The future of tomorrow starts at the drive-thru

16th January 2020 |

Originally published under Growth Stock Network on 16th January 2020.

Having just come back from CES in Las Vegas I got a glimpse into my past, present and future. No it wasn’t some kind of Ebenezer Scrooge moment, I was able to get my hands on some retro arcade tech, some modern arcade tech and importantly some future arcade tech. NBA Jam, TMNT Arcade and Golden Tee Golf was the past. PlayStation and Xbox was the present. And VR arcade machines with drop down headsets was the future. This was a glimpse at how people will be able to access VR technology in the real world even if they can’t afford a set at home for the time being.

The widespread use of VR is coming to the masses and its coming fast. It’s coming via things like VR arcades and it’s coming to ‘experience’ centres all over the world. Before you know it, using VR when you’re out and about with the family won’t even be something ‘new’ it will just be a part of your connection with the future technology trends that sneak up on the masses out of nowhere.

VR and VR experiences are the future of entertainment, education and experiences.

Capitalising on the big trends of the 2020s before they grab the mainstream

I believe than starting now one of the biggest market trends to capture the market’s attention in the 2020s is the virtual “experience” market.

And through that we see technologies like augmented reality (AR) and virtual reality (VR) starting to really get mainstream, mass market appeal.

This will come via home and business use, but also will filter out into our wider world in the form of VR “experiences”.

Imagine going deep sea diving to discover the undiscovered worlds of places like the Mariana Trench. This is the deepest part of any ocean in the world. It’s also around 2,500km long and 65km wide.

At its deepest it’s approximately 10.9km down. But there are some that suggest it’s even deeper in some places. The thing is it’s near impossible to get humans down there.

For comparison, Mount Everest is only 8.8km to its peak.

Of course, you’re not about to book a deep sea holiday to the bottom of the Mariana Trench anytime soon. But why should that stop anyone from experiencing what it’s like down there and the kinds of sea life that exist in this mysterious place?

That’s where we believe VR experiences will have an increasing presence in our world. And it’s where a company like your latest recommendation comes into play.

Introducing your latest Growth Stock Network recommendation…

Immotion Group [LSE:IMMO] is listed on the London Stock Exchange AIM sub-market. It has a market capitalisation of just £21.17 million and trades for only 7.25GBX.

Immotion is a VR company. It builds and develops VR technology to implement in places like zoos and aquariums, museums and science centres and leisure and entertainment locations.

The company builds and delivers “theatres” to sites where the customer can sit in the Immotion “theatre”, put on a VR headset and experience one of several types of VR experiences dependant of course on the location and type of instalment.

For example, one of the growing areas for the company is the installation of its technology and delivery of VR headsets to aquariums.

It has “theatres” in size from two seats through to 24 seats. Thanks to wireless syncing technology, every person in any seat is able to experience the same VR experience as anyone else who is a part of that particular experience.

Some of its current aquarium-based VR experiences include swimming with humpbacks and Legend of Lusca – exploring shipwrecks in the Bahamas. It’s also got ones to experience shark diving and a coming-soon experience exploring seal populations in the Yukon in Canada.

These are of course aquarium-specific ones. There are also VR experiences such as the Tower Coaster, Mission to the Moon and a river raft ride down the Congo to experience animals from Africa.

It’s hard to explain how immersive and advanced VR technology has become today.

I remember as a kid setting into a VR headset to play a downhill skiing game. It was all “blocky” and limited in colours and smoothness of motion. But it was still mind-blowing as a ten-year-old.

Today thanks to advances in camera technology and display technology we can experience these worlds as though we really are there. And until you use VR yourself you never fully appreciate how you can really transport to another world without leaving exactly where you are.

Only now, because the technology to deliver the content has become so good, do we believe VR is ready to really explode into the market as a technology that becomes as ubiquitous as a cinema screen at a zoo, aquarium or entertainment location.

It’s the kind of technology that we see every aquarium and zoo in the world ending up with. And there may even be a point where the best and only way to really experience the wonders of mother nature is via VR as a way to preserve ecosystems and endangered animals.

