staple in every household in the world in much the same way that paracetamol and ibuprofen are today.

There is a one primary risk to a speedy path towards legalisation and a flourishing of scientific endeavor in the cannabis sector and it is Donald Trump. In the US an increasing number of states have voted for legalisation. However, the federal government still classifies cannabis as a Schedule 1 drug, which is defined as “substances, or chemicals are defined as drugs with no currently accepted medical use and a high potential for abuse”. That does not stand up to reason when we look at the fact that there are pharmaceuticals on the market today that incorporate cannabis as an active ingredient and are being prescribed to patients.

The institutional antipathy today towards cannabis is such that it is considered more dangerous by the US federal government than cocaine, which is included as a Schedule 2 drug which is drugs, substances or chemicals that are defined as drugs with a high potential for abuse, with use potentially leading to severe psychological or physical dependence.

Trump has stated on more than one occasion how personally opposed he is to further legalisation. He was even gone so far as to threaten to overrule the actions of the states in legalising the herb. While it is extremely unlikely that he will ever follow through on those threats because of the constitutional implications such a measure would have, it is doing nothing to encourage investors into the sector and in fact is probably deterring interest.

The two stocks I have chosen to profit from the cannabis theme in the portfolio have not been performing as expected. The Trump administration’s combative attitude is at least partly to blame for that. Additionally, many subscribers have been having issues buying Terra Tech which means it is not an ideal vehicle for UK-based investors. Zynerba Pharmaceuticals is involved in the exploration of cannabis’ pharmaceutical benefits but it reported disappointing results with a trial in August and despite a brief recovery rally it has failed to recover.

I am therefore now recommending that you sell these investments since I no longer see much hope of the Trump administration undergoing a conversion to a more permissive stance.

Action to take: sell Terra Tech (TRTCD) and sell Zynerba Pharmaceuticals RG (ZYNE)

In their place I recommend buying Canopy Growth Corporation, which has a market cap of C$6.672 billion. Canada’s cannabis industry has been literally flourishing since legalisation. There have been no barriers erected at the federal level and the company has no problem banking its proceeds. This has resulted in the respective companies being cash generative and they are investing aggressively to capture market share as the industry continues to expand.

Canopy Growth Corp is the largest of the Canadian cannabis companies and in the event that the US market’s turmoil is ever resolved favourably, Canada’s companies will be in prime positions to move in aggressively to take a part of the US business as well. The risk with a company growing this quickly is that it outspends its growth potential. That was one of the primary contributing factors in the demise of Under Armour and it is a risk all companies with high-growth trajectories face. Additionally, it was a surge in public support for cannabis that got it legalised in Canada and therefore it is worth monitoring the tone of social commentary to ensure the regulatory background remains favourable.

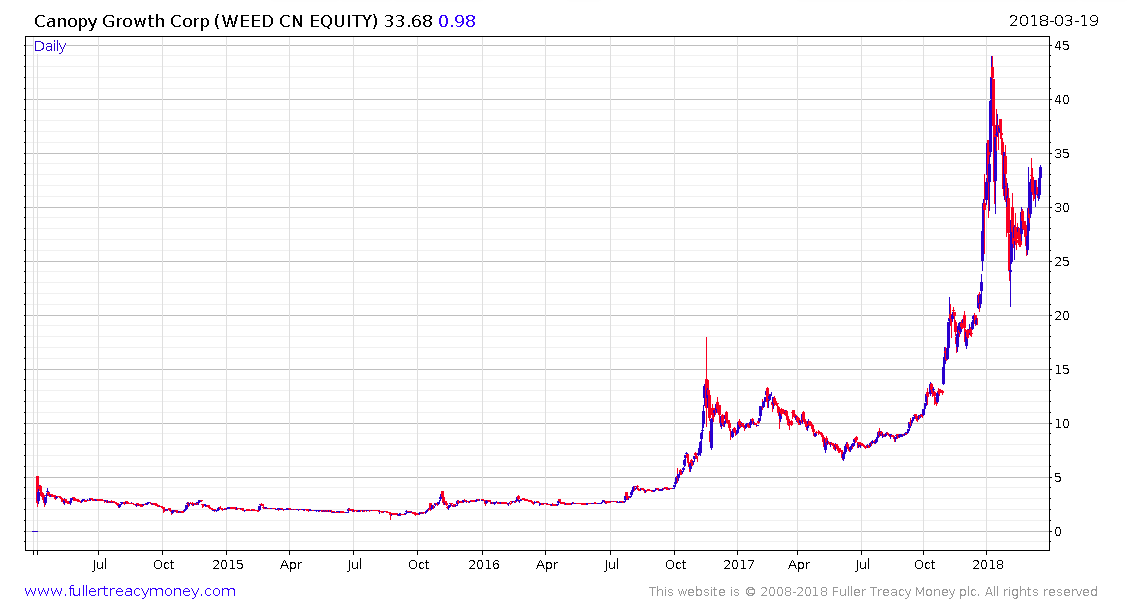

The share hit a medium-term peak at C$44 in January and pulled back to test the C$20 area by early February. Since then the share has trended higher and I rate it a buy up to C$35. My 12-month forecast is for the high near C$45 to be retested. Over the course of the next three to five years I expect to see the share trade up towards C$100.

Action to take: buy Canopy Growth Corp (WEED:CN) up to $35 (CAD)

Name: Canopy Growth Corp

Ticker: WEED:CN

Current price: 19/03/2018: $33.68 (CAD)

Market cap: $6.672 billion (CAD)

52-week high/low: $44/$6.58 (CAD)

Regards,

Eoin Treacy

Investment Director, Frontier Tech Investor