Investing low on the value chain

ISSUE 4th February 2022 |

Last month I introduced the theme of a “bear market in trust” that was likely to impact financial markets throughout 2022. Sure enough, stock markets have stumbled somewhat in recent weeks, for reasons ranging from expectations of higher interest rates to geopolitical sabre-rattling over Ukraine in Europe and Taiwan in the western Pacific. But if trust continues to erode, and I see every indication that this will remain the case, then investors should remain cautious.

Taking a broad look at the markets, not much has really changed. Sure, a few stocks have been sold off hard, but more for idiosyncratic than systemic reasons.

Tesla had begun to decline last year, from around the time that CEO Elon Musk announced that he was going to liquidate part of his large holding. MicroStrategy, Inc, which has built up a large, leveraged position in bitcoin to much fanfare, has been hit by the sharp drop in the leading cryptocurrency, as has Coinbase, the US’s largest listed crypto exchange firm. While the crypto craze continues to grab headlines, it remains a highly speculative, idiosyncratic market with no obvious macroeconomic significance or correlation with the overall stock market.

Following some volatile trading, year-to-date the UK FTSE nearly unchanged. Tech has underperformed, but if this is due primarily to declining earnings growth expectations, then in valuation multiple terms, the market hasn’t really corrected at all.

A bear market in trust is something more. It implies that investors will demand substantially lower, more conservative multiples on firms, especially those with a disproportionately large amount of intangible, hard-to-value assets on their balance sheets, including tech.

Be wary of inflation

The fact that we have now entered an inflationary environment is also of major concern. Inflation creates price information feedback loops, distorting rational economic calculations. It becomes unclear to what extent price rises are sustainable and what portion thereof can be safely passed by businesses along to customers without losing excessive market share.

Hence managers find it more difficult to run their operations as efficiently. Inventories build and deplete against expectations. Product mix at time and place becomes suboptimal. Resources become misallocated.

Over time, these largely hidden factors – which are frequently overlooked by mainstream economists and analysts – begin to harm productivity, squeezing corporate profit margins even further. Businesses become reluctant to invest, with negative consequences for long-term growth. The result can be a prolonged period of stagflation such as that observed in the 1970s and early 1980s.

The combination of tighter profit margins and lower overall economic growth expectations can lead investors to substantially reassess what they believe firms are actually worth. That will pull valuation multiples down – however, will that result in outright share price declines in a highly inflationary environment? That is far from clear.

Given that we are now deep into an inflationary environment – the most inflationary in the lifetimes of many investors today – it is dangerous to establish outright short positions. Sure, valuation multiples such as price/earnings ratios might decline to levels more in line with historical averages, or perhaps even below. But share prices may not decline at all.

Most firms can pass some portion of input price increases through to consumers, at least in part, limiting the margin squeeze and growing earnings in nominal terms even if not so much in real, inflation-adjusted terms.