That of course is the bigger picture, but Immotion is already working towards this future with its installations. It made deals to install Immotion VR in places like SeaLife in London, Blackpool, Paris, Legoland, Blue Planet Aquarium in Cheshire, the London Eye, Brighton Pier, the O2, Shedd Aquarium in Chicago and other locations around the world.

This “aquaria” focus is a short-term opportunity for Immotion to really capture a massive market share in VR experiences.

A December trading update noted this would be a focus for the company as these tend to provide better yields. Also with increasing interest in the US and Europe it makes sense for the company to focus here short term.

The model for Immotion is relatively simple. It doesn’t charge for the installations, but charges a per/headset training, set-up and maintenance charge.

Then with partner sites there’s also a revenue sharing with its partners for the experiences people pay at the locations.

For example at Star City Birmingham there’s an ImmotionVR installation with a range of different VR experiences. People can use their cinema pods to go Shark Diving, or perhaps plug into the VR Mutli-Racer to take part in one of the racing simulations.

There are locations like this in Manchester, Glasgow, Cardiff and other parts of the UK. You can see it all at immotionvr.com.

To go and use the machines will cost £6 a go in Birmingham for instance. Or for £30 you get a full hour to experience as much of these VR worlds as you like with the “Platinum Pass”.

It describes this as its “Partner” model. We think there’s longevity in these opportunities and while the company notes a crowded space in family entertainment centre markets it’s still something we think will draw in consistent growth for the company.

And the year is shaping up to be the start of what we anticipate to be ongoing growth for the company as its technology starts to really gain traction in markets, particularly in the US.

Just yesterday the company announced its current status for headset contracts and locations.

Two of its new partner sites are the London Eye and London SeaLife aquarium. At the Eye it’s installing a six-seater mini theatre. And an eight-seater mini theatre at SeaLife. These are just two installations of a total 93 that are contracted for the first quarter of 2020.

In total this now means the company will have 395 headsets installed after Q1. And according to the company it will achieve breakeven earnings before interest, tax, depreciation and amortisation (EBITDA) around the end of Q1.

What’s exciting about Immotion is it has a target to have installed 1,000 headsets by the end of 2020. If it can achieve that, we expect the company will be well on the way to achieving profitability and further growth in new markets.

The company says that weekly revenues per headset is around £305 for partner sites. Whereas “edutainment” sites like aquariums are yielding around £442 per week. If it can deliver 1,000 headsets in 2020 and even if the mix is 50/50 between “edutainment” sites and partner sites (avg. £373.50 per week per headset), then headset revenues per week would be around £373,500 – or 19.42 million annually.

Of course that doesn’t always equate to profit, but we think if it can achieve that, it’ll be well on the way to achieving full-year financial profitability.

The thing with this kind of technology is getting the ball rolling. Once you start to put installations in key locations like the London Eye, it starts to get awareness and reach into other markets.

And importantly, delivering the best quality content and experiences to the installations is what will keep them at locations around the world.

We’re excited about Immotion because of the breadth of experiences it can deliver. And we think the Partner model works well to entice partners into getting these installations on to site and then to fully appreciate the potential they have.

We see the rollout of headsets increasing not only to 1,000 over 2020, but even beyond that number. A recent deal with Aspro Parks solidifies this view.

The Aspro Parks deal is for the Blue Planet Aquarium in Cheshire. But looking beyond that, AsproParks operates leisure parks and centres at 68 locations around the world. These include aquariums and also family attraction parks.

These include, Walygator and Walibi in France, Top Camping in Finland, Linnaeushof in Amsterdam, Crocodile Park in Spain and even Hastings Castle and the 1066 Story in the UK.

That’s a potential 67 more sites that Immotion could see headsets going to if the Blue Planet installation proves to be a good partnership. These are the kind of opportunities that sit in front of Immotion and why we think there’s huge potential to capture a growing market in VR entertainment.

