Your April issue of Southbank Growth Advantage

25th April 2024 |

- The most important acronym of the 21st century: HALEU

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

The most important acronym of the 21st century: HALEU

Recently we’ve been re-focused on the importance of nuclear energy. The reason being the rise in compute-hungry technology like next-generation datacentres and AI models means a huge swell of power is needed to keep these things running.

That energy needs to be reliable, constant and efficient. While current energy grids can contribute towards these current and future needs, they can’t be relied upon.

Furthermore, with geopolitical issues continuing to rage around the world, the concept of energy security at a domestic level has never been as important.

The way we see it, that energy security comes with the development and commercialisation of nuclear energy.

And that’s a future we expect will come to fruition. Namely through innovative, advanced reactors like those in development from Oklo and Rolls-Royce.

However, as we outlined in our report “The Uranium Bull Market Playbook”, nuclear energy is great unless you don’t have the right fuel for it.

Of course, that fuel for fission reactors comes in the form of uranium. And we’ve pinpointed ways to play the physical uranium market.

But there’s another slight problem with this. That comes in the way in which the nuclear fuel goes from being dug up in the dirt into an actual fission reactor in a nuclear reactor.

Driving Putin out of energy markets

Most new, advanced nuclear reactor designs require new kinds of nuclear fuel. Well, we say new, but the reality is it’s still uranium but a particular kind of enriched uranium in order to create their fission reactions… and hence energy.

There’s one kind in particular that’s known as high-assay, low-enriched uranium (HALEU).

As we explained in our nuclear stocks watchlist report, HALEU is an important kind of nuclear fuel.

Uranium is not ready to be used as a fuel as soon as it is mined. At that point, it contains very low amounts of the fissile material – uranium-235 – which is needed for combustion in a nuclear chain reaction.

The rest – more than 99% – is non-fissile uranium-238. As a result, the uranium needs to be enriched to be more effective, and current nuclear plants run on uranium fuel that is enriched up to 5%.

HALEU is enriched to a greater extent – between 5% and 20% – to allow new reactor designs to generate more power per unit of volume. HALEU will also allow developers to optimise their systems for longer life cores and increased efficiencies (such as with fuel use).

The Nuclear Energy Institute (NEI) surveyed US advanced-reactor developers in 2020 to produce an estimate of potential HALEU demand through 2035. And even if only a fraction of the demand in the NEI survey materialises, HALEU requirements would be very large.

At 25% of the NEI estimate, for example, the HALEU market could be worth $400 million per year by 2030 and $1.4 billion per year by 2035.

More recently the UK government even launched a £300 million investment into a HALEU programme, becoming the, “first country in Europe to launch a high-tech HALEU nuclear fuel programme, strengthening supply for new nuclear projects and driving Putin further out of global energy markets.”

See that last sentence? The bit about Putin. This is the attitude that countries like the UK and the US are taking (and rightly so) to ensure they’re not reliant on foreign supply of energy that is high-risk.

The US is taking a similar approach. It’s enacted the Energy Act in 2020 that also directly established the HALEU Availability Program to ensure research, development and commercialisation of HALEU production in the US.

Which leads us to your latest recommendation that has become the first new, US-owned, US technology uranium enrichment plant to begin HALEU production in the US in 70 years.

Introducing your latest Southbank Growth Advantage recommendation…

If you read our nuclear watchlist special report, this name will be familiar to you. We’ve been watching it for a while and feel that with developments and the potential of Oklo in the short term, the continuous rise of nuclear energy demand, and a key milestone this company only achieved in late 2023, now is the perfect time to bring Centrus Energy into our buy list.

Centrus Energy (NYSE American: LEU) is a supplier of nuclear fuel (in particular HALEU) and related engineering services to the nuclear energy industry.

It currently trades on the NYSE American market with a market cap of $657 million and a stock price currently around $40.40.

Centrus is an important developer of this HALEU fuel, and thus is central to American plans (and likely British plans) for the future of the nuclear industry.

Centrus Energy is a supplier of nuclear fuel and services to the American nuclear power industry. It buys raw uranium, enriches it, and sells it as a ready-to-use fuel. It has world-leading expertise in uranium handling and nuclear fuel design.

It is a key American supplier for a strategic industry with a history of financial performance and a very bright future ahead. It is going to be a key player in the development of the next generation of nuclear power plants.

To summarise, Centrus:

- Is the only company that has a Nuclear Regulatory Commission licence for HALEU production

- Has a favourable cost position, with a long-term order book of ~$1 billion through the end of the decade

- Has world-class and proprietary technical, engineering and manufacturing capabilities

- Is an integrated domestic HALEU fuel supplier for national security and commercial needs

- Is now the first US-owned and US technology uranium enrichment plant to begin production in 70 years.

Centrus’ business model is relatively simple. It purchases raw, unenriched uranium from a variety of suppliers across the world. It then enriches the uranium to the specific needs of its clients, mostly global power utilities operating nuclear plants.

It is like an oil refiner, sitting between the miners and the end consumer. It has a diverse range of suppliers on a variety of contract terms, and it also purchases in the spot market to diversify its risk. It has $1 billion worth of orders waiting to be delivered and long-term supply agreements through 2030, which help ensure continued strong financial performance (see below).

In terms of its business, it is also quite innovative. It has a 440,000-square-foot, state-of-the-art Technology & Manufacturing Center in Tennessee, where a team of scientists and engineers develop new ideas with the aim of turning them into proven designs, high-quality products and components.

And so, it has managed to position itself as the key future supplier of the HALEU fuel we looked at earlier. For example, Centrus has signed an agreement with Clean Core Thorium Energy to develop next-gen nuclear fuels together, based on Centrus’ advanced HALEU and Clean Core’s thorium pellets which it calls ANEEL (Advanced Nuclear Energy for Enriched Life).

The new HALEU-Thorium ANEEL combined fuel will be suitable for the existing pressurised water reactors (PHWRs) used in Canada, and the new PHWRs too. Crucially, it will be able to reduce the amount of waste produced in such reactors by 80% – and it will also minimise waste management costs and safety concerns.

There are 48 such reactors worldwide, of which 19 are in Canada, offering Centrus an untapped market to move into. Clean Core plans to test and certify its ANEEL fuel at the Idaho National Laboratory in 2023 and expects to commercialise the fuel by late 2024.

Centrus has also signed a memorandum of understanding (MoU – which is non-binding) with Oklo to cooperate in the deployment of a HALEU production facility. Together, the two companies are aiming to commercialise advanced fission and the HALEU supply needed to fuel them.

