Your August issue of Small Cap Investigator

5th September 2023 |

- How to invest in the AI boom by not investing in AI at all

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

How to invest in the AI boom by not investing in AI at all

It’s 2019, November, and the world (for the time being) is as “normal” as you could expect. Little did the bulk of us realise that in just a few months’ time, the most impactful event of the 21st century would create a social and geopolitical upheaval the likes that none of us could possibly imagine.

But that’s still a few months away. The news that’s dominating the headlines of the financial markets right now is all about the “trade war” between the US and China.

Realistically, it’s not the first time these two global superpowers have been in a squabble about trade. The US is the incumbent superpower, both from a military and economic perspective, and China is looking to dethrone the “king”.

Arguably, the trade war that kicked off in 2019 is still in play. In fact, you only need to look at the current headlines getting around the newswires to see it for yourself…

Source: The Telegraph

Source: The Telegraph

There’s no doubt in my mind that these actions are related to the Chinese kerbs on the export of specific metals used and needed for the very chips the US wants to try to restrict heading back to China (I’ll get back to this point shortly).

Something fishy is going on. The US seems scared of China’s growing technology strength – and scared of its very specific capabilities surrounding artificial intelligence (AI).

To understand why that might be, we need to go back to July 2017 – two years before the “trade war” kicked off in earnest.

Specifically, we need to look at a document released by the Chinese State Council, titled “Next Generation Artificial Intelligence Plan”.

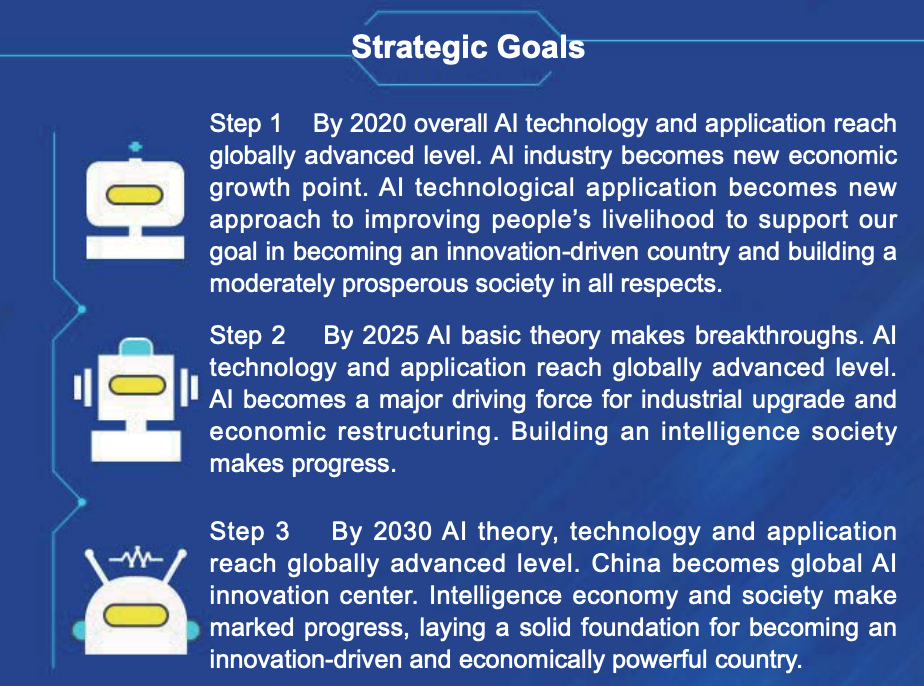

This was an outline from China about how the country planned to achieve dominance in the field of AI. A part of that was a three-step timeline. The third step is of significance, which says:

The third step is to reach the world’s leading level in artificial intelligence theory, technology and application by 2030, becoming the world’s major artificial intelligence innovation center, achieving significant results in smart economy and smart society, and laying an important foundation for becoming a leading innovative country and an economic power.

From a Chinese government-released summation, you can see the full three step plan below.

It’s step three that is most critical here. It expressly states China’s goal to become a global AI innovation centre. In other words, the leading global superpower in AI.

It’s worth taking a look at the entire paper. While it certainly outlines several strategic pathways toward AI dominance, China also knows that there is something critical to all of this coming to realisation…

… metals.

You cannot make the technology needed for an “AI world” without specific, critical metals. That’s part of why China has a stranglehold on the world’s high-tech metals.

Amongst its critical metals chokehold is arguably two of the most important metals needed in a high-tech future. Metals that are often overlooked by the market. Metals that we believe will gather momentum and prominence in the market as the “West” realises that supply security becomes more important to their high-tech future than cost.

Trade war, chip war… cold war

China has been a dominant player in the supply of metals needed for high-technology applications for a long time. Its dominance in the supply (processing) of rare earths is legendary. This is because China has refined and supplied metals to the world at ridiculously low prices, effectively undercutting the world to secure the supply chain (because China could).

For several years now there has been a concerted effort by the West to start to wean off their reliance on China’s supply of rare earths.