As we say, once the ball is rolling we think with these experiences the technology and the potential to roll this out across all markets globally is a huge opportunity for a small-cap, AIM-listed VR company.

Financials and risks

Its December trading update gave a glimpse of what the near future could hold for the company.

But the most recent financials to go off are interim results for the half year ended 30 June 2019. Based on those figures it brought in £1.3 million in revenues, well up from just £547,000 in the corresponding period the year prior.

This was clearly a growth period for the company. As such costs were higher than the previous corresponding period too. And they show a total loss for the period of £2.3 million vs £1.6 million the same corresponding period the year before.

At the time it had cash on hand of £2.3 million. That will have changed in the six months subsequent including a placement raising £2 million on 30 July 2019.

But these financials were some time ago, and we know it’s increased headset installations and has more contracted as per its update this week.

Hence we still expect it will achieve EBITDA breakeven in Q1 and think this will be a catalyst for the stock to press forward in the remainder of the year.

Also we anticipate its next set of financials continues to show growth and the opportunity in front of the company. Again we think this could be a positive catalyst for the stock to move higher short term and why we think the time to get in is now.

Of course you must be aware of the risks too.

This is a small, almost micro-cap AIM-listed company delivering VR hardware and content to partners and installation sites around the world. There’s some capital expense in delivering and installing these set-ups.

Hence it is reliant on ongoing usage and revenues for the ongoing training, maintenance of these sites. What would cripple the company and the stock price is when these installations have been in place and then are removed from sites or replaced with competitor installations.

Hence it’s critical to see ongoing growth in headsets contracted for and installed. Stalling, or backwards movement in headset numbers is going to be a poor outcome for the company. We don’t anticipate this short term, as we see them in a growth phase right now, but it’s a possibility down the track.

A lot of that comes down to the ongoing maintenance of the installations and importantly the content.

For a start it’s important that as the VR tech improves, Immotion’s installations improve with it. Some of this costs we expect the company will bear, as well as thits partners, but failure to improve the tech could result in less usage of the headsets and lowering average revenues per headset.

Furthermore, if the content is poor it leans towards customers using it once and likely not again. Word of mouth for these sorts of technologies is also important. Poor content or lack of new updated experiences again would be a drag on the stock.

While not something again we anticipate, it’s important to keep an eye on these aspects of the ongoing performance to ensure it is staying fresh and relevant to customers.

And financially while we see the company growing, it’s also important for the market and shareholders that they head towards profitability. Losses we can stomach during a growth phase. And we may even expect some capital raisings to accelerate growth.

Note, capital raising dilute shareholder holdings, but if applied properly to growth can offset this by rises in the stock price.

Ongoing losses, or growing losses without a path to profitability, will hold the stock price back. The next few sets of financials and interim financials are important as we’d want to see a trend heading towards profitability if the company starts to hit the targets it has set.

Considering the risks but looking at the opportunity for VR experiences to hit the mass market, we think Immotion Group is a red-hot stock to get into now.

Action to take

Immotion Group Plc. [LSE:IMMO] is an AIM-listed company trading for 7.25GBX. 90-day average volumes are 446,732 shares. That’s a value of around £31,848 per day in trading.

That makes it what we’d consider illiquid. Hence, we warn that upon our recommendation there a likely chance the price of the stock will spike.

Again make sure to use limit orders in the market sticking to the buy-up-to price. Patience is recommended if it shoots over the buy-up-to as often the dust will settle in subsequent days in trading.

We set buy-up-to prices to ensure that you don’t pay over the odds for the stock. Paying over the odds has the potential to erode future gains. So it’s important not to get too carried away if there’s an initial spike and remain patient using limit orders when placing your trades.

I recommend you BUY Immotion Group Plc. [LSE:IMMO] current price 7.25GBX, buy-up-to 8.55GBX. Make sure to use limit orders and to stick to the buy-up-to price. We will record the opening of tomorrow’s market for track record purposes.

