The real investment opportunity that AI presents to UK investors

23rd February 2023 |

In last month’s issue of Frontier Tech Investor, we introduced you to a new consumer-facing technology in our section, “Big breakthroughs”.

That technology was ChatGPT, which has taken the world by storm. It is the first really exciting proposition in “artificial intelligence” – AI – that the world has ever seen…

… or so the mainstream (and social) media would have you believe.

The reality is much further from this than most would care to recognise.

Actually, if you want to know why something like ChatGPT has been an overnight success (so to speak) then you should head back a decade.

What is AI and why did this overnight success take ten years to reach us?

I (Sam) have been covering the developments in AI for the better part of a decade now. Some of my earlier work looked at the implications of the (now defunct) BRAIN project funded by the US government’s Defense Advanced Research Projects Agency (DARPA). I also covered work undertaken by Sir Tim Berners-Lee and Sir Nigel Shadbolt and then looked into the kinds of companies pushing forward AI research and development such as IBM and Nvidia.

In fact, it was in November 2013 that I wrote a research report on Nvidia discussing the work that the company was doing with artificial intelligence, noting that:

… [in mid 2013] Nvidia trumped Google and created the world’s largest artificial neural network.

As a point of comparison, Google used 1,000 CPU-based servers – about 16,000 CPU cores.

Nvidia in collaboration with Stamford Uni created an equally large network with only three servers… that’s right, three. But by the time they’d finished, Nvidia had 16 servers, all powered by Nvidia GPUs. The completed network was 6.5 times bigger than what Google had created.

This was only possible because of the key difference in using GPUs vs CPUs.

The point to all this is as we rely more and more on computing to process information. It’s vital to leading us to a world of more advanced technologies.

It might be in the form of weather simulations. It could be the Google Maps in your sat-nav. Augmented reality through your wearable tech as you walk down the street. And it might even be a key part of machine learning and artificial intelligence…

It was around this time I was also looking at the relationship between open-source data and its integration into advanced machine-learning technologies.

The conclusion that I drew was that we were entering a future not necessarily of “artificial” intelligence, but “augmented intelligence”.

That’s where, I believe, we are today and will remain for some time: but therein lie the opportunities for investors.

You see, it’s important not to get too swept up in the noise and commotion surrounding AI. Already we’ve seen alarmist and fearful reporting on the immense threats that AI poses to the world. The pessimists say that we will see it change the balance between people and computers: jobs will disappear as AI takes over.

It’s very easy to get swept up into the hysteria about it all. And to be fair, that’s in part due to the accessibility of ChatGPT.

However, what the media is seeing with ChatGPT is not necessarily what you’re getting.

As noted in last month’s section on ChatGPT, the “intelligence” part of the application is a bit of a grey area.

The truth is that it’s highly advanced when it comes to the synthesis and analysis of data and interpreting that into real-world language. It’s a natural form of advanced machine learning. But is ChatGPT intelligent? No.

Is it a fascinating tool that we can use to augment our own intelligence though? Yes.

And when you make the distinction between AI and augmented intelligence, we think that you’ll see ChatGPT for what it truly is: you will see its potential and limitations.

As we see it, it is not necessarily the “pure-play” AI companies that have the real potential for the long term.

No: the real opportunities come from companies that are already on a solid footing financially, relatively unknown and able to supercharge their businesses by applying AI.

This month’s recommendation is a good example of such a company. It is CentralNic Plc (LSE:CNIC).

Dominating how we identify online

CentralNic Plc is a UK company, listed on the London Stock Exchange. The company is a web services and domains business that has grown over the years through a strategy of organic growth but also a number of acquisitions (20 at current count according to the company)

To give you an idea of some of the services that the company provides, we can take a look at the brands that exist under the company (some links are provided below to the sites).

- Only Domains – a platform that provides access to domain name registration, website development, email services and web security. It serves over 300,000 customers according to the company.

- CentralNic Reseller – a platform for the reselling of TLD (top-level domains) including a full automated system for domain registration and management.

- BrandShelter – a platform that provides domain management and security – notably by helping to monitor infringing websites, acquire relevant brand domains from third parties and register domains to protect a brand.

- Zeropark – an advertising and marketing platform without relying on cookies, to help brands reach new customer channels. Some partners include, Nike, Target, Adidas, Klarna, Afterpay and Etsy.

- TeamInternet – traffic and domain platforms to help customers monetise domains and buy and sell traffic for advertisers.

- CentralNic Registry – a TLD registry platform for domain registration and management.

In short, CentralNic is one of those companies that play important roles in enabling the internet to function, while being one that you have probably never heard of.

The ability to have an identity online, be it as an individual or as an organisation, has never been more important. Furthermore, ensuring that you’re found, that people can reach you, and that people can learn about you is an increasingly difficult task.

CentralNic helps customers find their online presence, manage it effectively and then to go on to maximise the monetisation of their online presence.

At its core, CentralNic’s business is strong, profitable (which we’ll get to) and has key relevance in an ever-increasingly digital world.

But it’s something that the company pioneered (in 2021) that we think holds the key to unlocking the full potential of the company. CentralNic has the ability to be a much larger and better-known business.

When AI and the internet meet

In July 2021, CentralNic announced that it was creating a new in-house division dedicated to data and AI.

This group would be headed up by chief data scientist Dr. Pawel Rzeszucinski – an expert in data and AI.

As the company explained in the announcement:

CentralNic stores, manages, and is exposed to huge datasets that can be used for advanced analysis. Examples include; navigation data on tens of millions of daily DNS queries, ad-tech data on tens of millions of domain advertisements, site usage data on hundreds of millions of unique visits and millions of monthly clicks, and similarly extensive data on transactions and registrations.

These extremely large data sets lend themselves perfectly to AI and machine learning applications that can be used to provide a large array of initiatives which will benefit both the Company and our customers. These include; improved customer service, optimised business operations and decision making, enhanced marketing, reduced customer churn and automated detection of non-compliant customer activity.

Now the obvious question might be, how does AI and a domain and web services company fit together. So let me give you a demonstration.