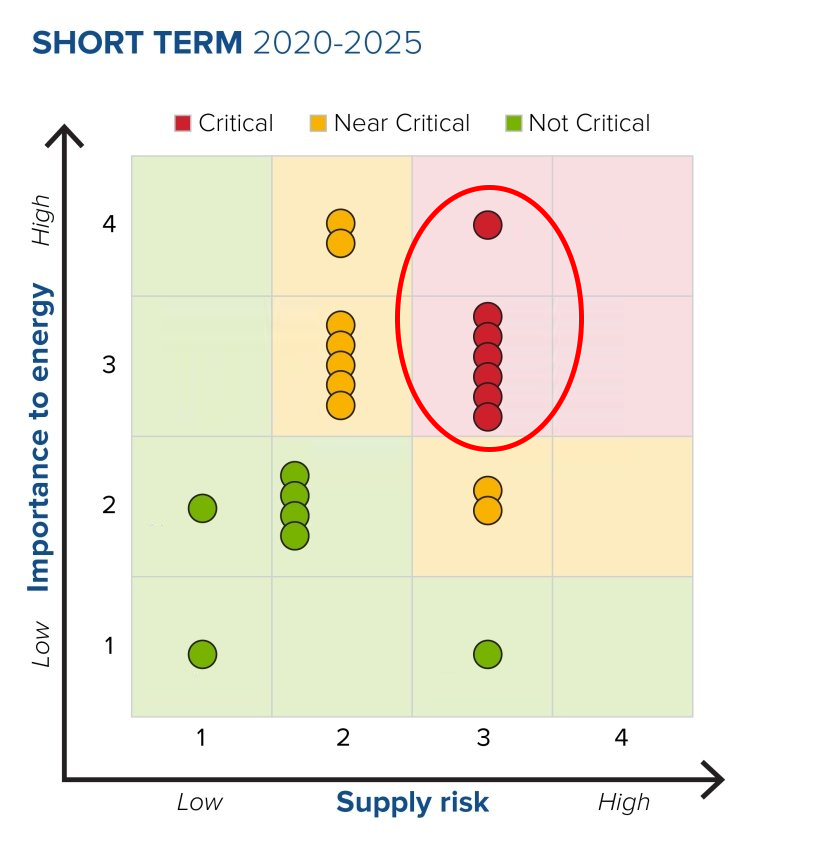

To understand why the West is hell-bent on securing their own supply of critical metals, all you need to do is look at the following chart.

Source: energy.gov

Source: energy.gov

I’ve circled a section in the top right-hand corner. This is because those are some of the most critical metals according to the US government. They are almost all part of the “rare earth elements” family of metals. Rare earth (lanthanide series) metals such as terbium, dysprosium and neodymium are in the mix. But there’s two other rare metals not often recognised by the market for their importance.

Those are gallium and germanium.

Right now, gallium and germanium may be two of the most important metals on Earth. Germanium isn’t highlighted on the chart above, but it is on the lists of critical metals in both the US and Europe. These two go hand in hand.

Gallium and germanium are rare. You don’t just pull them out of the ground like you might with gold, for example. The typical way to get gallium and germanium is through zinc mining.

Like the more known rare earth elements, China has historically dominated the supply and processing of gallium and germanium. In fact, China controls 98% of the world’s supply of gallium and 60% of the world’s supply of germanium.

So, when just a few weeks ago China decided to place export controls on gallium and germanium, this was a clear amplification of the trade wars that have been ongoing since 2019. China’s reasoning was to “safeguard national security and better fulfil the international obligations.”

In other words, China’s decision to restrict gallium and germanium exports is in response to the increasing levels of restrictions from the West for semiconductor or “chip” exports into China. Hence when The Telegraph reported the US was going to block Nvidia chips into the Middle East, which were then believed to be used by China, the tit-for-tat stepped up a level.

Trade wars, chip wars… call it what you will. What we’re seeing in play is a cold war between the US and China – and it all boils down to who’s going to lead (or win) the race in AI dominance.

But why gallium and germanium? What makes them so important in all of this? Why did China use gallium and germanium as its blackmail tool in the latest escalation of these wars? And why does it make a tiny mining company on the London Stock Exchange perfectly placed to profit from these chip wars?

Why is gallium and germanium important?

Gallium is a remarkable element that plays a crucial role in semiconductors. As the world’s insatiable appetite for semiconductors increases, gallium finds itself on the list of critical metals. Both the US and the European Commission have gallium and germanium on their list of critical metals.

One of gallium’s standout features is its low melting point, which is just slightly above room temperature at around 29 degrees Celsius. This characteristic makes it ideal for applications in microelectronics and semiconductors. When combined with other elements, such as arsenic or phosphorus, it forms gallium arsenide (GaAs) and gallium phosphide (GaP). These are essential compounds in the production of high-performance semiconductors.

Furthermore, gallium-based semiconductors have found their niche in specialised applications like optoelectronics and high-frequency amplifiers. Gallium nitride (GaN) is another compound that has gained prominence in recent years. This is due to its wide bandgap and exceptional performance in power electronics, LED lighting and even in the emerging field of 5G technology.

It’s expected that the use of GaN semiconductors will escalate as the world adopts more electric vehicles, uses more advanced and power-hungry semiconductors which are needed to operate at increasingly higher performance levels and as military technology continues to advance and improve.

Gallium’s importance in semiconductors is undeniable, given its unique properties that enable the creation of high-performance electronic devices. Its role in the electronics industry and its status as a critical metal underscore the need for sustainable sourcing and recycling efforts. This is to ensure a stable supply of this essential element for future technological advancements.

Likewise, it wasn’t just gallium that China put export controls on. The country also did the same with germanium. This too is a metal that is used in everything from high-performance chips to advanced driver assistance systems (ADAS) through to military uses such as GPS and night-vision systems.

The Chinese controls on germanium aren’t as dominating as gallium, but both are needed to supply our high-tech, energy-efficient future. Plus, they are exactly what a London Stock Exchange-listed miner has recently discovered at one of the leading mining prospects in Greece.

Can this tiny miner profit from China’s export controls?

Rockfire Resources (LSE:ROCK) is a tiny mining company listed on the London Stock Exchange. The company has several exploration projects on the go. The most relevant and potentially profitable of these is the Molaoi project. This is a zinc, lead and silver mine about a three and half-hour drive southwest from Athens.

On the face of it, a zinc, lead and silver mine isn’t all that exciting… until you recall something I mentioned earlier.

The way to mine gallium and germanium is typically through zinc mining.

In an announcement on 23 August, Rockfire confirmed both gallium and germanium at its Molaoi project.

It should be said that the company is predominately a gold, copper and zinc miner. Its 2022 annual report highlights JORC resources (JORC meaning the mining industry’s official code for reporting exploration results) across its projects of:

- 130,000 ounces of gold and 800,000 ounces of silver at Plateau;

- 120,000 tonnes of copper equivalent at Copperhead (comprising 80,000 tonnes of copper, 9,000 tonnes of molybdenum and 1.1 million ounces of silver); and

- 250,000 tonnes of zinc equivalent at Molaoi in Greece (comprising 210,000 tonnes of zinc, 39,000 tonnes of lead, and 3.5 million ounces of silver).

Its decision to focus resources towards Molaoi is significant. This is due to the increase in value of the project thanks to the find of both germanium and gallium at the exploration site.

Of further importance here is that Rockfire owns 100% of the site with a 30-year exploration licence, which was only granted in March 2022. Being in Greece, there’s also an element of geopolitical risk that’s mitigated thanks to it being a low-risk jurisdiction.

In terms of potential value of this discovery, Rockfire highlights that a tonne of germanium is currently worth around US$2.75 million per tonne.

Exactly how much germanium and gallium are at Molaoi is hard to say. Right now the mine is in its exploration phase. These are test holes that prove there is both gallium and germanium at the site.