Action to take: buy Immotion Group Plc

Ticker: IMMO: LN

Price as of 16.01.20: 7.25 GBX

Market cap: £21.17 million

52 week high/ low: 11.60p/ 4.63p

Buy up to: 8.55GBX

An update on your current Growth Stock Network recommendation…

I drive around the corner and take a left into the McDonald’s entrance. I pull around to the drive-thru ready to place my order.

Damn. The queue is about ten cars deep already, across both order boxes. And now a couple of cars have pulled in behind me.

This is where I’ll stay until the trickle of orders get through and I gradually make my way to the (still) confusing menu. You’d think after 30-odd years of McDonald’s I’d have a grasp of the menu.

Nope, it’s still as confusing as ever.

Yet still the whole drive-thru experience is still preferred to parking up, going in, placing an order on the “faeces-screens”, waiting and then getting going with a bag of food in tow.

Oh, what do I mean by faeces-screens? Well it’s pretty common knowledge that all kinds of things we encounter on a daily basis have all kind of harmful bacteria on them. Doorknobs, kids toys, handles and rails out in public, escalator belts, you know the usual things we might touch or grab every day.

And some of these bacteria are ones found in poo. Yep, hate to break it to you but most days you come into contact with poo-bacteria. Now the bacteria is micro and unlikely to ever make you sick. But it’s still there. And McDonald’s touchscreens have been found to carry all these bacteria.

Metro.co.uk did a sample of eight McDonald’s: six in London, two in Birmingham. According to Metro.co.uk,

Senior lecturer in microbiology at London Metropolitan University Dr Paul Matewele said: ‘We were all surprised how much gut and faecal bacteria there was on the touchscreen machines. These cause the kind of infections that people pick up in hospitals.

Now of course McDonald’s does clean its screens with disinfectant. And you should always wash your hands after using things like public touchscreens before eating food. Still, most people don’t. And that’s gross.

My solution is to use the drive-thru… even if there’s a massive queue and I’ve got to wait. No public touch screens for me thanks!

Still, no one likes to wait in a drive-thru either. And McDonald’s realises this. In fact, McDonald’s is pretty smart. It knows if it can cut down queues at drive-thrus, make the process faster, get more people “thru”, that’s better for its bottom line.

But how do you make a pretty efficient system even faster? Well it’s obvious isn’t it? In the 21st century, in the year 2020, you use artificial intelligence (AI).

In 2019 McDonald’s made two significant acquisitions. One a data AI company, Dynamic Yield, which it paid US$300 million for. Another, Apprente, an AI company focused on using AI-voice systems for food ordering.

Dynamic Yield is supposed to help change menus on the fly according to weather, time of day and traffic. Apprente is designed to interpret and deliver an outcome from voice inputs faster and more efficiently than a server in the window.

Also with a bit of number plate recognition it’ll also be able to offer up your “usual order” based on the time of day you visit as well.

This isn’t designed to replace jobs, instead it will enable human workers to serve the customer better. Hence AI’s implementation in a retail environment like McDonald’s enables customers a better experience from entrance to exit.

It’s significant when the world’s largest fast food company is diving deep into AI. What’s also significant is its use of AI to improve the customer experience.

You see AI is what I consider to be one of this decade’s “transformational technologies”. It has the kind of game-changing potential to touch and impact every industry in the world.

I bet five years ago you didn’t think that AI would be implemented by McDonald’s, yet here we are.

And recently at CES a panel talking about the economic impact of AI estimated the global impact of AI over the next decade would be in the region of US$16 trillion. That’s a huge opportunity if you can ride the right AI trends at the right time.

Of note as well during that session was a universal agreement that one of the key early areas of AI impact would be in retail and customer services. The implementation of AI would help lower costs yet improve the customer experience and bolster ever-squeezing margins.

And we think they’re right. Retail and customer services are ripe for AI to come in, sweep up the mess and enable far better customer experiences. Not only does it allow for greater customer volumes, but also builds brand loyalty.

I could go to Burger King or KFC drive-thrus, but if my McDonald’s experience is better, I know where I’ll be going again next.