As their announcement outlined:

The parties intend to enter into one or more definitive agreements relating to the following collaborative activities addressed in the MOU:

- Oklo would purchase HALEU from the production facility Centrus is planning to build in Piketon, Ohio, the only such facility licensed by the U.S. Nuclear Regulatory Commission to produce HALEU.

- Centrus would purchase electricity from the Aurora powerhouses that Oklo is planning to build in Piketon. These two power plants are designed to power thousands of homes and businesses in addition to the HALEU production facility; similarly, the HALEU production plant is designed to be scaled up to support hundreds of reactors.

- Centrus would manufacture components for Oklo’s Aurora powerhouse at Centrus’ advanced manufacturing facility in Oak Ridge, Tennessee, as well as manufacturing capacity at the American Centrifuge Plant in Piketon, Ohio, where HALEU production will take place.

- Centrus and Oklo would work together to establish and license the capabilities necessary to deconvert HALEU from uranium hexafluoride to uranium metal and fabricate fuel assemblies for Oklo’s Aurora powerhouses.

Centrus, meanwhile, has constructed the country’s first NRC-licensed HALEU production facility in Ohio, which began producing HALEU in October 2023. The company even recently rang the closing bell at NYSE on 5 March this year to commemorate this historic milestone.

Its HALEU will be a key fuel for many of the next-generation nuclear power plants. Its partnerships with Oklo and Clean Core give the firm clear commercial opportunities. Besides the nuclear power industry, Centrus’ other main customer is the American military.

Crucially, Centrus has designed, manufactured and successfully operated the world’s most advanced gas centrifuge (the machine for enriching uranium into useful fuel). It’s called the American Centrifuge, which has undergone rigorous testing by the US Department of Energy (DoE) and is available for national security deployment.

And for numerous reasons, only American companies are permitted to supply the critical fuels required for national security. Centrus is therefore a key partner of the US government.

In its own words, “Restoring America’s capability to enrich uranium with domestic technology is critical to meeting long-term national security requirements, such as supplying fuel for the U.S. Navy.”

Furthermore Centrus made the first delivery of HALEU to the DoE in November 2023, completing the first phase of its contract with the agency.

Phase two requires a full year of production at a rate of 900kg per year. It’s doing this at the American Centrifuge.

In 2015, the DoE described Centrus’ AC100 centrifuge design as the “most advanced” and “lowest risk” option to meet US national security requirements. The American Centrifuge was originally developed by the DoE in the 1980s and significantly upgraded by Centrus over a 15-year period.

These are the most advanced centrifuges in the world. Centrus spent the time since improving efficiency, reducing costs, and enhancing its reliability, thus advancing US expertise in centrifuge design and operation.

Its work is supported by the DoE’s Oak Ridge National Laboratory so that it can ultimately be deployed to support US national security requirements. So, on the military front, as well as commercially, Centrus is in a very strong position.

The company is also strengthening its balance sheet after generating strong profits, bringing liabilities down and growing assets.

Its 2023 annual report (published in February this year and the latest financials of note) shows:

- Revenues from the LEU segment of $269 million

- Revenues from services of $51.2 million

- Gross profit of $112 million

- Net profit of $84.4 million.

Considering the company’s market cap of just $657 million that means the company is trading at what we consider to be a low 7.7-times earnings. For a point of comparison, the nuclear fuel and uranium giant Cameco trades at an earnings multiple of 81-times earnings.

They are slightly different companies of course, but with no other listed HALEU producers that have a DoE licence to produce HALEU, we think the company’s long-term value is grossly underestimated.

Adding to our mix of nuclear plays is important. Now we have exposure through every major step of the process, from mining uranium to the enrichment of the fuel to the potential of small modular reactor technology.

Adding Centrus to complete that pathway is crucial and we believe a huge long-term opportunity for investment.

Buying instructions

Centrus Energy (NYSE American: LEU) is a supplier of nuclear fuel and related engineering services to the nuclear energy industry.

It currently trades on the NYSE American market with a market cap of $657 million and a stock price currently around $40.40.

Volume is a healthy 189,000 per day on average, so it should be relatively easy to get in and out of this stock as needed.

Action to take: buy Centrus Energy (NYSE American: LEU). Buy up to $44. Set a stop loss for downside protection at $21.

Source: Koyfin

Big breakthroughs

James:

Back in August last year we wrote about the potential of space-based solar power, a futuristic-sounding concept that has recently started to receive serious attention.

Certainly, the advent of a burgeoning private space sector and significant reductions in the cost per kilogram of space travel, alongside other recent technological developments, means that some extremely cautious optimism about space-based solar power is now justified, we concluded.

After all, space-based solar power is – or would be – the highest-intensity solar power you can get, available 24/7 and it can be sent anywhere on Earth.

Of course, the ability to collect solar energy 24/7, regardless of weather conditions or geographic location, certainly sets space-based solar power apart from its terrestrial counterpart.

The specific technology we wrote about involves using satellites to harvest solar energy in orbit that is then converted into high frequency radio waves beamed back to a receiver on Earth.

But this is not the only method on the table to harness this limitless clean energy source from space here on Earth.

Last month, a startup from California called Reflect Orbital announced it is now ready to put gigantic mirrors in space to reflect sunshine at ground-based solar farms at night, in turn maximising solar farms’ energy production.

In essence, Reflect Orbital is looking to develop a constellation of satellites to sell sunlight to thousands of solar farms after dark.

Unlike proposals to build solar power stations in space and transmit energy down to Earth, all the generation under Reflect Orbital’s plans would happen down here.

“We think sunlight is the new oil, and space is ready to support energy infrastructure,” explained Reflect Orbital CEO Ben Nowack on X, previously known as Twitter.

“By precisely reflecting sunlight that is endlessly available in space to specific targets on the ground, we can create a world where sunlight powers solar farms for longer than just daytime, and in doing this, commoditise sunlight,” added Nowack.

Nowack, a former SpaceX employee, believes a constellation of simple reflector satellites in low Earth orbit (LEO) can boost solar farms at night – a challenge that requires rockets and getting a lot of affordable mirror areas into space.

The first part of the puzzle was to build and test a prototype.

On 31 August 2023, Reflect Orbital completed its real-life experimentation with a hot-air balloon equipped with a large mirror.

By pointing the mirror toward a mobile solar farm, the company was able to generate 60, 120 and then 140 watts by reflecting the early morning sun rays from the sky down to Earth.

The company is now designing its first satellite.

Certainly, there’s no doubt that the possibility of simple orbital mirror constellations that reflect extra sunlight onto existing solar farms, increasing output in non-peak times, is intriguing.

Although the engineering of steerable ultralight mirrors is challenging, it might not be as inherently expensive as you might think, especially as launch costs continue their downward trend.