It’s expected the next steps, and further catalysts for the company, will come via feasibility studies. These will assess the commercial viability and potential success of the site. The expectation is that these will commence before the end of this year. Furthermore, the company is expecting to commence underground production within the next three years.

We believe that having both germanium and gallium at its Molaoi site will add value to the company. Accelerating and focusing on this site has clearly become a priority. It would come as no surprise for the Greek government to ensure that speed is of the essence to production. This is considering European demand and need for both these metals which feature on their critical metals lists.

More testing and drilling, as well as resources estimates are likely to follow. We expect positive results to bump the stock price higher. Should the feasibility studies also prove to have a positive outcome, we would expect the stock price to bump higher.

However, for the importance of these metals, and the discovery at the Molaoi site, you must be aware of the significant risks involved with Rockfire.

Risks

Firstly, this is an exploration company. This means that there’s no guarantee that what they find will actually make it to production and commercial sales. As noted, the requirement of feasibility studies will be required before the actual process of mining, extraction and production.

These are all things that require capital inputs. As with most exploration miners, that means capital raises. You should expect there to be further capital raises down the track. If that comes, you should expect that if you don’t participate, you will be diluted by future raises.

That is, of course, in the future. We don’t know for sure that these will come. However, we’d be incredibly surprised if they didn’t. Having conducted a raise in June to an institutional placement, the company raised an additional £880,000 to further the resource upgrade drilling and mineral resource at Molaoi.

It is likely that these sorts of raises are where retail investors can’t participate. So again, just be aware that these dilutive raises are likely to come as well.

If the mine for whatever reason proves to be commercially unviable, the stock will lose the jewel in its crown, so to speak. While it has other exploration projects, our view is that Molaoi is the value and stock price driver.

If Molaoi is not viable long term, we will be out of the stock and would expect a heavy loss on the position.

The stock is also tiny, with a market capitalisation of £4.9 million and a stock price of 0.25GBp. It’s one of the smallest stocks we’ve ever recommended to you. Volume in trading is around 2.6 million per day. However, at that stock price, that’s only around £7,000 of volume per day.

The reason we’re bringing it to you is because there are few companies on the London market that have both germanium and gallium resources that are small enough to make the asymmetric risk profile worth it.

Furthermore, with the company’s view to production at Molaoi in three years, that also fits our longer-term horizon for the stocks we look for.

The stock price will move on our recommendation. It’s advisable to ensure you stick within the buy limits so you’re not overpaying and not bidding for stock due to the movement from our recommendation.

If the stock pops over the buy limit, then be patient. There’s a good chance it may retrace back soon thereafter in absence of further positive announcements from the company.

This is one of those asymmetric risk plays that we love to uncover. Yes, it’s small, illiquid and highly risky as an explorative miner. But the demand and need for the West to secure supply of critical metals like gallium and germanium can’t be underestimated.

To have a miner with an exploration licence (for 30 years) in an EU state, with a confirmed presence of both germanium and gallium and aims for production within three years, this makes the risk worth it in this instance for such a small, risky company.

The point here is that you don’t need a huge capital investment for the potential upside, nor should you with something this risky. Always remember with stocks like this to never invest more than you’re prepared to lose.

Buying instructions

BUY Rockfire Resources (LSE:ROCK). Current price 0.25GBp, buy up to 0.35Gbp. This stock is illiquid. It may spike on our recommendation. Stick to the buy limits. Due to the volatility of tiny exploration companies, we won’t be using a stop loss on the stock. However, should the price head lower we will consider appropriate exit if the fundamental investment case falters.

Big breakthroughs

Picture this: a colossal expanse of solar panels, measuring ten kilometres by ten kilometres, positioned in geosynchronous orbit, working tirelessly to harvest solar energy that’s then beamed down to Earth through an expansive network of antennas.

A receiver with a diameter of a few kilometres is established on the Earth’s surface to capture the power and subsequently channel it into the grid.

What’s not to like? Space-based solar power is – or would be – the highest-intensity solar power you can get, available 24/7, and it can be sent anywhere on Earth.

You might find this scenario reminiscent of science fiction, akin to the futuristic visions penned by visionaries such as Isaac Asimov. However, this concept, which has been a clean energy dream for decades, is perhaps not as far-fetched as it may seem.

In fact, in June, researchers at the California Institute of Technology (Caltech) said that a small-scale space solar power prototype was able to beam a small amount of power to Earth – an important first for the nascent technology.

The prototype – launched into space via a SpaceX-powered spacecraft in January – contained solar cells and an array of transmitters that beamed power through space and ultimately back to the university.

For it to work, the photovoltaic cells first converted the sunlight in space into electricity, which was then transmitted wirelessly as radiofrequency (RF) waves to receiver arrays – situated about a foot away from a transmitter – that finally converted the microwaves back to direct current (DC) electricity.

(Caltech has a video explainer here.)

As well as lighting up a couple of light-emitting diodes (LEDs), the prototype also beamed a “detectable” amount of power down to a receiver on the rooftop of a Caltech lab in Pasadena, California.

This was the first time anyone had ever demonstrated wireless energy transfer in the harsh environment of space, where the prototype was subject to large swings in temperature and exposure to solar radiation.

Although only a small amount of power was beamed back to Earth, larger-scale units will soon be put to test.

Indeed, the scientists at Caltech think solar panels in space, which can soak up unfiltered sunlight around the clock with no setting sun, might one day be able to generate up to eight times as much electricity as land-based solar panels, where terrestrial limitations such as fluctuating weather patterns, night-time darkness and land availability all act to impede the full realisation of solar’s potential.

Certainly, the ability to collect solar energy 24/7, regardless of weather conditions or geographic location, certainly sets space-based solar power apart from its terrestrial counterpart.

Caltech’s breakthrough paves the way for several advantages that space-based solar power can offer:

- Continuous energy generation: solar panels in space can generate power without interruption, providing a consistent energy supply around the clock.

- Global accessibility: the energy collected in space can be transmitted to any location on Earth, ensuring equitable access to clean energy resources.

- Reduced carbon footprint: by utilising solar energy, space-based power systems could contribute to a reduction in greenhouse gas emissions.

However, several challenges must be addressed before space-based solar power becomes a mainstream energy solution, such as:

- Cost: launching solar panels and associated infrastructure into space is currently an expensive endeavour so developing cost-effective launch technologies will be essential to making the concept economically viable. However, SpaceX has pioneered reusable rockets that have dramatically reduced the cost of launches. And the mass production of satellites has brought down the cost of hardware, too.