Have you ever tried to register a domain? Have you ever tried to come up with a domain for your organisation? We have, and we can tell you this: it’s not easy.

First you need to come up with a name. Then you need to go to a domain name registrar (like Only Domains) and type in your domain to see if it’s available. However, what then if the domain is taken? You then have to go back and start again.

What if the implementation of AI into domain registration was a reality? ChatGPT gives a clue.

We decided to ask ChatGPT a simple question which you’ll see below, along with its answers.

Can you come up with 10 available domain names for our financial newsletter, Frontier Tech Investor, which are interesting, catchy and not too long?

Sure, here are 10 available domain name suggestions for Frontier Tech Investor newsletter:

FrontierTechInvestor.com

FintechFrontier.com

FutureFinanceInsider.com

TechInvestorNews.com

FrontierMoneyMakers.com

TheTechInvestorClub.com

NextGenFinanceInsights.com

FrontierWealthInsider.com

DisruptiveFinanceDigest.com

TechInvestorHQ.comCan you give us another 10 that are a bit more exciting?

Sure, here are 10 more domain name suggestions for Frontier Tech Investor newsletter that are a bit more exciting:

FutureFortunesHQ.com

TechTrendTitans.com

CuttingEdgeWealth.com

MoneyMintingMavericks.com

FrontierFinTechFrenzy.com

BoldFinanceInsider.com

TechInvestorNation.com

WealthRevolutionary.com

NextGenMoneyMoves.com

FrontierInvestmentForge.comHow about 10 more that are one word long, or a made-up word that sounds like a real word?

Sure, here are 10 domain name suggestions for Frontier Tech Investor newsletter that are one word long or a made-up word:

Fintechster.com

Innovestiq.com

Investoryx.com

Futurenova.com

Techstox.com

Wealthpiloty.com

Trendvise.com

Prospexa.com

Frontechic.com

Disruptrix.com

Now, all we have to do is choose one – and then register it. That’s a lot easier than registering a domain has been in the past. And this is the kind of thing that, we believe, CentralNic will look to add to its services and offerings in the future.

Further, we believe that if CentralNic can integrate AI in a way that not only finds the right domains, but then automated the registration and construction of the brand around that domain, it could unlock a profit centre that could take the company to new heights.

Of course, right now, this is speculation. There’s no concrete strategy by the company to integrate AI in this way. And what you see above is an example of what AI and domains could look like.

Nevertheless, we believe the company wouldn’t dedicate an entire division with a world-renowned data and AI scientist if it wasn’t serious about bringing AI into its offerings. That’s why we think CentralNic is a perfect way to get a strong footing in internet services but also AI.

Strong financial position

As mentioned earlier, CentralNic is a profitable company already, before it gains any benefit from incorporating AI into its business.

The most recent financial report is for the nine months to September 2022, released in November 2022.

It shows the company increased revenues by 88% compared to the corresponding period a year earlier. Gross profit rose to US$128 million, a 53% increase from the year prior. Operating profit was US$35 million, with a reduction in expenses of 8%, and a reduction in net debt of 22%. Earnings per share (diluted) was 2.41 cents.

The company is in a strong, financial position. It is cash flow positive from operating activities and is using that money to grow by acquisitions. It’s a strategy that we believe sets it up for future growth.

And as noted, if it’s able to boost efficiencies and services by using AI-based strategies, the perceptions and reality of CentralNic should improve.

Risks

Growth in earnings and cash flow depends on two things. One is ongoing organic expansion of what is a stable business. The other is successful execution of acquisitions.

The main risk is that one or both of these outcomes does not happen. Expectations would be harmed. Since the beginning of 2020, the stock price has grown from about 85p to 129p. The process could go into reverse if investors were disappointed.

In addition, it’s important the company does show some positive financial impact from its investment in data and AI.

While the company does have a valuation currently around £376 million, it’s by no means a large cap stock: nevertheless, it is one of our bigger plays. And it does carry a high valuation based on earnings, which – as noted – could get punished if forward momentum isn’t maintained.

Still, CentralNic is already profitable. It has a great business and a great strategy – and the potential to leverage AI into its existing business mix offers enormous potential.

Action to take: BUY CentralNic Group Plc

Ticker: LSE: CNIC

ISIN: GB00BCCW4X83

Market cap: £376 million

52-week high/low: 160GBp/106.5p

Buy up to: 153GBp

Source: Yahoo Finance

Source: Yahoo Finance

Big breakthroughs

At the back end of January, the Green Energy Transition took what might one day be seen as a giant leap forward.

Though it went largely unnoticed by all bar a few industry publications, a 26 January announcement of a deal between a secretive start-up by the name of Form Energy and US utility Xcel Energy potentially puts the world on the threshold of a breakthrough in answering unarguably the most critical issue associated with renewables…

… how to store energy from wind and solar when the wind isn’t blowing and the sun isn’t shining for many hours, if not days, on end.

So-called long-duration energy storage – defined as a system that can store energy for more than ten hours – is often called the Holy Grail of clean energy.

It is the linchpin technology that will provide flexible, affordable renewable energy at scale, allowing the economy to run off intermittent energy sources 24/7, including backing up power after any grid disruptions.

While lithium-ion batteries will play a dominant role in the electrification of transportation, it has long been clear that longer duration grid-scale energy storage will likely need a different battery.

That’s because lithium-ion batteries – which have dominated new long-duration storage up to now – can rarely deliver their full power capacity for more than a few hours, are prone to catch fire and see their capacity diminish the more they’re used.

However, in the announcement at the end of January, Xcel said it was testing Form Energy’s novel iron-air battery tech at a scale bigger than nearly any battery plant on earth.

Form’s iron-air battery is designed to store clean energy, affordably, for 100 hours, or far more than the four or so hours of storage that lithium-ion batteries provide today.

Iron-air batteries work similarly to lithium ion batteries – you put the energy into the battery, the battery holds the energy, and then you discharge it. But inside the battery the system turns sheets of iron into rust and then back into iron as a means of energy storage.