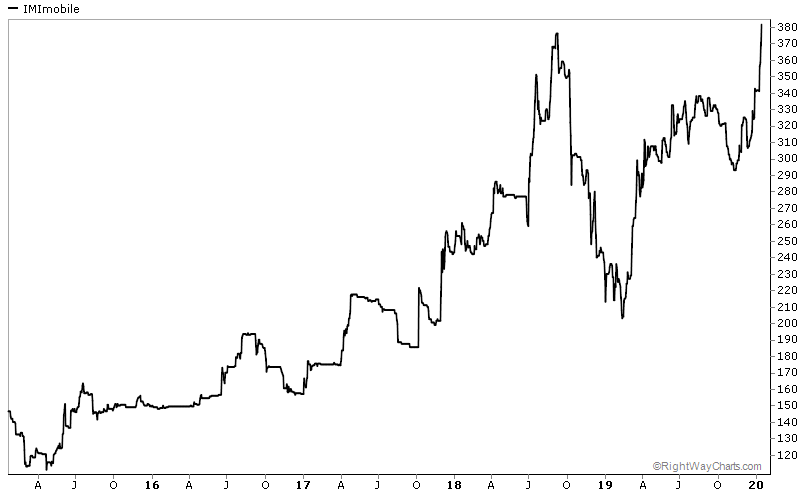

IMIMobile Plc. [LSE:IMO] is a software company that delivers cloud-based software, to automate and deliver better customer “journeys” to organisations. Some of its customers include AA, BT, EE, Foxtons, Pizza Hut, Vodafone, AT&T, Barclays, Lloyds Bank and RBS.

The company is traded on the London Stock Exchange AIM sub-market with a current market cap of £284 million and a current price of 372.50GBX. That does make it on the larger side of the small-cap market we focus on, but still small enough to open it up to the big gains we expect from AI-involved companies over the next few years.

IMIMobile develops and sells automation software to its clients. This comes via a cloud-based platform primarily – what it labels as IMIConnect.

This is a drag and drop platform that plugs in a range of application programming interfaces (APIs) so a business can communicate and connect with their customers via Twitter, WhatsApp, SMS, email, Messenger, voice calls, Apple Business chat and a range of other communication channels.

In setting up like this it can automate an entire customer journey with ease. In a world where legacy businesses are still struggling with how to improve customer experiences and using old systems like call centres, there’s a real market opportunity for IMIMobile to capture business across the globe.

It is of course a crowded marketplace. But IMIMobile has achieved growth and brought in significant large-cap companies like those mentioned above as customers for consecutive years.

Why we’ve now decided to change the stock recommendation to a buy and raise the buy-up-to price is the changing nature of AI and its ability to implement AI through its automation platforms, specifically its AI chatbots.

The IMIbot.ai is a part of its customer experience (CX) Automation Cloud.

Automating a customer “journey” is important to assist businesses in managing costs as well as making its social media, marketing or chat available through an application or browser.

This enables businesses to map out workflows from when a customer might enter their channels and predict and manipulate the process through their sales and marketing.

What this in effect does is enables a business to automate a lot of the process that gets the customer to what they want, when they want it and importantly maximising the monetisation of each potential customer.

One of its more promising parts of the product suite is the IMIbot.ai.

This is a AI-driven chatbot that you would encounter through a help or contact section of an app or site that actively helps a customer get to the end result without actual human intervention.

This process of automation and AI-driven communication is the future for customer experience with ecommerce and retail businesses.

You sometimes hear pushback from people about “not wanting to talk to a machine”. But a lot of the time with these AI implementations of customer service you don’t even know you’re talking to AI. Or if you do, so long as you get what you need quickly and efficiently, does it really matter?

These AI systems like IMIbot.ai also connect directly to human customer service when needed and without friction. This just makes the whole process smooth for the customer.

We believe that companies will continue to lean more and more on these types of automation and AI-driven communication channels. And we think that right now IMIMobile is red hot as it starts to expand its reach around the globe.