- Efficiency: optimising the efficiency of energy conversion, transmission and reception is crucial to minimising energy loss during the process.

- Safety concerns: transmitting energy via RF waves raises concerns about potential health and environmental impacts. Rigorous safety standards and research will be necessary to mitigate any risks.

Certainly, Caltech’s breakthrough in successfully demonstrating wireless power transmission from space to Earth serves as a catalyst for further research and innovation in the realm of space-based solar power.

Other researchers around the world are also racing to make similar progress with funding from governments trying to reach their climate goals, all working on various iterations of the idea.

In June, the UK announced £4.3 million in government funding for several research initiatives. That includes a group at Queen Mary University of London developing its own wireless system for beaming microwave energy from place to place.

Meanwhile, the US Naval Research Laboratory launched an experiment on the International Space Station earlier this year with the goal of beaming power across space using laser transmitters.

Of course, as technology advances and economies of scale come into play, the feasibility of large-scale solar power satellites becomes more achievable.

According to Sanjay Vijendran, lead for the Solaris initiative on space-based solar power at the European Space Agency, space-based solar is much closer to commercialisation than nuclear fusion, which garners a lot more attention and funding.

The most ambitious timeline so far is for this technology to be ready to power homes and businesses on Earth by 2050, says Xiaodong Chen, a professor of microwave engineering at Queen Mary University of London.

Although that sounds unrealistic, it’s also true that developments in space technology warrant some cautious optimism about space-based solar.

Certainly, Caltech’s recent breakthrough in space-based solar power marks a significant milestone in long-standing dreams to harness this limitless clean energy source from space here on Earth.

Buy List update

Ashtead Technology Holdings PLC (AIM: AT)

Subsea equipment rental company Ashtead Technology Holdings, recommended at 374p in the July issue of Small Cap Investigator, has enjoyed a decent first month in the model portfolio, rising 12% at the time of writing to 420p.

Ashtead has a history supplying subsea services to the oil and gas sector but has diversified into the fast-growing offshore wind market.

The AIM-traded firm saw revenue for the six months to June rise by 57% to just under £50 million driven by “continued high demand across both offshore renewables and offshore oil and gas”.

Offshore oil and gas revenue grew by 50% to £33.5 million, while renewables revenue increased by 74% to £16.3 million. Meanwhile, group like-for-like turnover rose 40% with acquisitions contributing around 14% growth and around 3% coming from currency movements.

A rise in inflation allowed the AIM-listed company to increase its pricing, which contributed to gross profit rising by almost 69% to £39.3 million, taking the gross margin to 78.8%.

The spike in exploration following the rise in energy prices also saw Ashtead’s equipment get more use and installation.

Chief executive Allan Pirie said the firm’s strongest ever set of interim results were thanks to “continued positive momentum through the first half of 2023, with the group benefiting from our strategic investment in people and equipment, together with further increases to both utilisation and pricing”.

Although growth is expected to moderate in the second half, after the “unseasonal” strength of the last year’s final quarter, “market fundamentals remain strong” and the full-year outturn is now seen well ahead of the board’s previous guidance, added Pirie.

The stock remains a HOLD while it trades above 395p.

European Metals Holdings (AIM: EMH)

At the time of writing, European Metals Holdings is trading around 40p, over 21% up in the model portfolio, although the stock has fallen from 49p at the end of July.

At the end of July, the Australia-based lithium mining company European Metals said its latest quarter (to end June) had seen its Cinovec lithium/tin project make further good progress.

Highlights included a site visit from the Czech prime minister and securing the land required to build the lithium processing plant.

EMH added that the definitive feasibility study currently being undertaken on Cinovec by DRA Global is on track for completion in the final quarter of this year.

The extension in the time forecast for the DFS completion plus optimising the flowsheet had increased the cost by around €6.86 million.

On 30 June, the company’s total cash was AU$8.9 million.

Cinovec is being developed by Geomet, a 51/49% joint venture between state-owned CEZ and EMH.

Cinovec will be a significant pure lithium producer in the EU – a region where there is little domestic raw material production and a region with a huge demand as it battles to achieve a carbon-neutral future.

The stock remains a BUY below its 45p buy limit.

Central Asia Metals (AIM: CAML)

Copper producer Central Asia Metals has risen from around 175p on 6 July to 206p at the time of writing, still leaving it 25% underwater in the model portfolio.

The stock’s performance has closely followed the decline in copper prices during 2023. These prices have fallen due to lower-than-expected demand for the critical metal, primarily due to China’s struggling economy and the overall slowdown in global economic growth.

As of now, the cash price of copper on the London Metal Exchange has dropped by 11% since its peak in mid-January, when it was above $9,400 per metric tonne. The current price stands at $8,359.

However, copper is set to embark on a new energy transition super-cycle, according to analysts such as Max Layton at Citi Bank.

“For us here at Citi, copper is the energy transition bull trade. The world is cyclically weak right now, and that means the trade is on pause. But copper’s eventual bull run is likely to make oil’s famous 2008 rally look like child’s play,” said Layton, Citi’s managing director for commodities research, in a 23 August video presentation for clients.

That should certainly help Central Asia Metals, which was recently recommended as a “buy” by the Sunday Times’s Lucy Tobin on 6 August.

Although higher costs and investment since 2022 had hit CAML’s performance, alongside the tumbling price of copper, production costs were low overall and the miner had good cashflow, a strong balance sheet, zero debt and decent dividends, noted Tobin.

The long-term outlook for copper prices was also good, given its vital role in electric vehicle manufacturing and decarbonisation initiatives.

On top of that, trading on just 6.2 times earnings, the shares looked “oversold”, said Tobin.

The company’s stated deal-making ambitions might be one reason for investors’ “sniffiness”, she added.

Yet analyst Peter Mallin-Jones at Peel Hunt believed that the company’s cash position underpinned its payout and opened up options for strategic acquisitions.

For his part, Richard Hatch at Berenberg judged that the miner was “among the lowest-risk, highest-yielding stocks of our coverage, yet it remains overlooked from a valuation standpoint. We would encourage investors to revisit the investment case of this quality name.”

“Buy”, said Tobin.

Elsewhere, broker Canaccord Genuity set a target price of 265p for the company.