Howewer, beyond that, the economics are likely certainly questionable, especially in comparison to alternative land-based technologies.

A recent academic study on “orbiting solar reflectors” suggests the approach is unlikely to be able to make solar 24/7 or even double the output of existing farms.

Instead, it may provide a circa 20-minute boost of output during mornings or evenings. What’s more, the illumination, after diffusing in atmosphere, will not be much brighter than an overcast day.

Although this could lead to perhaps a 10% increase in capacity factor, during admittedly valuable morning and evening periods, it’s hard to see this being cheaper than simply boosting a solar farm’s output using batteries, the cost of which is getting cheaper by the day.

Certainly, if you gave us the choice between simply installing a battery that can produce 100% of a solar farm’s rated power for a couple hours every morning or evening or, alternatively…

… launching a load of reflectors to space in a complex array of satellites that then beam sunlight to ground-based panels in order to boost output to, say, 20% of rated capacity for 20 mins each morning and evening…

… then I think we can work out the direction of travel for any industry involving orbiting solar reflectors.

And it’s not, it’s safe to assume, to the stars and back.

Buy List update

Ashtead Technology Holdings PLC (AIM: AT)

Subsea equipment rental company Ashtead Technology Holdings, recommended at 374p in July last year, fell to 687p on 17 April but was last seen at 758p at the time of writing, around 3% up on the month and 103% up in the model portfolio.

Ashtead has a history supplying subsea services to the oil and gas sector but has diversified into the fast-growing offshore wind market, specialising in renting out equipment crucial for the operations of installations throughout their lifecycle.

The company’s technology offerings include surveying equipment, sensors, and robotics essential for installation, operation, maintenance and decommissioning of assets.

Last year saw Ashtead’s revenues grow 51% to £110.5 million, up from £73.1 million in 2022.

Ashtead’s acquisitions of WeSubsea and Hiretech in late 2022 and ACE Winches in November 2023, contributed 17% of company revenues, according to annual results released on 16 April.

The company also saw strong organic growth in its 2023 results, accounting for 35% of its revenue growth.

Ashtead seems intent to continue its M&A strategy that has seen it complete eight transactions since 2017.

The company is certainly on an ambitious growth journey and making ongoing investments in its subsea equipment rental fleet that has in excess of 23,000 assets.

The stock remains a HOLD while it trades above 395p.

European Metals Holdings (AIM: EMH)

At the time of writing, European Metals Holdings is trading around £18.80 after surging by nearly 45% over the last month, though the stock is still 43% down in the model portfolio.

European Metals part owns the Cinovec lithium asset in the Czech Republic, one of very few advanced-stage, large-scale lithium projects in the European Union with a mineral resource of nearly 7.4 million tonnes of contained lithium carbonate equivalent.

The project is being developed by Geomet, a joint venture between EMH and Czech-state-owned CEZ.

On 11 April, the company said lithium hydroxide monohydrate had been successfully produced in a test during the recent larger-scale Cinovec pilot programme, a significant milestone.

The AIM-traded firm said the achievement underscored the viability of the lithium chemical plant (LCP) process flowsheet for the industrial-scale production of either lithium carbonate or lithium hydroxide.

It said the pilot programme yielded crucial results, demonstrating that crude lithium carbonate could be converted into clean battery-grade lithium hydroxide monohydrate at laboratory scale.

The positions the company closer to realising the full-scale industrial production of lithium chemicals.

“We are extremely pleased with the results from the lithium hydroxide test program,” said Keith Coughlan, EMH’s executive chairman.

“The lithium hydroxide produced was of the highest grade possible and exceptionally clean. This, when combined with the ability to produce either battery-grade lithium carbonate or hydroxide, enables a wider range of off-takers for the Cinovec product.”

In other mews, EMH also announced it has delayed the publication of a definitive feasibility study (DFS) for the Cinovec project, although the company noted that the ongoing additional work held promise for significant project enhancements.

Originally slated for release in the first quarter, the DFS delivery has been postponed owing to continued engineering work and social and environmental engagement efforts that have unearthed potential improvements to the lithium processing component of the study.

European Metals said it would make an announcement before the end of April, detailing some of the significant issues.

European Metals also stressed the extension of the study period would not impact the overall project timeline.

The stock remains a BUY below its 45p buy limit.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF has fallen by 5% over the month to trade last at around £6.07 at the time of writing, putting it around 32% below our £8.96 entry price.

LITG has significant positions across different parts of the lithium supply chain, including in lithium heavyweights such as Albemarle, Tesla and Mineral Resources. This helps cushion it against lithium price volatility. For example, if prices fall, that’s a negative for producers but a positive for companies that buy lithium to make value-added products.

The ETF invests in the full lithium cycle, from mining and refining the metal, through to battery production. It seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Global Lithium Index.

By owning mining, refinery and battery production companies in the fund, Global X has its fingers in multiple parts of the lithium industry.

Although the lithium market has generally been depressed over the last few months, it should certainly benefit from heavy demand for lithium. After all, without lithium, we can’t build EVs or have the green future that countries are demanding.

Certainly, the supply glut in the market looks like it is now set to dissipate. UBS and Goldman Sachs both recently revised their 2024 supply estimates, signalling a reduction in oversupply, while, Morgan Stanley warned of the growing risk of lower inventories in China.

With the market showing signs of re-balancing, we can expect lithium prices to stabilise in the near future.

LITG remains a BUY.

Central Asia Metals (AIM: CAML)

Central Asia Metals (AIM: CAML), a mining company with operations in Kazakhstan and North Macedonia, has risen 9% over the last month to 202p at the time of writing, still leaving it 27% underwater in the model portfolio.

The group’s principal business activities are the production of copper at its Kounrad operations in Kazakhstan and the production of lead, zinc, and silver at its Sasa operations in North Macedonia.

The stock continues to rise in line with strong copper prices, which have risen to nearly $10,000 a metric tonne, a level that is expected to be sustained by the appearance of shortages over the coming months.

Copper prices on the London Metal Exchange (LME) are now around $9,644 a tonne.

The rally was triggered by news that major copper smelters in China have pledged to curb output in response to a tightening copper ore market.

For its part, Central Asia Metals updated the market on operations in its first quarter during the month.

The AIM-traded firm said that, at the Kounrad plant, copper production reached 3,120 tonnes, while at the Sasa mine, zinc in concentrate production amounted to 4,741 tonnes, with lead in concentrate production totalling 6,529 tonnes.

Looking to the full 2024 year, Central Asia Metals projected copper production between 13,000 to 14,000 tonnes.

Additionally, it said it expected zinc in concentrate production to range from 19,000 to 21,000 tonnes, and lead in concentrate production to be between 27,000 and 29,000 tonnes.