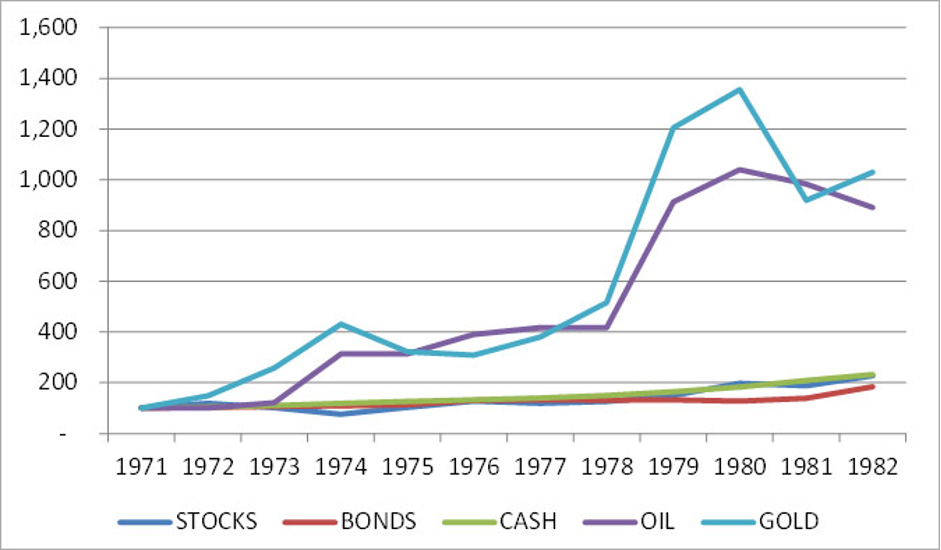

This was observed in the 1970s and early 1980s. Stocks may have done fairly poorly overall but, in nominal, broad market terms, they didn’t outright decline over the period. That said, both stocks and bonds were soundly outperformed by commodities, as shown in the following chart:

Performance of US stocks, bonds and major commodities, 1971-1982 (Jan 1971 = 100)

Source: Bloomberg, US Federal Reserve

Source: Bloomberg, US Federal Reserve

Exiting the market entirely and waiting for prices to decline necessarily becomes an issue of timing. In a low-rate environment, in which real, inflation-adjusted interest rates are deeply negative, sitting in cash is an expensive decision which grows ever more so over time. The longer it takes for valuations to correct, the longer the investor is losing out to inflation.

Rotate within the market, not out of it

The better strategy in this sort of environment is to rotate within the market rather than rotate out entirely. In this month’s issue, I’m going to focus on one specific way in which investors can get defensive within the market while protecting themselves from inflation.

In brief, investors should invest low on the value chain.

This is where multiples are traditionally lower and intangibles tend to comprise only a small part of the overall asset base. Perhaps most important of all, this is the part of the economy which is least distorted by inflation and where it is easiest to pass price increases through to customers, protecting profit margins.

What do I mean exactly by “low on the value chain”? Let’s start with commodities – that is, raw economic input. All industrial processes must begin with raw inputs, which need to be gathered, refined, chemically and/or physically transformed and otherwise processed. Some combination of industrial technology, energy, labour and capital – plant, property and equipment – is required to carry out the processes, however basic, which produce the output.

The output of the lowest value chain firms might itself be a low-level input, yet absolutely essential to other basic or more advanced industrial processes. Consider sulphuric acid, for example. It has nearly zero household uses. (Indeed, you probably shouldn’t have any lying about as it is dangerous, nasty stuff if handled inexpertly.) However, it is arguably the single most important industrial chemical when measured in terms of the overall amount of activity it facilitates including, critically, fertiliser production.

Much of the chemicals industry sits relatively low on the value chain. Do you recall the classic 1960s film The Graduate, starring Dustin Hoffman in the title role and Anne Bancroft? There is a scene in which a young university graduate unsure what career to pursue is speaking with an older, successful businessman who recommends that he get into “plastics”. (Plastics are part of the petrochemicals industry.)

That older man had a point. Almost non-existent over a decade before, plastics were in process of taking over the world in the 1960s. Today, of course, we take it for granted that practically all consumer goods and their packaging contain at least some plastics or synthetic fibres of some kind.

Incidentally, when my father graduated from university in the 1960s, he went to work for General Electric in its silicone products subdivision. While not plastics, which are made from hydrocarbons, silicones nevertheless are chemical industry products, with an astonishingly broad range of uses.

What all of the above have in common is that they are absolutely essential to economic life as we know it. Their manufacturing cost as a portion of the overall value chain into finished consumer goods might be tiny, but without them, there is no further movement up the chain at all.

What this means is that if inflation drives up the cost of sulfuric acid manufacture, or that of plastics or silicone products, those costs are going to be passed up the value chain, where they will eventually need to be absorbed by other firms, squeezing margins, or, alternatively, by consumers.

The “foundational” industries

There is a term for those industries that sit along the very bottom of all of the myriad value-added chains which comprise the capital stock of the global economy: foundational industries. These can be grouped into agriculture, fishing, forestry, mining/excavating and, in the modern, industrialised world, the energy to power whatever processes are applied to all of the above. Without these foundational industries, there is nothing to process at all; no value to add.