Form Energy’s core technology – which is slower to charge, and thus slower to discharge – is based on three cheap and readily available materials: iron, air and water.

By using these inexpensive materials, the company aims to have its batteries cost less than $20 per kilowatt-hour, which is up to one-tenth the cost of the more common lithium-ion batteries in use today.

If the company gets near its $20/kWh target, in combination with longer duration… well, that is truly transformative.

The potential here is enormous.

Every hour we add of affordable storage is a step we take towards making utility-scale wind and solar facilities true 24/7 powerplants.

Iron-air batteries were actually studied in the 1970s for potential use in vehicles, but as they lost more energy to the process of energy storage that application didn’t work out.

But they now start to make serious sense in times of renewable energy curtailment. Although some energy is lost in the process, iron-air batteries have the capacity to capture and store energy for multiple days – something that is still far too costly with lithium-ion technology.

Xcel will place two of these long-duration energy storage systems at two different coal plants slated for retirement – Comanche Generating Station in Pueblo, Colorado, and Sherburne County Generating Station in Becker, Minnesota.

Modelling showed that the iron-air battery tech would help Xcel integrate higher shares of renewables, including wind. Meanwhile, storage systems can also enhance the resiliency and security of electricity supply. This includes during extreme weather conditions like, say, a polar vortex or winter storm, as well as in day-to-day, week-by-week and seasonal variations in weather.

Each Form Energy project will provide 10 megawatts of instantaneous power for up to 100 hours, meaning they each will store a total of 1,000 megawatt-hours. This makes them among the largest in the world in terms of the total amount of energy that they can store.

Both projects should come online by 2025, pending regulatory approval.

Saying that, there’s still a long way to go.

Many start-ups claim to be building long-duration storage, and Form Energy hasn’t publicly demonstrated its technology or shared proof that it really works.

But, if the claims are to be believed, then Form Energy stands almost alone in the realm of delivering clean energy for 100 hours or more.

That’s perhaps why the company has already lined up more than $360 million in funding.

Although we’ve had a few false dawns in long-duration storage before, investors, undoubtedly, can still see that getting beyond the four-hour constraints typical to lithium to, say, one or two days of cheap, clean storage, would be a major, transformative step.

We wait for further news.

Buy List update

Central Asia Metals (AIM: CAML)

Copper producer Central Asia Metals (AIM: CAML), recommended in the previous issue of Frontier Tech Investor, rose to 292.5p in early February but has since sold off to just 266p currently, down around 4% from our entry price of 276p.

Copper prices have lost a little steam since the beginning of February amid a softer-than-anticipated recovery in China, one of the world’s biggest copper consumers. Copper reached $9,356 per metric tonne on 23 January on the back of expectations of rising demand in China after the country reopened following strict Covid-19 lockdown measures.

At the time of writing, copper was last seen slightly lower at just above $9,000/mt.

Fortescue Metals Group Limited (ASX: FMG)

Australian iron ore giant and green hydrogen hopeful Fortescue Metals Group Limited (ASX: FMG) continues to trade around AU$23, putting it around 32% up in the buy list at the time of writing.

The company released half-year results that saw revenues decline 3.6% in H1 FY23, compared to H1 FY22. The company also announced an interim dividend of AU$0.75 per share compared with AU$0.86 declared a year ago.

The miner flagged that inflationary pressures will continue to be a risk for the remainder of fiscal 2023. On a more positive note, the miner achieved record half-year iron ore shipments of 96.9 million tonnes (Mt), beating the prior record first half set in H1 FY22 by 3.8Mt.

The world’s fourth-biggest iron ore miner also offered fresh detail on its plans to develop a global green hydrogen business.

It is due to make a decision this year on five projects that it will develop and one of those is likely to be in Texas, according to Fortescue Future Industries CEO Mark Hutchinson.

Fortescue said it has also commissioned its first two big battery storage installations at its Pilbara iron ore mines, and begun construction on its first big solar farm, as it accelerates its switch to green energy.

Rize Sustainable Future of Food UCITS ETF (LON: FOGB)

Trading at around 364p at the time of writing, the Rize Sustainable Future of Food UCITS ETF (LON: FOGB) sits under our 378.48p entry price, having fallen from over 382p in early February.

The ETF currently has 51 holdings involved in the production of sustainable food and packaging, with plant-based foods, precision farming and fertiliser manufacturers among the targeted sub-sectors.

Sharp price drops of companies in the ETF, such as Beyond Meat and Tattooed Chef, since the start of the month have pressured FGOB despite the underlying theme continuing to gain momentum.

According to Swiss private bank Lombard Odier, the paradigm shift towards new food systems creates multiple growth opportunities that represent an annual turnover of $1.5 trillion worldwide by 2030.

Foresight Sustainable Forestry Company (LON: FSF)

Foresight Sustainable Forestry Company (LON: FSF), which invests in UK forestry and afforestation assets, has gained 4% over the last month, though it still currently sits 4% under water in the buy list.

On 19 January, it said its June 2022 equity fundraising proceeds were now fully deployed following the completion of 11 acquisitions. The trust said it had deployed a further £19.2 million into nine afforestation properties and two forestry properties, ten of which are in Scotland and one in Wales. The acquisitions increase the portfolio by approximately 1,464 hectares, meaning FSF’s total portfolio now covers 11,215 hectares.

It also said it has now secured the necessary planning permission, full consents and grant contracts for three Scottish afforestation properties in the portfolio. Planting at Upper Bar, Auchensoul and Redding Farm is expected to start imminently and is scheduled to complete at all three sites before the end of April 2023, FSF said.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF (LON: LITG) has fallen by around 3% since mid-January to £9.33. However, it’s still around 5% up in the buy list at the time of writing. LITG holds companies such as Tesla (TSLA) and Albemarle (ALB), which are involved in the global mining and exploration of lithium, or in lithium battery production.