CAML remains a BUY under 310p.

Foresight Sustainable Forestry Company (LON: FSF)

Foresight Sustainable Forestry Company, which invests in UK forestry and afforestation assets, has risen 4% over the last month to around 67.32p at the time of writing, putting it around 38% down in the portfolio.

With a decline in land values continuing to impact the investment company and with the firm still not reporting any significant news this year, the firm remains a HOLD in the model portfolio.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation, the world’s largest gold miner, is trading around $37.71, up 11% on the month. The stock is now 42% below our $65.39 entry point.

Newmont has started to trade in line with rising prices of gold, which remains among the best investments of 2024. Gold prices now sit almost 4% below their all-time high of over $2,400 achieved earlier this month, but they remain up about 14% this year, far outperforming the S&P 500’s 5% return.

Amid optimism for NEM’s next earnings report in late April that should continue to support the stock, Newmont remains a BUY under $100.

DS Smith (LON: SMDS)

Recycled-content paperboard and packaging producer DS Smith has risen by 0.4% to 352.40p at the time of writing, putting it 11% up in our model portfolio.

Earlier this month, DS Smith announced that it had been acquired by US-based International Paper, one of the largest paper and pulp companies in the world, in a deal worth £5.8 billion.

International Paper moved in late March to gatecrash a £5.14 billion all-share deal put forward by its British rival Mondi.

The companies have recommended the deal to both sets of shareholders, arguing that they will bring together complementary businesses with “industry-leading positions in two of the most attractive geographies of Europe and North America”.

Under the terms of the takeover, DS Smith investors will receive 0.1285 International Paper shares for each DS Smith share. This values each DS Smith share at 415p based on the closing International Paper share price of $40.85 on 25 March, the last day before the announcement of a possible offer.

Upon completion of the combination, DS Smith shareholders would own about 33.7% and International Paper shareholders would own the rest of the combined company.

International Paper said it would seek a secondary listing on the London stock market.

UK firm Mondi last month reached an agreement in principle to buy DS Smith in an all-stock deal of £5.14 billion, with the purchase price representing a 33% premium at that time and DS Smith shareholders getting control of 46% of the enlarged group.

But International Paper late last month offered a higher counter-bid as it sought to expand its European presence at a time of consolidation in the sector.

The takeover still needs approval of both sets of shareholders. The deal is expected to close in the fourth quarter of this year.

The stock remains a BUY.

Kraneshares MSCI China Clean Technology Index UCITS ETF (LON: KGRN)

Kraneshares MSCI China Clean Technology Index UCITS ETF, recommended at $24.83 on 12 October, the day it listed on the London Stock Exchange, was last seen at $19.67, putting it 21% down in the model portfolio. It has fallen by around 3% on the month.

KGRN, which tracks the MSCI China IMI Environment 10/40 Index, is the only UK-listed ETF to specifically tap into China’s cleantech industries.

I’m certainly happy to continue to have exposure to some of China’s world-leading manufacturers of clean-energy technology, from solar panels and wind turbines to electric vehicles, in our portfolio.

China’s government has a grand plan to achieve energy independence and is spending big to make it happen. Goldman Sachs estimates that China will funnel over $7 trillion into energy transformation through 2040.

The ETF is a BUY below $26.83.

NET Power (NYSE: NPWR)

We recommended carbon capture company NET Power at $9.49 in our November 2023 issue. At the time of writing, it is fetching $11.01, putting it 16% up in the model portfolio, with the stock rising 1% over the last month.

As you’ll recall, NET Power has developed a natural-gas power plant that makes it easy to capture carbon dioxide released by the burning of natural gas.

Net Power’s technology produces electricity by combusting natural gas with pure oxygen, creating water and carbon dioxide — most of which is recirculated back into its power generation system.

Excess high-purity CO2 can then be sold to industry or sequestered underground. The company plans to use Occidental Petroleum’s existing infrastructure near Odessa, Texas, to move trapped CO2 to a permanent storage location.

The company plans to build its first natural gas plant in Texas’ Ector County by the first half of 2028.

The stock remains a BUY up to $11.

Stellantis NV (NYSE: STLA)

We recommended multi-car brand giant Stellantis at $22.84 in the January issue. At the time of writing, its shares are trading at $24.96, putting it 9% up in the model portfolio, after falling 15% over the last month.

The stock reached an all-time high at nearly $30 on 25 March but has since fallen back, in part due to an industry sell-off sparked by concerns over EV demand.

However, the Chrysler-parent company is moving ahead with its EV plans, even as competitors scale back and sales growth slows.

Stellantis CEO Carlos Tavares has been relying on cost cuts to make Stellantis leaner and bolster profit, citing pressures from the EV shift as reason to thin its workforce in countries including France and the US.

The stock remains a HOLD while it trades above its buy limit of $23.50.

Prysmian Group (IL: 0NUX)

Prysmian Group, which entered the model portfolio at €48.13 in the March issue, now trades at €49.74, putting it 3% up.

Since the recommendation, the Italian cabling giant has confirmed its new CEO and General Manager to be Massimo Battaini and entered into long-term supply contract for copper wire rod with Aurubis.

The stock remains a buy up to €60.

Cyngn (NASDAQ: CYN)

Earlier this week Cyngn’s stock price exploded higher up over 100% in intraday trading on Tuesday. Then it closed around 10% lower. So, what the hell is going on?

Well Cyngn announced on Tuesday that the company had been chosen to supply its DriveMod Tuggers to John Deere’s operation in Dubuque, Iowa.

Cyngn didn’t say categorically that Deere was the “Fortune 100 company” it often refers to in its press releases, but c’mon, it’s got to be, right?

When we first recommended the stock we said:

Cyngn announced in July [2023] that it had signed a new customer, a “Fortune 100 Heavy Equipment Manufacturer.” This was followed up in September with, “Paid Deployment with Fortune 100 Heavy Equipment Manufacturer in North American Facility.”

Now it doesn’t take too much to have a guess at what company it’s talking about here.

The Fortune 100 only has two heavy equipment manufacturers in it.

Those are the $110 billion and $132 billion heavy machinery giants, Deere & Company and Caterpillar Inc.

While Cyngn hasn’t named the “Fortune 100” company, we can’t see how it can be anything else than one of those two.

Maybe we were right all along. Either way, it doesn’t matter. The point is a company like Deere says this is the kind of tech it wants to use in its operations. That is vindication that Cyngn is on the right track.

Now, that’s why it shot higher. So why did it claw back all that performance and close lower in just one trading session?

Well management then released another announcement about a capital raise of $5 million at a stock price of 10 cents. So, as you’d expect, the price headed down to the raise level.