There may be little that is exciting about these industries to many. Indeed, given the trend in recent years towards “green” investing, basic industries have become something of an investment pariah. Investors with strict ESG guidelines – environmental, social and governance – might not even be allowed to invest much in the sector, if at all. But as these industries sit lowest on the value chain, they all tend to have strong pricing power and hence relatively stable margins. This makes them generally suitable as effective inflation hedges for the defensive investor.

Consider infrastructure and basic transport

While not considered a foundational industry per se, infrastructure, including basic transportation, sits nearly alongside the sectors mentioned above. There is little point to any of the foundational economic activities without the ability to move things around from place to place, or to store perishable products appropriately.

Imagine even a relatively simple economy trying to get by without decent roads, or grain storage facilities, or the ability to channel and move fresh water. Just consider the Babylonians, Egyptians and Romans: one key reason why these empires were so vast and long-lived is that they understood the importance of good infrastructure.

As one moves farther up the value chain, pricing power tends to decline. Manufacturers normally have some discretion regarding from which firms they source their basic material inputs. Wholesalers have discretion from whence they source their inventories. Consumers have discretion over precisely which product they buy, even for relatively non-discretionary items such as basic food and clothing.

As firms in markets with any meaningful competition face rising cost pressures, they seek not only to maintain profit margins but to maximise revenue. This means in practice that, as the pressure rises, the more cost-competitive firms will squeeze the margins of the less competitive. The overall portion of price increases that is absorbed rises accordingly. In some industries there is such a high level of competition that firms will even be willing to operate at a loss from time to time, if this is perceived to be a means to maintaining or acquiring greater market share.

Beware discretionary sectors

When it comes to discretionary items, including certain types of services, a highly inflationary environment can be devastating for corporate profits. Consumers facing a real income squeeze are going to economise. Rather than merely shop around for the best value, as happens with non-discretionary items, when it comes to discretionary goods, they might not shop at all.

The world of discretionary goods is also particularly fickle. The trends and fashions that continually compete for consumers’ discretionary incomes come and go. It is hard to know from one year to the next which product in which sector is going to be the “must-have”.

Those firms that can stay one step ahead of consumers’ preferences can be highly profitable. In last month’s issue I highlighted Coca-Cola as an example of a firm that has done astonishingly well at keeping its products up with the times, if not always ahead. There are many other examples but few with such global scope or longevity.

Today, the world of discretionary goods has a huge tech component, especially when viewed in valuation terms. Think Apple and Tesla, arguably two of the trendiest brands throughout the developed world, with enormous, highly subjective, intangible value. While most consumers no doubt need a smartphone or simple car, not one of them specifically needs an iPhone or Model X. Moreover, even existing Apple or Tesla customers might not be so keen to dip into their inflation-squeezed discretionary budget to upgrade frequently.

The valuations of both firms, and of the tech sector more generally, are pricey. For instance, the ratio of enterprise value (EV – the sum of a company’s market capitalisation and its net debt outstanding) to earnings before interest, tax, depreciation and amortisation (EBITDA – a widely used measure of operating profits) within the relevant sub-index of the S&P 500 composite remains at around 25 times – a high level by historical standards.

I continue to recommend that investors underweight large tech stocks or avoid them entirely. For those inclined to have at least some exposure to “Big Tech”, Microsoft and Google could be safer options as their growth is driven relatively less by consumer discretion and relatively more by the comparatively essential, almost utility-like nature of much of what they provide.

Building a defensive, low-value chain portfolio

Putting all of one’s eggs into one investment basket is never a good idea. Even in a challenging, environment of stagflation (i.e. a mixture of high(ish) inflation and low(ish) growth), investors should own more than just basic industrials and infrastructure. However, at the same time, investors should be aware that what is typically considered a “balanced portfolio” of, say, 60% diversified equities and 40% bonds is perhaps not so well-balanced for a stagflation. This is because both equities and bonds can lose value: the former due to compressing profit-margins and multiples; the latter due directly to inflation.