The stock remains a BUY under 310p.

Foresight Sustainable Forestry Company (LON: FSF)

Foresight Sustainable Forestry Company, which invests in UK forestry and afforestation assets, was last seen around 97p, a couple of pennies down month on month around 11% down in the portfolio.

Since launching at the tail end of 2021, FSF has built up a forestry portfolio of about 12,000 hectares across 65 properties and has raised £175 million. It is targeting a return of more than 5% ahead of inflation measured over a five-year average timeframe.

In its interim results published in June, it reported that it had delivered net asset value (NAV) per ordinary share returns of 10.6% since its initial public offering (IPO) in November 2021.

FSF also noted in its interim report that it recorded a profit for the period ending 31 March of £6 million. This was down from £7.9 million 12 months previously. Its unaudited NAV was £186.6 million, having increased from £180.6 million six months previously. NAV per ordinary share was up by 3.5p over the same period to 108.5p.

“Our target is to get to half a billion [pounds] of NAV within four to five years of launch,” FSF co-lead Robert Guest said in an interview with The Scotsman newspaper on 11 August.

“That’s not helped by current equity market conditions, but it’s still achievable, if interest rates can come under control, if inflation can come under control… we’ve got a platform to grow from.”

Guest said that part of FSF’s aim is to provide sustainable timber production amid a prevailing global imbalance between supply and demand, with the latter expected to grow to four times its current size by 2050.

Timber is versatile, very low carbon, and “a good thing to invest in,” he added.

FSF’s portfolio also continues to expand, with the fund noting its interim results that it had planted about a million trees at four afforestation schemes, creating an additional 107,500 or so voluntary carbon credit pending issuance units.

“The expansion of the number of carbon credits in FSF’s portfolio means that as at 31 March, carbon credits were valued at £2.5m,” it said, adding that it has 34 further afforestation properties in the portfolio set to be planted in 2024 and 2025.

Furthermore, Guest said in the interview that he believes FSF could lock down more “opportunistic” acquisitions, tapping into its £30 million revolving credit facility, and potentially also raising new equity.

As such, it remains a BUY under 150p.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF has fallen from around £9 at the end of July to around £8.44 at the time of writing, 5.87% below our £8.96 entry price.

There are currently 40 holdings in the Global X Lithium ETF, with Albemarle Corporation being the top holding with about 9.08% of the fund’s total share currently.

The underlying Solactive Global Lithium Index tracks the performance of the largest and most-liquid listed companies that are active in the exploration and mining of lithium, or the production of lithium batteries.

Overall, the fund is designed to mostly react to the global electric vehicle (EV) growth trend, though is not tied specifically to the fate of miners, but rather a mix comprising the entire EV supply chain.

As reported by the deep dive, Lithium carbonate prices have fallen over the last few weeks. After stabilising at around $42,000 per tonne from the end of May through mid-July, spot prices have retreated to $30,000 per tonne.

Lithium prices had bounced off the $22,750/tonne level in late April 2023 after a whopping 75% fall over the previous six months. However, it appears that battery manufacturers have pulled back their buying of lithium since the start of the third quarter as inventories have piled up.

One likely reason for this is the lacklustre Chinese macroeconomic backdrop, which seems to have translated into a slowing of consumer demand for EVs. EV sales in China fell 3.2% in July to 780,000 units from 806,000 vehicles in June, according to the China Association of Automobile Manufacturers (CAAM). However, July unit sales were up nearly 32% versus year-ago levels.

What’s more, major lithium producers are eying price recovery with buyers expected to restock soon.

US-headquartered lithium producers Albemarle and Livent said they are expecting lithium spot prices to recover from recent weakness because they foresee a brighter demand picture for the remainder of the year.

The Global X Lithium & Battery Tech ETF remains a BUY.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation, the world’s largest gold miner, was trading around $39.32, just down from prices around $43 at the end of July. The stock is now but 40% below our $65.39 entry point.

The continuing suspension of operations at its Penasquito mine in Mexico, which has been shut since 6 June, continue to weigh on the stock, with the timing of a restart still uncertain.

However, the near-term trend for gold prices appears bullish and Newmont’s production outlook also looks positive.

The company’s gold mineral reserves stand at about 96 million ounces as of the end of 2022, a large portion of which is located in low-risk regions such as North America.

What’s more, in May, Newmont agreed to buy Newcrest, a low-cost gold and copper player based in Australia for AU$26.2 billion. This should help Newmont with its margins. The deal will also boost Newmont’s production of copper, which, as said above, is vital for the fast-growing green energy economy.

Newmont said on 11 August it had received clearance from Australia’s competition regulator to proceed with its proposed takeover of Newcrest, which would be the third-largest deal ever involving an Australian company.

Newmont continues advancing other regulatory approvals and expects to close the transaction in the fourth quarter of this year, it said.

UBS bank said there are plenty of upside catalysts once the Newcrest acquisition is closed later this year.

“In our view, divesting several of the smaller mines to increase share buybacks, recasting capex plans and providing updated operating guidance on a combined basis are all potential positive catalysts,”, the bank said in a note.

“On the downside, we assume Penasquito restarts at the end of Q3, so prolonged downtime would drive our estimates lower.”

Newmont remains a BUY under $100.

DS Smith (LON: SMDS)

Recycled-content paperboard and packaging producer DS Smith has risen from around 271p at the end of June to 309p at the time of writing, now just around 2% below our entry price.

On 24 August the firm announced it has entered into an agreement to acquire Serbian packaging company Bosis doo.

The price of the deal was not disclosed.

The acquisition is complementary to the business’ existing regional packaging activity in Eastern Europe and will support its growth drive in the region, according to the accompanying press release.

Following completion of the acquisition of Bosis, DS Smith’s total packaging operations in Eastern Europe will comprise 29 box plants and additional facilities, employing more than 7,000 people in the region.

Situated c.100km south of Belgrade, Serbia, the family-owned business was founded in 1982 and employs 140 employees working on a single site in Valjevo.

Separately, DS Smith is still considering selling six of its UK recycling sites in the UK.

According to reports, it is understood the company could sell its recycling depots to waste management companies or even to existing merchants. Sales are expected to include the baling equipment and other infrastructure.

DS Smith is at the centre of the UK cardbord recycling market as it supplies major users of cardboard packaging, including online giant Amazon.

With retail volumes often now coming direct from retail hubs, the depots are thought to be less important to the papermaking business.