Honestly, for all the potential of this stock, the management seem to be quite useless at how they communicate to the market. Even the simple strategy of announcing the capital raise before the Deere news would have made perfect sense to a rational human being.

The dilemma here is that as we maintain this position, we are still excited about the tech and potential of that tech in the company. But increasingly we are bemused by how management operates and the timing of its capital raises almost immediately after a really strong announcement.

It does seem right. That said, we think the tech overrides its other follies. We stick with the stock and strongly expect that deals like the one with Deere do propel the company back to a stock price where we can look to extract a profit from the position.

CleanSpark (NASDAQ: CLSK), Hut8 (NASDAQ: HUT) and Argo Blockchain (LON: ARB)

With these three companies, it’s important that you read this month’s Crypto Corner section.

In short, it looks at the impact the bitcoin halving has taken on the miners. This includes examining why the market thoroughly oversold these companies leading into the halving and why they still all have long-term potential into a new bitcoin bull market.

In short, they remain able to generate significant volumes of bitcoin in their operations. The incoming quarterly reporting should give us some clearer indications as to just how that might look for Q2 and Q3 this year.

Expect them to remain volatile. If the price of bitcoin does head higher along with their reporting of strong mining volumes, then these miners could all be primed to pop higher.

Surface Transforms (LON: SCE)

The case of Surface Transforms is one in which again there’s a definitive market for its cutting-edge technology, but problems in production, capital and cash flow have all worked against the company.

This is an example of a company that is perhaps too niche. Even though there are clear benefits from carbon ceramic brake technology, the company is repeatedly unable to capitalise on this market opportunity.

Surface Transforms still expects to be able to deliver profitability in 2024 however and still claims to have long multi-million-pound pipelines with OEM customers. Yet the stock has been crushed and it is trading at a fraction of our entry.

It seems the market is now pricing in the company struggling to exist longer term as a going concern. Which means do we stick with it and take management’s view that they can right the ship? Or is it that when the company’s next update hits it says it’s going to bring in the administrators?

At this point, we stay with the stock. If Surface Transforms can make this thing profitable and it has indeed truly appeased the OEMs, then a return higher is a real possibility. But we expect May’s financials and the next few operational updates will be critical. Not knowing exactly where it ends up, the stock is a HOLD until further notice. This is considering the risk from here that the company could wind up operations if it can’t deliver on recent promises. But we believe the company can rectify the situation and there is a strong market for its products.

Inside the lives of James and Sam

Sam:

April there’s really only one thing happening outside of work and family…

It’s MASTERS MONTH.

Would this be the year of Rory McIlroy finally getting his hands on a green jacket? Or would the seemingly impossible-to-defeat Scottie Scheffler snatch another one?

Or… maybe, just maybe… Tiger would rise from the depths of near disability to get just one more under his belt.

Even my wife knows that it’s Masters week when the golf is on this time of the year. And thankfully a few of the dads at my son’s school were keen on hitting the local marina to have a few “daddy drinks” as my son puts it, and see just who would reign supreme.

This was the one and only photo from that night. I used it to remind my brother that he should have been on a plane to spend some time with his nephews (but really to hang out play golf and watch it with me that week).

Can’t get too much a better spot for a spot of Masters coverage than here. Albeit the best location to watch would be at Augusta.

Which is exactly what I plan to try and do next year. I’ve registered myself on the Masters website and will be applying for tickets. And if I can’t get any, I’ll keep trying every year until I get them… or die.

It’s bucket list stuff but is also a clear reminder that golf is big business. Even where I’m located down in the Algarve, one of the main reasons people come down here is for golf. And with a lot of the courses here charging in excess of €120 per round, you can see why.

Clubs, bags, apparel, travel, beers at the pub… golf is mega business. And then you see that in 2024 alone, Scottie Scheffler has made around $16 million in prize money and you wonder why aren’t I a golf prodigy?

There are some big companies involved in it too from Topgolf Callaway Brands ($3 billion market cap), Acushnet Holdings ($4 billion), Mizuno Corp ($1.2 billion) and of course the Saudi Public Investment Fund ($unlimited capital)…

Fair to say that if you can get a chunk of the golf pie in your investments, that also might not be a bad approach to take for a robust overall portfolio. And like my grandfather used to explain to me, own the companies who make the things you buy.

James:

Long-term readers will know that, together with my partner, twin brother and his wife, I own a two-bed apartment in the French ski resort of Avoriaz, nestled in the Alps in the commune of Morzine.

We bought the property with two purposes in mind, the main one being for our respective families to enjoy it for ourselves for a few weeks a year. However, we also hoped we’d be able to make a little money via letting it out the rest of the time.

On the first count, the purchase is proving an undoubted success.

We’ve now had several holidays with family and friends at the apartment. We keep our ski equipment and clothing in a designated locker in the building, which has removed a lot of the hassle out of any ski holiday. The apartment now feels very much like a home away from home, and we’ve started to make some friends in the resort.

It’s also been fantastic to see the kids improve their abilities on the slopes at rates that no adult can remotely match.

But on the second count, it’s fair to say the jury is still out.

Prior to the purchase we ran the numbers and thought it would be possible to generate a yield of around 5-6% via letting it out, though, in truth, we would all have been content if the property was at least able to wash its own face, thereby providing us with some “free” holidays.

It hasn’t worked out that way, though there are some obvious reasons for this, not least the fact that the purchase finally completed in February 2020, just one month before Avoriaz, like the rest of the French Alps, closed for nigh on two years amid sweeping Covid-19 lockdown measures.

Those two years of paying the mortgage with no rental income coming in meant that we ran the property at a loss.

What’s more, since the resort reopened, we’ve used the apartment ourselves frequently, including in some of the peak weeks of winter when short-term rental rates are at their maximum. We’ve been eager to make up for lost time and very much accepted that this would impact on the apartment’s top line.

As I said, the main reason for the purchase was to enjoy it for ourselves – which is something we couldn’t do during Covid and a wrong we’ve been determined to put right subsequently.

One factor that we’ve been unable to control is the weather. Over the last two winters, the snow has been a little patchy, which has reduced demand in the winter over some key weeks, pulling down rental rates with it.

Generally, however, the apartment has been pretty much fully booked over the winter when it’s been available to rent, while summer bookings have been more or less in line with expectations laid out in the estate agent’s brochures (at around 50% occupancy).

But with all this mind, we’ve decided to make some changes.

Now that we’ve all had plenty of trips to the apartment in the post-Covid years, we’ve decided that we will collectively reduce the amount of time we spend there during the winter.

We will now also bookend any ski trips we make to either right at the beginning of the season in December and/or right at the end in April, keeping the peak weeks only for rentals. This had been the original plan before Covid changed our motivations.