Electric vehicle (EV) battery stocks have largely had a good start to the year amid resurgence in growth stocks and as policymakers in the United States and other regions look to stimulate investment in batteries and EVs. On 14 February the European Parliament formally approved a law to effectively ban the sale of new petrol and diesel cars in the European Union from 2035, aiming to speed up the switch to electric vehicles and combat climate change.

The landmark rules will require that, by 2035, carmakers achieve a 100% cut in CO2 emissions from new cars sold, which would make it impossible to sell new fossil fuel-powered vehicles in the 27-country bloc.

Aurubis AG (DE: NDA)

Germany-based copper smelter and recycler Aurubis AG (DE: NDA) has risen from under €92 in mid-January to €93.86 now, now standing 39% up from our entry point.

Aurubis posted a fall of about 24% in quarterly earnings on 6 February, attributing the decline to the impact of inflation and increased energy prices, though it maintained upbeat earnings estimates for its full-year profits.

Aurubis posted operating earnings before taxes (EBT) in the first quarter to end-December of its 2022/23 financial year of €125 million, down from €164 million in the same year-ago quarter.

But the company confirmed its December forecast of full-year 2022/23 operating EBT of €400-500 million. There is continued high demand for Aurubis’ products, CEO Roland Harings said.

Newmont Corporation (NYSE: NEM)

Newmont Corporation (NYSE: NEM) rose above $55 in late January though subsequently fell back to around $45, 31% down from our $65.39 entry point.

In early February, US-listed Newmont, already the world’s largest gold miner by output, launched an all-share bid for its Australian rival Newcrest that values the smaller company at almost A$24 billion.

A combination of rising costs in Australia’s mining sector, production issues for gold and volatility in its price amid sharp rises in interest rates has increasingly driven companies to consider deals to boost their scale.

Newmont’s offer for Newcrest would be the largest M&A deal announced so far this year. The deal would also increase Newmont’s footprint in copper, which, of course, is becoming more sought after due to its use in renewable energy and EVs as economies de-carbonise.

Although Newmont’s proposed merger with Newcrest is likely accretive to earnings on a long-term basis, it does raise the risk of a potential dilution risk to shareholders, hence the sell-off after the release of the news.

We are keeping our eyes peeled on developments and will update if necessary.

Norsk Hydro (OL: NHY)

Norwegian aluminium producer Norsk Hydro (OL: NHY) has inched a touch lower over the last month: it is now trading around NOK 78.35, still 17% up in the buy list.

On 14 February Norsk Hydro said that inflationary pressures in 2023 are likely to subside, though the outlook is “unpredictable”, as it posted a bigger-than-expected fall in fourth-quarter core profit.

The stock remains a buy up to NOK 100.

SDCL Energy Efficiency Income Trust (LON: SEIT)

SDCL Energy Efficiency Income Trust (LON: SEIT), an investment company focused on assets in the energy efficiency sector, which rose to over 110p in November, was last seen hovering above 91p, 7% down from our entry point.

SEIT invests in technologies including rooftop solar, energy storage, combined heat and power and industrial energy recycling in buildings ranging from data centres to hospitals, schools and universities, and high-emission steel and chemical industrial facilities.

It also funds projects that reduce demand for energy at the point of use, including improvements in lighting, heating, ventilation, air conditioning, building energy management systems and controls.

SEIT continues to trade at a discount to its NAV, meaning that, right now, it costs less to buy the shares than the underlying investments are worth, a situation that should eventually reverse as energy efficiency measures gain in popularity.

After all, these measures are cheap, achieve rapid results and already attractive payback times have been slashed further by rising oil and gas prices.

DS Smith (LON: SMDS)

At 330p, sustainable packaging solutions provider DS Smith (LON: SMDS) now stands 6% up from our entry point after falling from 369p at the start of February.

It hasn’t released any news over the last month, though it continues to look to be good value, trading on a forward price-to-earnings ratio of just 8.94 and yielding a healthy 4.82%, covered twice by earnings.

It remains a buy up to 400p.

Lyxor World Water ETF (LON: WATL)

Lyxor World Water ETF (LON: WATL), which allows investors to track the world’s largest companies involved in water supply, water management and treatment, has risen from £45 on 20 January to £47.20 now, putting it 4.5% up in the buy list.

The ETF has found support from strong performance from its two largest constituent holdings: plumbing and heating products distributing company Ferguson Plc and plumbing supplies maker Geberit AG, which together comprise over 15% of the ETF.

Ferguson, in particular, has been on a tear, gaining 33% since 3 October alone. It serves a variety of end markets in North America, including residential, commercial, industrial, and government and infrastructure. It recently authorised a $2.5 billion buyback programme, which equates to around 7% of the company’s current market capitalisation.

Watsco Inc (NYSE: WSO)

Heating, ventilation, and air conditioning (HVAC) distributor Watsco Inc (NYSE: WSO) has moved back into positive territory in the buy list, gaining around 13% over the last month to $306.30, 4% up from our entry point.

Watsco continues to generate attractive sales, profits and cash flow growth and should benefit from favourable industry dynamics, including from the Inflation Reduction Act in the US.

On 16 February, the company announced a surge in fourth-quarter earnings from the prior year.

The Miami-based company reported quarterly earnings of $137.67 million, up from $78.89 million last year. Revenue for the quarter was $1.581 billion, up from $1.511 billion in the same quarter last year.

Meanwhile, the company said its board has authorised an 11% increase in annual dividend rate effective in January 2023 to $9.80 per share.

Yara International (OL: YAR)

Yara International (OL: YAR), one of the world’s largest producers of nitrogen-based mineral fertilisers, now trades around NOK 477.40, up from NOK 440.20 on 25 January, putting it 16% up in the buy list.

Shares of Yara rose after the fertiliser maker beat quarterly earnings forecasts and annual dividend forecasts in an announcement on 8 February.

Higher fertiliser prices have helped to offset a surge in gas prices that led it to curb output last year.

October-December earnings before interest, tax, depreciation and amortisation (EBITDA), excluding one-off items, rose to $1.07 billion from $765 million a year earlier, the company said. Analysts in a company-provided poll had expected a profit of $988 million.