In June, the firm suffered the first decline in demand for its packaging in over a decade, as the rising cost of living hit spending on online shopping from the US to Europe.

The stock remains a BUY though we are watching market dynamics closely.

Aura Energy (LON: AURA), Yellow Cake (LON: YCA) and Sprott Global Uranium Miners ETF (LON: URNM)

There’s a reason why we’ve put these three companies together under one update. That’s because the uranium market is getting some tailwinds behind it again.

The spot price of uranium is up around $58.50/lbs. This is up around 20% since the start of the year.

According to the Financial Times, part of the reason for this surrounds a potential coup in Niger and overall increases in demand for the nuclear energy fuel. Add to the mix that uranium is becoming “hot” amongst retail investors and suddenly stocks like Yellow Cake and Aura are starting to shift higher, with exchange-traded funds (ETFs) like Sprott Global Uranium Miners seeing increases in inflows.

In fact, according to HANetf, Sprott Global Uranium Miners ETF surpassed $75 million assets under management for the first time since its inception. The CEO of HANetf, Hector McNeil, commented:

“We are delighted to witness URNM’s rapid growth and its surpassing of $75 million in AUM. Uranium is in high demand, as evidenced by its strong performance against other commodities so far this year. There is a dual need for countries to gain energy security, and also achieve net-zero targets in response to increasing legislation.”

This is all positive momentum for the uranium sector. It’s also seen the stock prices of these plays trend higher again.

Our view on nuclear energy and the demand for uranium is long term. The direction and momentum we’re now seeing reaffirms our view. We continue to be bullish on the whole sector and these direct ways to play it.

CentralNic Group (LON: TIG)

This week, CentralNic completed a name and ticker change. The company will now trade as Team Internet Group and its ticker is TIG. This means that if you want to trade the stock, the ticker you’ll need is TIG.

Mirriad Advertising (LON: MIRI)

Despite some positive news in 2023 around its collaboration with Microsoft, Mirriad has continued to struggle, both financially and in terms of its stock price.

The company’s interim results forecast sufficient cash at hand (and no debt) to see a runway to August 2024. That’s good as it buys Mirriad some time to get the company back on track and to see some more meaningful revenues flow through, which the company is expecting.

But Mirriad is looking like it will be on the chopping block soon if it can’t start to turn the ship around in the next few months. We won’t be waiting until August next year to see if the company can do it. Instead, if in Q1 2024 there’s no big turnaround to suggest that some of the losses can be made back, then we’ll look to offload this disappointing play. Still, we’ll give it some time. Mirriad’s anticipation of programmatic revenues in 2024 may just be enough to get the tailwinds pumping behind the stock again.

We continue to see if progress actually comes or not. We will make a decision on it in the new year, unless earlier action is otherwise needed.

PodPoint Group (LON: PODP)

PodPoint is another holding we continue to keep a close eye on. While the company is winning new contracts, the company’s half-year report showed it was struggling to penetrate the residential (home) market which is a key focus of the group.

There’s an upcoming capital markets event on 16 November that we anticipate will be a make-or-break moment for the company. It expects to present its “Powering Up” transformation plan at the event. We eagerly anticipate its outline for growth plans, product development and strategy going forward.

Another point to note is that if the UK government winds back the goal of banning new petrol and diesel car sales by 2030, this is likely going to hit the PodPoint stock price further. We will stick with PodPoint to see if the management has a robust plan for moving forward. If it disappoints, we’ll exit this underperformer. Likewise, if the government removes the prospective ban on internal combustion engine (ICE) cars, we believe this would be another catalyst to exit the stock.

We keep an eye on it and will keep you updated.

Inside the lives of James and Sam

James:

Navigating overseas travel – particularly air travel – as an adult often demands patience and resilience. The combination of long security queues, cramped airplane seating, busy waiting areas, unhelpful border agents and fellow irritable passengers can make even the most seasoned traveller doubt their travel decisions.

But throw a toddler into the equation, and it can seem as though you’ve drenched the entire ordeal in accelerant and struck the match.

So with the stresses of our tortuous house build also mounting up, my girlfriend and I decided we could do without the hassle of travelling overseas with our three-year-old this summer, so we forewent the lure of hot sunny beaches and faraway shores for a holiday in the UK instead.

We had ten days in Wiltshire in South West England where we had the run of a large house, complete with an indoor swimming pool and surrounding fields.

It’s fair to say it wasn’t the most glamorous or exotic of holidays we’ve ever had, but it was brilliant, nonetheless, and just what the proverbial holiday doctor ordered.

The kids loved scavenging for potatoes in the garden’s vegetable patch while I found myself whiling away the hours, beer in hand, pond-side with a large net, fishing out all the blanket weed and other algae that seemed to multiply by the second – an activity you’d not normally find in the regular holiday brochures, granted, but extremely relaxing all the same.

We also took on a few day trips, including visits to Peppa Pig World in the New Forest, Old Wardour Castle near Tisbury, a friend’s house in Hampshire and a late afternoon trip to Stonehenge.

The weather certainly obliged though it was by no means scorching or even particularly sunny – which certainly saved an hour or so each day chasing a toddler around with sun lotion in hand.

After years of travelling overseas every summer, it was certainly a nice change to staycation in the UK instead and one I’d be more than happy to do again – though it does seem I’m increasingly in the minority.

Indeed, according to a recent article by Bloomberg, the UK staycation boom of the recent Covid years has now officially ended.

The number of holiday-let limited companies set to be struck off the Companies House register – which normally happens when a business is being wound up, voluntarily or due to unpaid debt – rose from just over 300 in July 2021 to more than 550 in July this year, according to data from estate agent Hamptons, Bloomberg reported.

What’s more, Simply Sea Views, a website listing cottages around the British coast, said its bookings were 12% lower in the first half of 2023 compared with 2021. Last year saw a particularly sharp drop, with Cornwall down by a quarter after gaining the most new lettings during the pandemic.

“The pendulum well and truly swung back from the 2021 staycation boom,” said Josh Williams, Simply Sea Views’ owner.

Conversely, London’s Heathrow airport reported 37 million passengers in the first half, compared with 26 million in the same period last year, while travel company TUI AG’s UK bookings this summer were 4% higher than pre-pandemic levels, Bloomberg said.

For investors, the return to normal holidaying habits post-Covid might mean prospective landlords in places such as Cornwall or Devon might now opt for long-term rentals rather than holiday lets, though these trends are certainly not set in stone.