Finally, we’ve also decided we will now market the property ourselves and no longer use the services of a local rental agency that creams off 25% of our booking revenue.

It was vital to use such an agency while we were still finding our feet with the apartment and resort, but we now think we’re in a position where we can do a lot of the donkey work ourselves, especially as there are four of us to divvy up the tasks.

We’ve already contracted a local concierge service on the ground to help with the linen and laundry, as well as handling the keys and other emergency functions that come with running a short-term rental property. But we’ll do all the marketing of the property ourselves.

We’re now deciding whether we need to use a property management system such as Guesty or Hospitable that both automates and centralises some of the marketing functions for a small fee. These services also us to build our own website to drive direct bookings. (If any of you have any experience with these systems then please do drop me a line and let me know if one is better than the other!)

Either way, the property will be going live on Airbnb and perhaps one or two other portals in the next week or two.

In short, as a seasoned investor, I’ve been happy to accept some of the challenges involved with running a vacation property. Things haven’t’ always been plain sailing but the apartment is now successfully serving its main original purpose and now, with the tweaks we’ve made, it’ll soon start to pay its own way too.

Crypto Corner

Sam:

The hardest thing during a crypto cycle is to do nothing.

And sometimes, you should be doing nothing.

Well, slight caveat to that. My view is that you should, where you can be, “stacking sats”. That means adding to your bitcoin pile.

That is a long-term hard and fast view that for the last 14 years has been 100% the right thing to do.

But outside of bitcoin, the wider market, there are times when nothing is the best thing.

It can be easy to get tempted into just doing something, but often you’re better off deleting the CoinGecko app from your phone and just leaving it all alone for a while.

That’s because you want to have already deployed your capital into crypto that you’ve got conviction will do well in another bull market cycle.

If you’ve not taken your stake and built your crypto portfolio by now… it’s not too late, but it’s not far away from being too late.

Most people will buy up various crypto into a rising market. But you’re simply lowering your chances of mega success by waiting too long.

The other thing that’s tempting is to get involved into things you don’t know much about because you anecdotally see and hear of people making money hand over fist in the market on the most stupid of things.

I’m all for owning some memecoins, and over the years I’ve done quite nicely from memecoins. I do think if you really want to commit to crypto investing, playing about with a tiny bit of risk capital and memecoins is actually a bit of fun. But here’s the thing: of the huge number of memecoins out there, only a handful will ever make it.

Your chances of hitting the big time, 1000x gains (and more) are so slim that you either a) shouldn’t bother, or b) have the expectation that if you make 1,000% you’ve already shot the lights out more than most will.

Also, the time to buy up memecoins for “max gainz” was this time last year. Now with the market going a bit bonkers for them, I dare say you are too late for mega money in memecoins, but there’s still some profit to be had.

Point being, build a portfolio of the staples of bitcoin and Ethereum, solid layer 1 crypto. That is, crypto that align with thematic areas like decentralised physical infrastructure (DePIN), artificial intelligence (AI), bitcoin layer 2 developments, and a meme coin or two.

Now when it comes to the big guns, as in bitcoin, we should talk about the halving and how that’s impacted not just the market but importantly the miners that secure the market.

How to cut your revenue in half and increase it at the same time

Bitcoin’s halving completed over the weekend. And the block reward was slashed in half, as it is every 210,000 blocks.

This is often a tipping point that leads into another big crypto bull market. And I don’t see this time being any different.

But just like all the other halvings, there’s been a fair share of negativity about this halving, particularly aimed at the bitcoin miners. That’s important to know because the market took the view that a reduction in the block reward means a reduction in miner revenues…

Well yes… and no.

In fact, what we’ve begun to see is miners making more after the halving and it boils down to JPEGs.

This story goes back to 2017 when the idea of non-fungible tokens (NFTs) first became a part of crypto.

These were predominately based on the Ethereum blockchain and became quite the craze. Their launch became so popular that in some cases it completely clogged and slowed down the Ethereum network.

The NFT mania, however, really took hold in 2021’s crypto bull market when millions were being made on the minting and trading of NFTs on all kinds of different networks from Ethereum to Tezos to Solana.

The NFT craze caught mainstream headlines as renowned digital artists were seeing their NFT art selling through legendary auction houses like Sotheby’s and Christie’s all of a sudden.

The most famous and valuable of all was the sale of Beeple’s “Everydays: The First 5000 Days” which sold for $69.3 million in March 2021.

NFT mania has caught its fair share of critics over the years. The 2021 bubble clearly burst not long after. Albeit some popular NFT mints like CryptoPunks and Bored Ape Yacht Club still have “floor prices” upwards of $100,000 and $35,000 respectively.

Historically these NFTs have never been a “thing” on the bitcoin network. Mainly due to the fact that they were technically possible. The programming capability of other networks like Ethereum and Solana made NFT creation and popularity easy.

However, thanks to network upgrades like Taproot in 2021, all of a sudden bitcoin allowed for greater programming capabilities. In 2023 we began to see new developments on bitcoin around NFTs which were called inscriptions. This led to a surge in Ordinals which were NFT inscriptions on the bitcoin network.

This is all important because in 2023 and into 2024 the popularity in Ordinals started to have an impact on the fee generation of bitcoin’s network.

That’s important for miners, because while they get the block reward when they mine a block, they also get the fees generated per block.

So for example, if a miner mined a bitcoin block pre-halving, they were getting 6.25 BTC plus the fees. What you’ll see in the chart below is the average fee per transaction on bitcoin. What this means is that a higher fee means often higher fee rewards per block.

You can see in late 2023 that the average fee per transaction went from around $1.75 in early November to as high as $37 per transaction in mid-December.

That’s due to Ordinals.

So miners, began collecting more and more BTC per block in fees leading into the halving. In some cases the fees were getting close to the block reward.

Yet since the halving took place last week we’ve seen the release of what

are called “runes” on bitcoin’s network. This is the ability to mint fungible

tokens on bitcoin’s network. Fungible tokens are those that can be replicated and are not individually unique like a non-fungible token is.

This has only been possible since the halving and the release of the runes protocol. The stock market didn’t understand this at all but the build-up in excitement for runes has been working its way through crypto circles for months.

And that massive spike in fee per transaction right after the halving is the result of runes.

The day after the halving, with the surge in activity in minting runes on bitcoin, the average fee per transaction rose to over $127. It became so wild that miners were now making more per block in fees than they were getting from the newly slashed block reward of 3.125 BTC.

In fact, the total reward per block was now exceeding the total reward per block before the halving.