The company also proposed an ordinary dividend of 55 crowns per share for 2022, up from 30 crowns for 2021 and ahead of expectations of 47.14 crowns.

Inside the lives of James and Sam

Sam:

It’s been a hectic month in the life of yours truly. Not long after we sent out our last monthly, I jetted off to Australia for a family wedding. I flew out on a Saturday and landed back in the UK ten days later.

The good thing about trips like that is the fact you don’t have time to adjust to the time zone differential: you just suck it up, drink all the free grog that is available and get on with it.

Yes, that’s right, Australian weddings are fully catered for: that means, free food, free beer, free (and very fine) wine and, in this particular example, free cocktails and whisky.

Meanwhile, if you’re at all wondering what Sydney (more specifically Bondi Beach) is like at the start of February…

I also managed to watch a definition of insanity from this vantage point at the Icebergs pub. The (empty) Icebergs’ pool in that picture was actually in the middle of being repainted white that day. The only problem was that as the surf was barrelling in, it would splash over the side of the pool and wash away the paint the poor fellas had just applied. I think they just gave up and waited for low tide.

I also got some sage advice from my brother about fermented grape juice while I was out there. As you may or may not know, I like wine. I’ve got a few top-quality ones that I had thought about keeping for investment purposes, but then also I have a bad habit of drinking them too.

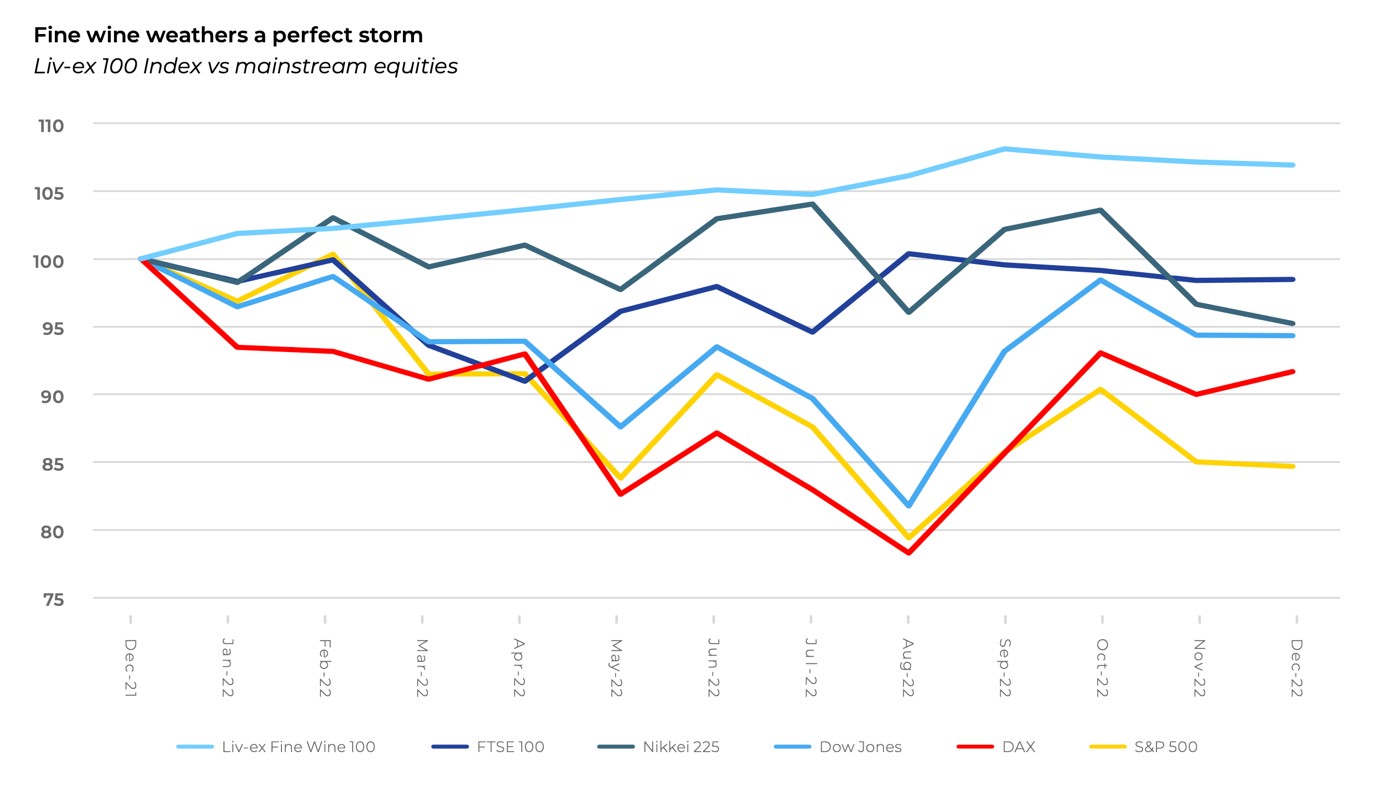

Now… wine investing can work quite well. In fact, WineCap’s Q4 2022 report shows that the Liv-ex Fine Wine 100 index outperformed the FTSE 100, Nikkei 225, Dow Jones, DAX and S&P 500 from December 2021 to December 2022.

Source: WineCap Q4 2022 report

But if, like me, you have a habit of drinking fine wine, then this all turns to dust pretty quickly. My brother wisely told me to just forget about the current prices of the wines in my cellar:

“Drink them based on the price you paid for them.”

Now that is sage advice.

This all came to a point when I was at my uncle’s house whilst in Australia. A while ago (about 15 years I’d say) I was at a function with my uncle and they had a blind raffle for wine.

All the bottles were in brown paper bags, so you couldn’t tell what was what. All of them were $20 bottles of wine… except one. One was a 1995 Penfolds Grange, that most iconic of Australian labels.

I went up and bought two, for a $40 entry fee. I grabbed two of the bottles and headed back to my table with my uncle. I told him to pick one, which he did. You can see it below…

My uncle promised me that we’d drink it one day… perhaps after the birth of my first child. This was before I’d even met my wife, let alone had two kids.