Therefore, a sensible approach would be to maintain a substantial equity allocation but rotate out of tech and discretionary sectors and into industrials and infrastructure instead. Utilities and consumer non-discretionary sectors could also both take a share of the reduced tech-plus-discretionary allocation.

When it comes to basic industrials, investors have a broad range from which to choose. For a start, they may consider prominent sector exchange-traded funds (ETFs). Within the FTSE, there is the basic industrials sub-sector for which there are ETF tracker funds. Other major stock markets also have investible basic industrials tracker ETFs.

When it comes to picking specific stocks, there are bellwether firms, many of which have been around for decades, with vast experience dealing with challenging economic environments such as that we are facing today. A few worth listing here would be BP, Shell, BHP, Glencore and Rio Tinto in the UK and Caterpillar, Dow Chemical, Archer-Daniels-Midland, Bunge and John Deere in the US.

For the other sectors mentioned above – infrastructure, basic transport and consumer non-discretionary – there are also a variety of prominent tracker ETFs. As infrastructure and transport firms tend to be regionally focused, there isn’t much available in terms of truly global bellwethers.

An exception here would be FedEx, which operates nearly everywhere and derives a substantial portion of its revenues from emerging markets.

As for consumer non-discretionary, global bellwethers could include Unilever, Johnson & Johnson and Procter & Gamble. Here in the UK, the major supermarket chains are also an option.

Speaking of the UK, while not exactly a non-discretionary activity, going to the pub comes awfully close. And to the extent that pub-goers are seeking to stretch their inflating pounds into as many pints as possible, and hopefully into at least a little food alongside too, it is worth considering investing in the major UK pub chain operators. The UK’s largest pub chains generally aim to make both food and drink as affordable as possible, taking advantage of their economies of scale.

Their shares have generally been beaten up hard during the past two years, losing nearly as much as half their pre-pandemic value. If it is indeed the case that the UK is exiting lockdown restrictions for good, this appears increasingly unreasonable.

Don’t forget precious metals and miners

One of the most important actions to consider taking heading into stagflation is to add precious metals to a portfolio of financial assets. Gold and silver might pay no interest. However, they compare favourably with cash and bonds which may, in real terms, produce negative returns. Moreover, precious metals also don’t potentially go bankrupt or default, and their prices tend to at least keep up with if not necessarily outperform inflation over time.

As their prices also tend to move somewhat independently of both stocks and bonds, they increase the diversification benefits of a portfolio and stabilise returns. A simple exercise in passive portfolio analysis demonstrates this.

Looking at the past few decades, adding 10-15% precious metals to a portfolio of stocks and bonds reduces the volatility without sacrificing anything in returns. Looking longer term, including the dreaded, stagflationary 1970s and early 1980s, a material precious metals holding would have substantially enhanced returns.

While both gold and silver can be owned outright for minimal storage costs or through an ETF tracker, there is also the option of investing in miners. As these share the pricing-power characteristics of basic industrials generally, they have defensive, essentially inflation-proof properties, and the valuation of the sector at present is not particularly high. (Newmont, the largest US-listed gold miner, has an EV/EBITDA ratio of under 10.)

However, it is only the mature miners with proven resources which tick all of the defensive boxes. They may offer less potential upside than junior firms in the event of a large precious metals bull market, but such is the nature of the risk-return trade-off in precious metals miner investing.

Last year, precious metals performance was disappointing given the context of rising inflation. I consider it possible that the ongoing crypto craze may have provided a headwind for a time. If so, that headwind may now be dissipating as the crypto sector undergoes a correction.

Meanwhile, real interest rates remain deeply negative. Whatever happens in the crypto world, this represents a tailwind for precious metals tailwind which could well prevail over the course of 2022. Moreover, the recent rise in energy prices implies higher input costs for miners. While that might be an issue in a sector without pricing power, precious metals miners can easily pass that on, occupying as they do, a place low on the value chain.

John Butler

Editor, The Fleet Street Letter Monthly Alert

PS Care to comment on the above? I’m always interested in thoughtful feedback from my readers, so please send me a note at editorial@southbankresearch.com and I’ll try to respond to any queries.