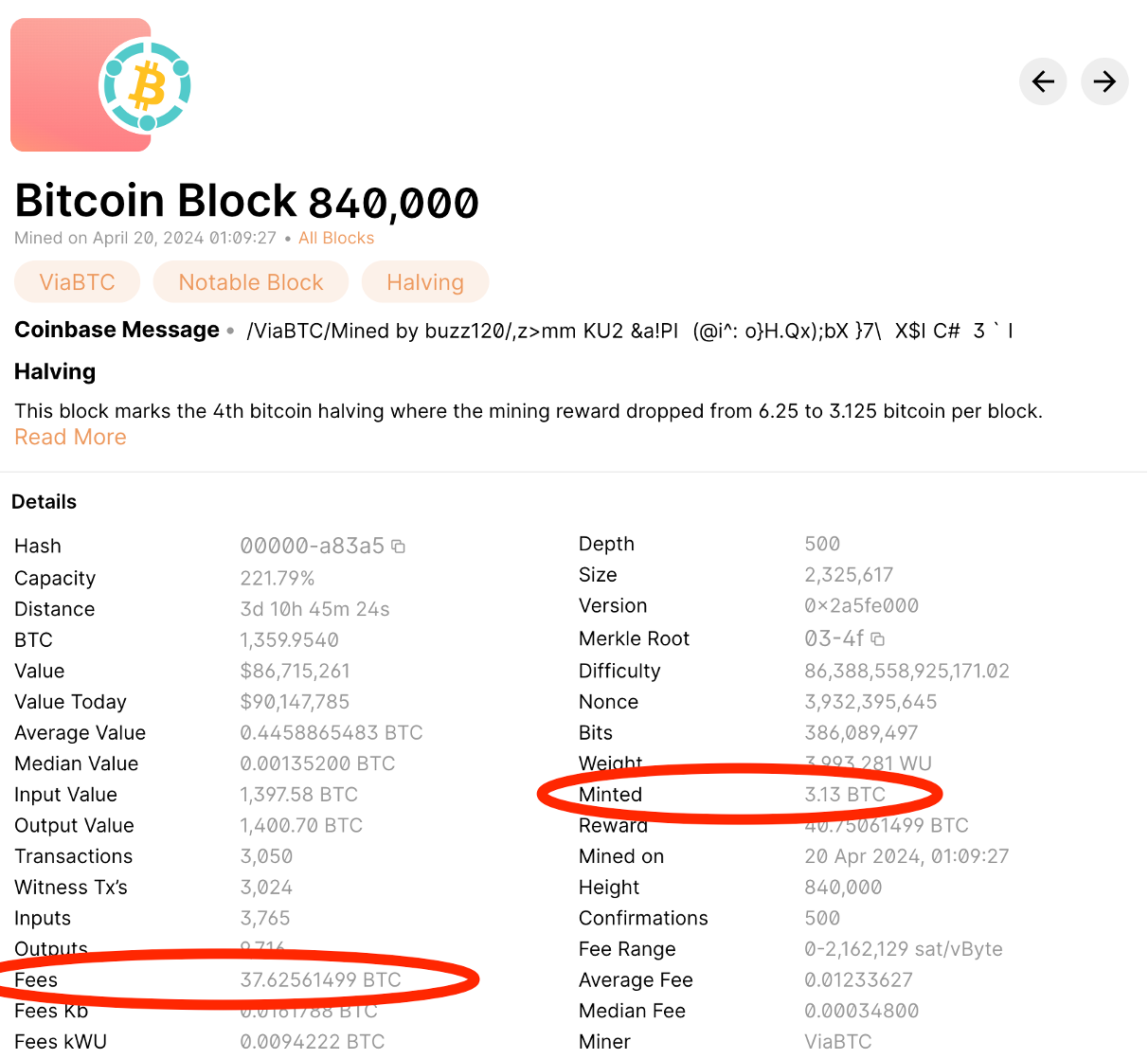

Take a look at block 840,000, the first block of the new halving epoch.

I’ve highlighted here two things. The “minted” section which indicates the new block reward of 3.125 BTC (they round up to 3.13 in the display but it is only 3.125) and also the total fees, which in this case was 37.625.

That means the miner of this block got a total reward of 40.75 BTC.

This has, of course, died down somewhat since. But even now there are regularly blocks where the fee reward is more than the block reward. In many situations miners are currently making more per block than they were pre-halving.

This all happened over the weekend, so the market couldn’t properly react until Monday. And they all shot higher. This is exactly the reaction we were expecting post halving.

The fee generation of miners is often overlooked. While the long-term price factor we still believe offsets any slash in the block reward, you also must factor in the block reward plus the fees.

This is a sign that miners can remain highly profitable with bitcoin mining long term.

It bodes well for the like of CleanSpark (CLSK), Hut8 (HUT) and Argo (ARB) as it shows that the negativity around the halving was overexaggerated. However, bear in mind they continue to trade with great volatility as they will still move off the bitcoin price action, but at least the fears of the halving, for now at least, seem to be past us.

What else we’ve been looking at this month

James:

China is hoarding copper, but why?