I thought he’d drunk the bottle long ago. So when in Sydney I found out it was still intact, I was all over it. We had to drink it. But then he got inside his own head… and some peer group pressure from others.

They kept thinking and saying this was a £400 bottle of wine, that it needed to be drunk with others, savoured and enjoyed for all. I tried to educate them to the folly of this approach.

This was not a £400 bottle of wine, but a $20 bottle of wine, and should be drunk as such, as in right now!

I was overruled.

So, the bottle of ’95 Grange remains unopened and undrunk. I, on the other hand, am unimpressed – and just to prove a point, I may just buy a bottle myself and drink it out of principle.

What would you do? Buy and drink… or buy and invest when it comes to fine wine? I know what I’ll be doing!

James:

I detailed a major stress enveloping my life in this section last month. This month I write of a new hobby that has done more than perhaps anything else to clear the head and take the mind off worrying about any of life’s uncontrollables: learning the piano.

That’s right. My little family and I have spent most evenings over the last month immersed in an online piano learning course that is both great fun and proving an incredible way to learn an instrument that always looked – to me at least – dauntingly hard.

I mean, I had a few lessons as a kid, but never really improved much beyond the one-fingered-bandit stage. So, when a friend asked me a few weeks ago whether I’d like an electric Yamaha piano his wife was about to throw out I thought it would be a great thing for the family to learn all together.

And it has been brilliant. We were recommended a downloadable app called Simply Piano, which we play on an iPad perched above the digital piano (itself perched above an old piano that is so out of tune and missing so many keys that it’s unplayable). The app responds to the piano’s microphone and interprets our playing in real time. We’ve created profiles for all of us so we can learn at our own speeds.

The course has a strong focus on getting beginners off the ground quickly, and it’s amazing to see how we’ve all improved so much in such a short period of time. The first lessons take a sort of quiz-like form, asking you to play the notes that pop up on the stave. It’s worked wonders. I’ve already learnt to sight read both treble and bass clefs, and my left hand is now an apprehensive but increasingly willing party to proceedings – which is a stage I thought I’d never get to.

I’m still on the beginners’ “Essentials” stage, so I’m a long way to being what you might call competent, but I’m getting there. I can now play “Imagine” by John Lennon, “Careless Whisper” by George Michael and a couple of Imagine Dragon songs that my stepson is much fonder of than I am. I’m eager to get to the Elton John and Billy Joel stage.

Overall, it’s incredibly rewarding to see and hear visible signs of progress and it’s also been great to bring the family together in one shared communal activity. I always thought the idea of “family fun” was a slight misnomer (always involving at least one family member traipsing along, either literally or proverbially): however, this app has been genuinely brilliant fun for all of us, with plenty of singing along to accompany the ivory basher at work. It’s highly recommended.

Elton John in the making…

Crypto Corner

What a wild month we’ve had in the crypto markets… as per usual.

What’s fascinating about the market right now is that the waves of negative news continue to flow over the industry. However, the bad news appears to be having very little impact on prices – which have been rising.

For instance, reports in the last few weeks have highlighted:

Kraken’s staking services had been legal. So the US government banned them. Unsurprisingly:

Yes, that’s right, once the US government acted, HM Treasury – on this side of the Atlantic – decided that this might be something it’s interested in too.

This is what happens folks when people ask for “more regulation” in crypto markets – you end up getting what you wished for but worse.

Truth be told, regulation is good, so long as it regulates bad actors out of business and enables good actors to go about things the right way.

But since when has regulation ever not been overreaching, not too invasive and genuinely promoting of progress rather than stifling progress?

Yes, that’s a rhetorical question…

In short, if you’re a crypto business then you’re going to get regulated like a financial services business. And perhaps you should be. After all, when you boil things down to their bare bones, these so called crypto “exchanges” are financial services businesses: they should be treated as such in order to ensure that consumers are properly protected.

What is clear though from all the reports out of the United States and the UK on staking is that there’s a significant knowledge gap between what the authorities think they know and what they actually know about it all.

I think what we’ll end up with is a situation where dollar-denominated stablecoin staking products will be treated as financial products. That actually makes sense.

But for native stakers, people like you or me, who choose to own a crypto, self-custody that asset and then enable staking from our own wallets – that will be just fine. After all, that’s an important part of just enabling proof-of-work blockchains to continue to function as intended.

Some water is yet to pass under the bridge: however, if you were to ask me right now am I concerned the authorities are going to ban staking, I’d tell you that I’m not worried.

However, it is a problem for businesses that are offering staking as a service but who are not yet properly authorised to offer financial products.

Speaking of dollar-denominated stablecoins, the US government is also taking aim at Paxos, a stablecoin issuer. In fact, the US government says that it is aiming at Paxos, but appears to be looking to put a shot across the bow of Binance:

- Paxos ordered to stop minting BUSD and is under investigation by the New York Department of Financial Services

I think the key point that regulators are missing with this Paxos investigation is that stablecoins in US dollars are only that way because they were easy to create and to use. Now there are loads of different stablecoins elsewhere in the world, denominated in euro, Australian dollars and sterling. If the US government is overly heavy handed in its approach to US dollar stablecoins, then stablecoin users will shift their attention to another fiat-currency backed offering.

That’s the beauty of a free market working efficiently: the capital is free to move wherever it wants to and can be most productive.

As mentioned above, this is all happening in the context of the price of bitcoin shooting up to just under $25,000 and the wider crypto markets continuing an obvious trend higher.

What I’m seeing now is pretty closely following the 2019 playbook. That implies that crypto prices will move higher over the remainder of the year, but with some inevitable pullbacks.

In the event that the price of bitcoin streaks past $40,000 and looks as though it is heading towards $60,000, then watch out for the return, in a big way, of retail investors’ Fear of Missing Out – or FOMO.

In every single crypto winter, the number of people who proclaim that the market is dead and that crypto is a scam multiply. Their voices get louder, and then they eventually are proven wrong. I don’t see this cycle being any different to the previous ones.