In the long run, the local holiday let sector could even get a reprieve from climate change. Scorching summers in the Mediterranean, which saw heatwaves and wildfires in July and August, may convince people to return, once again, to the UK’s own coastal attractions.

And, of course, let’s not forget the travel chaos of the recent bank holiday weekend, where thousands of holidaymakers found themselves stranded at airports across Europe after a major outage caused a network-wide failure in Britain’s air traffic control system.

With some passengers being left on board grounded planes for hours at a time, it’s safe to say there were plenty of holidaymakers who wished they had stayed at home instead – even those without toddlers.

Peppa Pig World!

Sam:

It’s currently 29 degrees, sunny and I just had a visit in my office from my boys. They’ve been picking oranges and lemons off the trees in the gardens.

That means, the Volkering household has moved to Portugal. We did it in a couple of shifts. Well, two shifts to be precise. I got the good end of the deal: two and a half days in the car, 2,455.8 km with a loaded car, a cat and a dog.

Proof of range

An overnight stay with the boys!

My wife spent two and a half hours on the plane. But she had the boys, ages two and four. So yes, I got the good deal.

Sun, beach, outdoor living, tax, cost of living – in that order – are the reasons why we decided to live abroad for a while. It’s not an uncommon practice for editors here at Southbank Investment Research to hop around a bit. In fact, just last week, John Butler wrote an excellent piece on it all which you should read here.

I say “abroad” but perhaps I should say “abroad from abroad”. I am after all Australian by birth, lived there for a big chunk of my life, then spent the last ten years in the UK, and now live in Portugal.

I’m Australian, my boys are British, with Aussie passports, as is my wife, and if things go to plan, they’ll have another passport in the coffers in another five years or so. Is that the trick to it all? Collecting as many passports as you can for your kids to give them opportunities anywhere in the world?

While it seems like the world is closing in on itself, with nationalistic issues at the heart of so much contention in countries around the world, maybe the most valuable thing is to get as many passports as you can.

Nonetheless, that’s not really what I was thinking on my 2,455.8-km drive.

When you’re hammering it across Europe’s motorways, you really do get to hammer it. Set the cruise control at a mix of 120 kph to 130 kph (give or take a few kph…) and let it rip.

As we (me, cat and dog) watched the k’s tick by at rapido pace, I started to get excited when the range to empty on the car started to extend further and further. In fact, as you can see from my photo above, my average fuel consumption was 6.8 L/100 km.

Now I know my car is telling a lie. My fuel tank capacity is 65 litres. But I was doing over 1,000 km per tank of fuel on my trip. I was able to get to 1,000 km before I decided to fill up again. And my projected range was another 70 km.

In other words, my average consumption was closer to 6 L/100 km than to 7 L/100 km.

I was chuffed with that.

As I tore across the continent, whenever I did stop, the smattering of electric vehicles (EVs) was obvious to see. Charging stations everywhere (most empty and taking up car spaces that could go to mobility or family spots). But I would stop, grab a snack and go. And if it was time to fill up (on the rare occasion I needed to) I’d be in and out within five minutes (and that included a pee, grabbing a drink and paying).

There’s not a single EV on sale today that comes close to getting the kind of range I was with my car. Not a single EV in sight that provides the convenience that a diesel car can do. And until there is, I won’t be buying one.

I suspect with advances in technology, synthetic fuels, a backtracking on net zero policies and other factors in play, I might never have to buy an EV. And that would suit me just fine.

Have you taken a long road trip in an EV? How did it play out for you? Good? Bad? Am I off the mark, am I missing something about EVs? Or are you like me and can’t fathom the idea of a 2,455.8 km road trip in anything but a “dirty” fuel-powered car? I’d love to hear your thoughts, feel free to send them to us at feedback@southbankresearch.com.

Crypto Corner

I’ve just got back from a couple weeks of holiday. As you’ll have read in our section on what we’ve been up to behind the scenes, I’ve been in the process of moving country.

I’m now based in Portugal. The reasons why are numerous. Providing a lifestyle for my boys that is similar to what I had as a kid growing up in Australia was a big factor. So too was the ability to only remain a couple hours away from London, which was why Portugal fit the bill.

There are also other considerations and benefits too. If you’ve been around crypto a while, you’ll know another benefit (at least for now) is the favourable treatment regarding crypto assets.

That also helped sway the decision-making process.

Nonetheless, today’s Crypto Corner isn’t about the benefits of moving country for more favourable treatment of crypto assets. Although that is probably worth a deep-dive report anyway.

What is at the forefront of the industry’s mind right now is the impending approvals (or rejections) of bitcoin exchange-traded funds (ETFs) in the US.

The most significant development in this was a federal appeals court in the US ordering the US Securities and Exchange Commission (SEC) to review its rejection of the Greyscale Bitcoin Trust’s conversion to a bitcoin ETF.

In short, this means a federal court has said the SEC has not applied the correct process and decision-making to the rejection of Greyscale’s application.

That’s significant, as it indicates the court agrees with the overriding view that the SEC is not doing its job properly when it comes to crypto.

What makes the rejections of the sporty bitcoin ETFs so confusing is that the SEC was more than happy to approve bitcoin futures funds, including a leveraged product. But when it comes to ETFs backed by underlying bitcoin, the SEC has rejected every application so far.

If the Greyscale ETF conversion is approved, it may very well be the first domino to fall in many spot bitcoin ETFs now waiting for approval.

It should be said the Greyscale ETF isn’t the be-all and end-all for future bitcoin ETFs. The fund in its current form is a strange beast. As a fund it has high fees. The price trades at a 20% discount to net asset value, which indicates there’s some question and concern about the fund, redemptions and the liquidity of the fund if investors wanted their investments back.

I expect a lot of the questions and concerns around Greyscale will clear up with an ETF. For one, redemptions would be easier. Also, while the fund is at a discount to net asset value (NAV), that’s been closing as of late, and with an ETF I’d expect the fund to trade a lot closer to the NAV.

The major factor in play with Greyscale becoming an ETF is that in doing so, a path of little resistance will be created for others. It may also be the case that the SEC is wanting to have a bigger player (like BlackRock) in the bitcoin ETF space first. Therefore, when Greyscale is (hopefully) greenlit for ETF conversion, the big players can catch the outflows from Greyscale to a more “reliable” player in the market.