It recently acquired a company in North America, 3CInteractive. 3C is another cloud-based “customer engagement” platform. This acquisition is specifically to enable IMIMobile to broaden its reach and accelerate growth in what it describes as, “the largest addressable market for the group’s software.”

This acquisition, the software and its potential to reach across industry, the implementation of AI and automation within its platform and the company’s strong track record of growth makes it a perfect company to get a foothold in now, before it starts to realise its growth potential in the US.

We think it’ll continue to grow existing markets, but really see acceleration in US sales and growth as the acquisition rolls out and IMIMobile gets a real foothold in the US market.

And, as we say, it’s got a strong record of growth which we believe it will continue to demonstrate with its full-year results and the subsequent financial year.

Financials and risks

Based on IMIMobile’s interim figures for the six months ending September 2019, the company is delivering consistent growth and importantly is profitable.

Also according to the company, it’s delivered a consistent five-year compound annual growth rate (CAGR) of 21%. Its six-month interim results shows,

- Revenues of £83 million compared to £67.2 million from the previous corresponding period

- Gross profits of £35.2 million compared to £29.1 million from the previous corresponding period

- A statutory after-tax profit of £707,000 compared to a loss of £92,000 from the previous corresponding period.

All of this is exactly the kind of numbers you’d want to see from a company that’s heading from the small-cap space to the large cap-space. And that’s exactly where we see IMIMobile heading.

If it can capitalise on the US expansion, bring in greater revenues and turn those into growing profits then we would expect the company’s stock price to reflect this going forward.

And if it can deliver after-tax profits growth as it scales up, then this could even turn into what I refer to as a “Golden-Egg Stock” – a small cap that turns a profit and pays out a dividend.

But it’s not there yet. We see that is the direction it’s heading and we believe it’ll get there.

This comes with risk, however.

As noted there’s competition risk in play here. There are a lot of software providers delivering cloud-based platforms to businesses. There are others that deliver this kind of drag and drop platform to automate workflows and processes for customers.

And there are other companies that are looking to roll out AI-enabled automation like AI chatbots to help the customer journey.

One of the opportunities we see is potential growth in the US market. We expect growth here, but if growth is slow or underwhelming this could have a negative impact on the stock.

This could come from competition-winning contracts over IMIMobile or from an inability to convert customer prospects to paying customers. If it can’t capitalise on the US market in the next 18 months we may see the stock draw back.

Also if the company cannot continue to deliver growth, that’s also going to rock the share price. It prides itself on consistent annual growth. We again expect that to continue, but if it doesn’t, or if there’s a step backwards and the company shrinks, it would hit the stock price hard.

Remember, it’s still small cap so growth isn’t a guarantee, albeit here it’s an expectation and part of our thesis for recommendation.

And of course there’s just wider macro risks around global markets having been on a strong run over the last few years. Difficulties or wider market weakness regularly comes back to hit small-cap stocks. This of course is out of the control of the company but it is a risk to consider.

But looking at the risks vs the potential opportunity the company presents, we think this is a stock worth taking a punt on as it taps into the future world of customer experience automation and AI rollout.

Action to take

IMIMobile [LSE:IMO] is an AIM-listed company trading for 372.50 GBX. 90-day average volumes are 129,306 shares. That’s a value of around £489,288 per day in trading.

That makes it relatively liquid. However, we do warn that upon our recommendation there could be a bit of a spike in the price of the stock, hence it’s important not to get too carried away if the stock does run and let the dust settle by using limit orders when placing your trades.

I recommend you BUY IMIMobile [LSE:IMO] current price 372.50GBX, buy-up-to 435GBX. Make sure to use limit orders and to stick to the buy-up-to price. We will record the opening of tomorrow’s market for track record purposes.

Action to take: buy IMIMobile Plc

Ticker: IMO: LN

Price as of 16.01.20: 372.50 GBX

Market cap: £284.34 million

52 week high/ low: 383.50p/ 203.00p

Buy up to: 435GBX

Regards,

Sam Volkering

Editor, Growth Stock Network