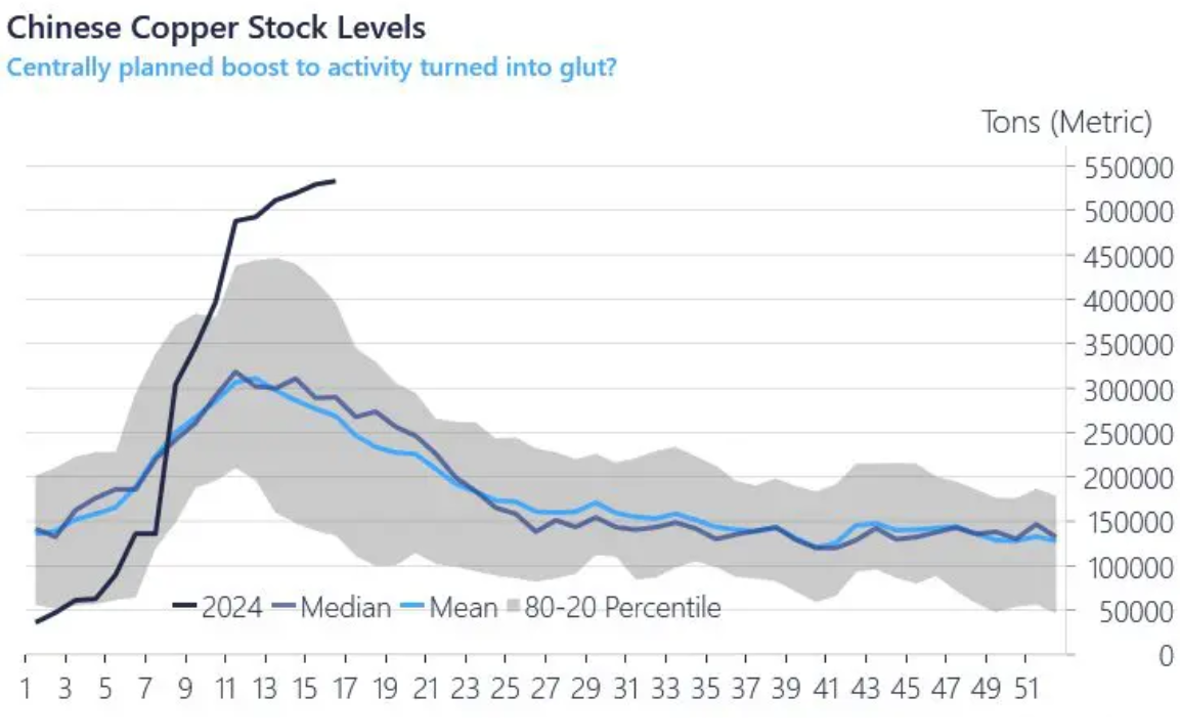

Something strange is going on in the copper market, specifically in China.

Starting mid-February, China started to hoard copper like there’s no tomorrow, as the chart below shows.

It’s hard to say for sure what China is up to.

One argument is that the stock levels are building as a consequence of sluggish demand. Another is that China is potentially looking to take advantage of relatively low copper prices ahead of an upswing in goods production as it builds out massive capacity within green tech – be it in solar panels, EVs or wind turbines. Copper, after all, is the backbone of the green energy transition.

But with similar stockpiling taking place in other commodities such as oil and iron ore, could China also be preparing for a structural devaluation of its currency, stocking up on important commodities in advance? Manufacturing efforts within EVs, solar and batteries would certainly gain momentum from a one-off CNY devaluation, after all.

Of course, Chinese buying of copper and the like could serve to boost select commodity prices, much to the benefit of our holding Central Asia Metals (CAM). We’ll continue to watch this development closely.

Coal about to entirely drop off the UK grid

You don’t hear much about coal-fired power in the UK any more, and with good reason.

Over the last ten years, costly carbon taxes and the emergence of cheap renewable energy sources have pushed coal power to the margins of Britain’s energy landscape. While some facilities, such as Drax in North Yorkshire, have transitioned from coal to biomass, most have had to shut down.

In fact, only one coal-fired power plant now remains – Uniper’s Ratcliffe-on-Soar plant in Nottinghamshire – and that is due to shut in September, calling time on an industry that as recently as the 1980s generated four-fifths of the UK’s power.

You could even say Ratcliffe’s closure will marks the end of the first Industrial Revolution, which was largely built on coal, and in time could symbolise the start of another. Uniper has already set out plans to produce green hydrogen at the site by the turn of the decade.

But until September, the Ratcliffe plant will continue to fire up as a back-up option. For the next few months, and the next few months only, you can see its daily contribution to the UK grid here.

Learning the secret to the strongest force in the universe

In the recent Scientific American article “Physicists Finally Know How the Strong Force Gets Its Strength”, author Clara Moskowitz explains a recent breakthrough in understanding the strong force, one of the four fundamental forces in the universe that holds atomic nuclei together. The strong force operates between the particles known as quarks and gluons that make up protons and neutrons.

In particular, it shows how 99% of the mass in the universe comes from the energy of gluons that glue quarks together inside protons and neutrons.

The breakthrough not only enhances our understanding of the fundamental constituents of matter but also improves our ability to predict nuclear reactions in environments like the early universe and neutron stars.

For someone who didn’t get beyond physics GCSE, I found this superbly crafted article surprisingly easy to follow. It tells us more about how materials behave and, in turn, demystifies the bizarre force that binds atomic nuclei together. Highly recommended.

Sam:

What does NASA learn from an eclipse?

As noted, it’s all been about the moon, the sun and the eclipse in the month of April for me. And while the kids are fascinated by it, so am I.

And I wonder what scientists will have been able to learn from this event about our moon, the sun and space. That’s why I’ve been regularly on NASA’s website this month to see what it learnt from all this.

This rundown after the eclipse was a great read about NASA’s perspective and how it brought together all kinds of testing and analysis of what took place.

How to cool the future

I’ve recently been writing a lot about the AI revolution in our free Substack e-letter, AI Collision, (as you’d expect).

In particular I’ve been looking at all the different parts of the puzzle that go into making AI function as it should. After all, the processors are just one part of a much bigger picture to an AI future.

There was one company in particular that I wrote about just a couple of weeks ago that’s worth checking out here.

Well, that company just released its latest quarterly earnings report. And it was great. So great in fact that the stock jumped from a close of $79 to a high of over $92 the next trading day!

Which meant of course that I’ve had my head buried in its earnings reports and presentations. It’s worth a look to understand that the AI revolution is much, much more than just Nvidia processors and the large language models of “Big Tech”.

Bikes, cars, computers and cash companies

There’s some action afoot in the world of motorsport.

The owner of the Formula 1 Championship, Liberty Media, went and bought the MotoGP championship at the start of the month.

This is interesting for a few reasons. Liberty Media is clearly making bank from Formula 1, seeing a 6% increase year on year from F1 revenues. It’s really turned F1 into a profitable sport. According to McLaren CEO Zak Brown, “We’re now in a position where pre-Liberty, you had teams falling away. Now post-Liberty era there are teams lining up to get into the sport.”

He went on to say that every team is now worth over £1 billion. That’s telling, because clearly Liberty sees an opportunity to do something similar with MotoGP. Is the idea of a double header F1 and MotoGP weekend on the cards?

In the US, I believe so. It’ll most likely happen at the Circuit of the Americas in Austin, Texas, where both championships already race (albeit currently at different times).

What’s also telling is that big-money sponsors are now flooding back to F1. It’s rumoured that a “pack” of teams are trying to get MasterCard on board. Leading the charge is McLaren.

This comes off the back of HP announcing a title partnership with F1 team Ferrari. It’s said the value could account for as much as two-thirds of the team’s budget!

Not like Ferrari (the car company) is struggling either. Its stock is up from around $278 a year ago to trade around $420 now. Success on the racetrack likely only helps with sales, pushing the company further into profit.

So you see, something like Liberty Media buying MotoGP, its existing ownership of F1, the increasing value of the brands and teams in F1, it all connects and fits together. Then it impacts publicly listed companies like Ferrari too and makes us wonder if these are the kinds of stock worth buying…

Maybe, if Ferrari starts winning anytime soon!

James Allen and Sam Volkering

Editors, Small Cap Investigator