So you can believe a doomster like Charlie Munger of US investment firm Berkshire Hathaway – who by all accounts would consider me an “idiot”. Alternatively, you can take a look at what’s staring you in the face with the crypto opportunity.

I mean, how possibly could Mr Munger possibly understand how the market works, when this is how crypto functions…

The crypto market in three pictures…

Source: Twitter

Source: Twitter

Source: CoinGecko

Source: CoinGecko

Source: CoinGecko

Source: CoinGecko

Take those images as you will. Laugh at them. Be amazed by them. But also consider that people are making lots of money from them.

Reader Questions & Answers (Q&A)

The new format of this publication is… interactive.

That means that we both encourage you to send in your questions.

Questions can be to either or both of us. They can be about stocks, a particular technology or industry, crypto, or a “boots on the ground” research mission.

Questions & Answers is a key part of the publication.

Given that we publish towards the end of each month, it may be difficult for us to tackle time-sensitive questions. It should usually be possible for us to address questions that are not time sensitive.

Please bear in mind that we can’t give personal advice. Also, if your question is related to anything operational, like how to change a password on your Southbank login or where to find a report, please get in touch with our wonderful customer services team.

When sending in your questions, please acknowledge you’re happy for us to republish it. Don’t worry: we won’t be using any names or initials, just the questions.

We can’t guarantee to answer all reasonable questions – particularly if we receive a huge number: however, we will do our best, and may follow up directly with you.

Please send them in: [email protected].

Question: James, will you still be covering new opportunities in climate tech in the revamped Frontier Tech Investor?

You bet I will! How investors can profit from the flood of money flowing into solutions to mitigate or adapt to the effects of climate change remains one the key investment themes of the publication. After all, in my opinion, all technology will soon be seen through the lens of climate change.

2023 is set to be a big year for climate tech, not least in the UK, given that climate tech investment in this country more or less doubled last year. In fact, the UK is second only to the United States for the number of companies working to address the climate crisis, with over 5,200 climate tech companies established in the UK to date.

There are lots of exciting opportunities on my radar that could turn into fully fledged recommendations as the year develops.

Question: James, are there any good opportunities to invest in nuclear fusion, where I understand there has been a lot of progress recently?

Late last year a US government lab announced a successful test of nuclear fusion, no doubt prompting a flurry of Googling from investors eager to speculate on fusion plays. Unfortunately, though, there aren’t any pure-play publicly traded fusion companies currently on the market, though that doesn’t mean to say there aren’t ways to invest in nuclear fusion, which is the fusing of two atoms to create energy.

For accredited investors who can access private equity or venture funds, then companies such as Helion Energy, Commonwealth Fusion Systems and Marvel Fusion are all active in the space.

Investors could also look at publicly listed producers and manufacturers in the materials sector, such as lithium or deuterium, or even potential users of the new technology, on the premise that big data centre companies such as Google and Amazon will eventually be huge customers for renewable fusion energy in order to save billions in energy costs.

But investors should remember that nuclear fusion is still an unproven technology without a business model and still years away from being commercially viable: the above comments should by no means be taken for investment advice or recommendations!

Question: Doesn’t crypto as a subject come under the banner of frontier tech investment? You have some blockchain mining positions in Frontier Tech Investor, but no Crypto (except for IOTA). Have you considered having direct crypto investments as part of the service?

Frontier Tech Investor is first and foremost a stocks advisory service. That means our mission is to uncover the best investments on the London Stock Exchange for UK investors. Now, yes, we have IOTA in the buy list which is a crypto – but it’s a legacy position from some time ago under a previous editor. And as it’s a position that currently we don’t want to sell, it’s still there.

Fundamentally, cryptos aren’t stocks so they really fall outside of the mission we have here at Frontier Tech Investor to invest in UK-listed stocks. So at this stage unless we get 20,000 people kicking our door down to provide an entry-level crypto advisory service, we won’t be bringing them into Frontier Tech Investor. However, we do still view the crypto investment idea as one we want you to be a part of, which is why we have the stocks rather than the cryptos that focus on the crypto market.

Question: Can you suggest a couple of Investment trusts that are overweight in artificial intelligence (AI) companies?

When we get question like this, there’s a limit as what we can say. We can’t give personal financial advice – and this kind of question does stray into that arena. However, that shouldn’t stop you from undertaking some extra research yourself into this area. And the good thing is that there’s some great tools out there you can use to filter funds that have exposure to the AI investment idea.

For example, if you’re in the market for exchange-traded funds (ETFs), etf.com is a wonderful resource where you can easily search for ETFs that have a specific theme. In this case, you’d go to ETF.com and search for AI and see what it comes up with. Then you can review the holdings, check with your broker if they offer the ETF and then decide after some further research. We may look to include an AI ETF in the future. Nevertheless, we prefer to find individual companies that appear to have the potential from new technology, such as AI. Normally, the possible upside from a particular name is greater than it is from a thematic ETF.

Question: I see a lot of videos where your talks about crypto as an alternative means of trading from being trapped into the failing system of fiat currencies and the 24/7 surveillance society like CBDCs. I have read before that crypto retail sales are banned in the UK. What does the team make of this? And do they have possible solutions to getting around it?

There’s a lot of confusion and misinformation about this in the UK. The regulators have not been very clear about the position on it all, but the answer is thankfully quite simple.

The Financial Conduct Authority (FCA) issued a ban in 2020 on the sale of crypto derivatives to retail investors. That means that things like CFDs, options and futures are banned for sale to retail investors in the UK. This does not mean direct sales of cryptos to retail investors are banned.

You can go to any exchange such as Coinbase, Binance, Kraken, Bottlepay (and many others) to buy crypto directly with your money. It is perfectly fine to enter the crypto markets this way.

What else we’ve been looking at this month

Sam:

When GOATs move the markets

Tom Brady recently retired from the NFL (again!). Lionel Messi declared he was retiring from the Argentinian national side after their World Cup win. LeBron James recently surpassed Kareem Abdul-Jabbar for the NBA all-time points scoring record.