Which means that although ETF applications from BlackRock, ARK Invest, Van Eyk and Fidelity may still be some months off, they are, in my view, an inevitability in the market. The court order to review Greyscale just reinforces that point.

That said, we’re only talking about bitcoin ETF approval in the US. There are already bitcoin ETFs in other places around the world… sort of.

ETC Group has a physical bitcoin exchange-traded product (ETP) that’s listed on the XETRA exchange in Europe. An ETP is virtually the same as an ETF. The difference is semantics, as the ETC Group ETP is 100% backed by physical bitcoin. You can see for yourself all about it here.

There are others including those from 21shares (see here) and from Coinshares (see here) again, the only thing is these aren’t out of the US.

So, all this talk about the “first” ETF is actually nonsense. But that doesn’t negate the fact the US market is huge. It’s also highly accessible. It’s more accessible and has greater capital flow than the European markets.

In that sense it is important that these ETF approvals are given. Not necessarily because of what bitcoin represents, but because of the wider acceptance it delivers.

It’s hard to pinpoint if these US ETFs are a good thing or not.

Consideration has to be given to the fact that none of these are what bitcoin is really about. These ETFs are controlled and custodied by centralised institutions, gatekeepers of finance. They won’t be for everyone and they won’t be accessible for everyone. You don’t need their permission either if you want to get bitcoin.

If you want to hold bitcoin, go get some. You know this, and you know how easy it can be. But what these ETFs do provide access to is capital that wants to find its way into bitcoin that currently can’t.

I think that’s the bigger picture that a lot of the industry misses. I don’t see ETF approval as that big of a deal for crypto people. What I see it doing is giving that element of trust to investors that continue to be sceptical of it all.

You don’t need convincing (or maybe you still do?) that bitcoin is no scam, fad, Ponzi or flash in the pan. But I know many people still do. What institutions bring when they launch something like a bitcoin ETF is acceptance, validation from the “TradFi” crowd and, importantly, a lot of capital at the gate.

I’ve said it before, but you have to consider the huge amounts of capital that can’t get into crypto and bitcoin because of the problems with traditional finance (TradFi). I use myself as an example…

I have money in a superannuation fund (pension) in Australia. The choices for me to invest in anything crypto-related don’t exist. What a bitcoin ETF might provide is a “TradFi-acceptable” way to invest in the asset class.

An ETF would meet certain rules and restrictions around things like custody and risk mitigation that direct crypto ownership doesn’t satisfy in the TradFi world. It would give my capital (currently blocked from crypto) a pathway into bitcoin – 100% I would move a portion of my capital into a bitcoin ETF because it would be the only way that capital could get into bitcoin.

Relatively speaking my balance is nothing compared to the capital that others would have. Think of all the baby boomers with more than $1 million in their Aussie superannuation funds – again, most of them have no practical way to invest in bitcoin in their funds. Unless a regulated bitcoin spot ETF is available.

And if we’re only looking at Australia, a small (population) country with more than $3.5 trillion of assets in superannuation, even a fraction of all that being able to legally access a bitcoin ETF… the potential capital flow is huge.

So, this is why a bitcoin ETF isn’t the worst thing in the world for the crypto “purists”. When you properly understand how the world’s TradFi system works, and where capital still sits at the gate, some of that finding its way into bitcoin – even if via an ETF – can’t be the worst thing in the world at all. In fact, it’s probably a healthy thing for the longevity and future of bitcoin and the wider crypto world.

What else we’ve been looking at this month

James:

The gas market state of play

One year ago, European gas prices stood at around €220/MWh. Today they’re trading around €35/MWh, putting it close to the average price of the 2010s once you adjust for inflation. Although prices have tanked, it’s clear risks still abound as we head into the winter heating season.

If you want to get a handle on the current setup for the natural gas market, then check out this article by consultancy Timera Energy, which uses five charts to set out the state of play ahead of winter. The article details how expectations have changed versus this time last year and what to watch this winter.

After reading the piece, it strikes me that a thermometer might be any gas trader’s best investment for trading the market this winter.

How a small EV maker became the third most valuable auto manufacture

An unprofitable electric vehicle maker hailing from Vietnam has suddenly become the third most valuable auto manufacturer in the world, leaving the likes of General Motors Co. and Ford Motor Co. in its dust.

As reported by Bloomberg, shares of Vietnam’s VinFast Auto have soared almost 700% since it listed in mid-August even though it hasn’t made many cars yet, let alone turned a profit. By Monday 28 August, VinFast was worth $200 billion, behind only Tesla and Toyota in the automaker sector, but worth more than Goldman Sachs and Boeing.

If you want to read what’s behind the epic rise, and why investors would be wise to refrain from piling in, then take a read of this article on Quartz.

The fightback against climate doomism

Climate “doomers” believe the world has already lost the battle against global warming. That’s wrong – and while that view is spreading online, there are others such as Assaad W. Razzouk, a Lebanese-British clean energy entrepreneur, author, podcaster and commentator, who are fighting the viral tide.

Every week Razzouk aggregates good climate news on his Twitter feed to show that climate action is widespread – and has momentum. The thread had been running for over three years now and should be your first port of call to find out the exciting progress being made to combat climate change.

Sam:

China’s recent moves on AI supremacy aren’t all that recent

Technically, I haven’t been reading this… however, it is something I wrote about China’s AI development plan in 2019 (you can read my piece here). It was obvious then what China’s plan of attack was: China was (is) hellbent on AI supremacy – and there’s a good chance it’ll get there. It’s worth a read to see how long this battle has been raging.

Net zero’s hypocrisy

The irony of one of the world’s most abundant uranium countries not having a nuclear energy policy (aside from it being illegal) shouldn’t be lost on anyone. Then again, Australia’s politicians have always been a confusing bunch… That should read incompetent bunch, I think.

Nonetheless, when you read that the pathway to Australia’s net zero goals is to take down an abundance of the natural environment, well, that shouldn’t be a great surprise either. A decent article on the hypocrisy of net zero in Australia (a short but powerful read).

Uranium’s real dirty secret

While on the topic of uranium, it’s important to know that when sourced properly, and used in the right way, it can be a solution to a lot of the world’s energy problems when used for nuclear fuel.

However, the history of uranium isn’t so clean as the energy it can generate. Everything always needs some perspective. If you want to get a (pretty dark) look at what that used to look like, this is a captivating read.

James Allen and Sam Volkering

Editors, Small Cap Investigator