These names all comfortably enter the equation when talking about GOATs (Greatest of All Time) in terms of their respective sports.

However, if we’re talking about the greatest GOAT of all time across all sports, I don’t think we can look past Tiger Woods (a completely subjective view here). His domination of professional golf from 1997 through the entirety of the 2000s is unrivalled.

Now, I’m sure that loads of people will disagree with me – perhaps you included. However, before you do, ask yourself this… have any other potential all-time GOATs ever moved the entire stock market too?

It’s hard to believe, but this article on Tiger’s performance at the 2008 US Open goes some way to reinforce my view that he’s the best athlete of all time and quite possibly the best there ever will be.

The rational brain

A friend sent me a link to this page during this month.

We had been discussing the spate of “UFO” news that was hitting the headlines during February and the inevitable conspiracies that followed. Add to the mix a weird laser show that seemed to be coming from the Chinese spy balloons, the earthquake in Turkey and Syria, and… well, things were getting weird.

Of course, “Project Blue Beam” is nonsense – but this particular site was good fun, especially with the description of journalist and conspiracy theorist Serge Monast’s head as “… quite thoroughly full of squirrels and confetti by this time.”

Whilst Project Blue Beam is an interesting read, it’s the Rational Wiki site that I found particularly interesting. It’s full of rational explanations for the world’s current “weirdities”– and those that have happened throughout time. It is well worth sticking in your browser bookmarks folder.

I’m on time/I’m late

Having been in transit recently, it’s hard to know if your flights are going to be on time or late – until, typically, the very last moment. That’s when you’re at the boarding gate and the board flashes up “Delayed” right as you think you’re supposed to be embarking into the plane.

The good news is that you can get ahead of this. When I travel, I always check the status of my flights using Flightradar24. It’s a site that shows every flight in the world – in real time. All you need is your flight number. From there, you can check the status of your flight and can even track the plane you’re flying on via its tail registration: that means that you can see where it’s been and if those previous flights were on time or not.

In other words, if the previous leg your plane is flying on is delayed, then you’re going to know about it before anyone. And you can even watch it land, prior to it being allocated as your flight. I find that Flightradar24 eliminates “departure anxiety” as I know at all times where the plane is, where it has been and if it’s on time or not. I highly recommend getting familiar with the app if you’re in the skies a lot.

James:

Directing the greatest leg of darts

My identical twin brother is a TV director at Sky Sports, and I’ve always liked grilling him about exactly what that entails, especially when there’s a big live event taking place. The final of the PDC World Darts Championship last month was no exception. This was the final that comprised perhaps the greatest leg of all time: 61 seconds of remarkable sporting theatre, even for non-darts fans, as viewers watched Michael Smith nail a nine-darter after opponent Michael van Gerwen missed the opportunity to seal his own. The final was also notable for some inspired commentary that elevated the drama to another level.

But, as my brother instructed, watch again and marvel at the skills of the TV director, too. Throughout the final, the director – a friend and colleague of my brother’s – had to make extremely quick decisions and anticipate where each player would throw on the board. Apparently, after studying each player, he knew exactly how each plays and what doubles they like to leave themselves with.

But for this leg, particularly, notice how, as it develops and the tension builds, the director chooses to go from split screen to full frame action so that the viewer can get good close ups and see the full reactions of each player. What’s even more impressive is that apparently the director not only directs the footage but vision-mixes (or cuts) it all himself too – all in real-time and all under the pressure of live TV.

Apparently, there were 50-odd cuts in the 61 seconds of the leg, which is incredible when you think about it, especially as the footage itself is seamless and totally in sync with the developing drama. (By way of comparison, my brother says you can easily go 20 seconds on a live football game without seeing any camera cuts at all.)

For me it was fascinating to hear just how “on” the director has to remain during the whole match, with no let up at all. The levels of focus are insane and there’s no breather; even after that brilliant moment of sport, with the viewing crowd both at the venue and at home in a state of frenzy, for the director, it’s straight on to the next leg.

Hindenburg Research 1 – 0 Adani Group

Losing $70 billion in a few weeks has got to hurt, no matter if you’re still left with a fortune worth $50-odd billion.

But such is the present fate of Indian billionaire Gautam Adani, who started the year as the world’s third richest man but is now languishing – though that’s hardly the correct term – down in 24th place.

The starting point of the fall – and it’s likely not over yet – was a research note from US-based investment firm Hindenburg Research that accused the Adani group of decades of “brazen” stock manipulation and accounting fraud.

Bonds and shares of the various Adani entities fell. Then they fell some more.

Hindenburg specialises in “short-selling” – betting against a company’s share price in the expectation that it will fall.

The Adani Group has denied and rebutted the allegations in the report, but that hasn’t been enough to stem investor fears. Hindenburg stands by the report and says that the Adani Group has “failed to specifically answer 62 of our 88 questions”.

What’s incredible is the David and Goliath element: Hindenburg Research, named after the 1937 airship disaster, is a tiny, relatively young New York financial research firm that’s taking on the Adani Group, until recently India’s largest conglomerate – and seemingly winning.

This fight has legs and I suspect many more punches will be thrown.

Theranos drama The Dropout details an investors’ nightmare

If you’re after a new series to watch on the box then you could certainly do worse than The Dropout, the new limited series on Disney Plus about the rise and fall of Theranos and its founder Elizabeth Holmes, the Silicon Valley darling turned convicted corporate fraudster. I’m partial to a based-on-a-true-story series and, after a sluggish start, this one soon had me racing through the episodes.

Holmes, you might recall, was recently convicted for defrauding investors in her blood testing start-up that was once valued at $9 billion.

The former billionaire falsely claimed the technology could diagnose disease with just a few drops of blood. But it did not work and – facing multiple lawsuits – the company was dissolved in 2018.

The Dropout chronicles the rise and fall of the start-up and you’ll watch it supremely thankful you weren’t one of the fleeced investors or, even worse, a patient who had believed what the tech falsely said it could on the tin. Watch the trailer here.

James Allen and Sam Volkering

Editors, Frontier Tech Investor