Your December issue of Southbank Growth Advantage

20th December 2024 |

- The breakthrough tech tackling power-hungry AC and water scarcity

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

The most purchased stock in the UK (for good reason)

Sam:

In August 2013, before I started working with Southbank Investment Research, I wrote to my readers in Australia for my publication, Revolutionary Tech Investor, about the future of money.

Specifically in that report I wrote,

The way I see it is that Bitcoins will serve as a new ‘reserve currency’. In a similar way that US dollars and gold do now.

At the time, you could buy one bitcoin for $100.

A couple months later, in February 2014, I was a guest on The Rick Amato Show on US TV to talk about bitcoin. Host Rick Amato described bitcoin in his own words,

“It sounds like a bunch of bored high school kids who are very smart, trying to have a good time with something.”

On this “interview” they also surprise attacked me with a guest – software entrepreneur and “tech expert” Andrew Blount (I believe at the time he was also running for governor of California). They put him on because he wasn’t a fan of bitcoin. His sage words of wisdom were,

“It started out as a scam. It’s run its course as a scam. And it’s going to end as a scam.”

They then laughed at it (and me) and compared bitcoin to “bubble-gum wrappers”.

The interview finished with Amato asking,

“Am I oversimplifying this? What this is, is a matter of perception?”

My response,

“Yes, you are oversimplifying it. It’s much bigger than that, and it’s going to be around longer than we’re alive.”

Bitcoin was trading at around $550 at the time.

In October 2016 when I informed clued-up investors, just like you, on “How to profit when digital gold [Bitcoin] hits US$50,000”, I explained,

When the world is on the brink of financial collapse, it’s not gold, not currency, not even stocks that really flies. It’s bitcoin.

And then said,

… bitcoin could soar from US$639 now to $49,618, another 7,765% return. I wouldn’t be surprised to see it top US$50,000 for just one single bitcoin.

I repeated this prediction in my 2017 book, Crypto Revolution: Bitcoin, Cryptocurrency and the Future of Money. And again, when we updated the book in 2019.

Then on 18 March 2020, as bitcoin was crunched along with all other assets around the world and it hit a “low” of around $5,800, I sent an urgent alert to my exclusive crypto subscribers, telling them to “halt on all action… except bitcoin.”

Yet still on 3 December 2020, as bitcoin was up around $18,000, the Financial Times wrote a piece where it said, “To be completely frank, we have never heard of [Sam Volkering], but it turns out he’s written a book! Called Crypto Revolution.”

The FT then went on to say about my book,

You know when you do a £5 Secret Santa with colleagues, and you end up getting someone you secretly don’t like very much? You’re welcome.

I trawl through these examples as a reminder that for the last decade, while I’m by no means perfect, I’ve been always right about bitcoin.

And everyone that’s ever followed my advice on bitcoin and bought some, and held it, is in profit. Everyone.

Today I write to you to say that my view is that long term, bitcoin gets to $1 million. And then goes past it. Maybe forever higher, forever. By then, maybe I just stop making these forecasts. I think by then you won’t need me to.

However, this long-term view on bitcoin is one thing. How UK investors get exposure is another. Yes, anyone can go and buy bitcoin directly, we know this. I think everyone should.

But there’s also no tax effective structure in the UK that allows for that. By that I mean ISAs and SIPPs. There’s about £750 billion in ISAs in the UK. About another £205 billion in SIPPs. That’s as of 2023 as well. So realistically by now we’re probably looking at £1 trillion worth of capital that cannot buy bitcoin directly, cannot access a bitcoin spot ETF and are very restricted as to ways in which they can get exposure to bitcoin in these accounts.

But there is a way. And if you’re bullish on the long-term value of bitcoin, as I am, and you want some of your money exposed to that, without having to hold bitcoin directly and deal with the responsibility of that, or want to access exposure through something like an ISA or SIPP, then this is for you…

The Money Glitch

The urban dictionary definition of “money glitch” reads as,

A type of glitch that makes the player earn a lot of currency in video games that have virtual currency.

Right now, there’s a theory that MicroStrategy (NASDAQ:MSTR) has figured out the money glitch with its approach to a “bitcoin strategy”. Therefore, the stock is on an infinite trajectory higher.

Every fibre of experience, education and intuition says nothing can go up forever… but then again, we’re talking about bitcoin here and its impact on global finance, money, commodities and now, big-money stock markets.

So… can something go up forever?

The bitcoin and MicroStrategy bulls would say yes.

The sceptics… well, they might have you believe MicroStrategy executive chairman Michael Saylor is nothing, but a con-artist and that bitcoin is a scam.

What are we to make of this?

My view, and your latest recommendation is that Saylor is doing all he can to stack the company with bitcoin as fast as he can, and it’s setting them up to be the most valuable company in the world long term.

Which is why I’m recommending today to buy MicroStrategy (NASDAQ:MSTR).

The Bitcoin Strategy

Michael Saylor founded business intelligence software company MicroStrategy back in 1989. He served as CEO until 2022 and as executive chairman ever since.

The company as a business intelligence software company has a rocky history. It grew fast from inception in the late 80s, then burst in the dot-com bubble. It saw its stock price rise and fall dramatically through the 90s, 00s and 2010s.

But this isn’t a business intelligence software company anymore. It is now a “bitcoin development company,” thanks to Saylor.

In 2020 at the height of the pandemic, Saylor announced that MicroStrategy would be adopting a bitcoin strategy, adding bitcoin to the company’s treasury operations. As Saylor explained in an announcement on 21 December 2020,

“The acquisition of additional bitcoins announced today reaffirms our belief that bitcoin, as the world’s most widely-adopted cryptocurrency, is a dependable store of value.

[…]

“The Company continues to believe bitcoin will provide the opportunity for better returns and preserve the value of our capital over time compared to holding cash.”

At that point MicroStrategy had spent $1.125 billion adding 70,470 bitcoin to its balance sheet with an average price of $15,964 per bitcoin.

Its laser-eyed focus on bitcoin has continued in the four years since. And Saylor has been right.

His most recent announcement on X.com explains MicroStrategy has spent $25.6 billion adding 423,650 bitcoin to its balance sheet at a purchase price of $60,324 per bitcoin.

Furthermore, Saylor announced this year that MicroStrategy would be going even harder at adding bitcoin, to the tune of $42 billion in the next few years. But this is likely to be done in the coming months, such is his approach.

Buy why? Why is Saylor taking this ruthless approach to loading up MicroStrategy with as much bitcoin as possible in the shortest space of time?

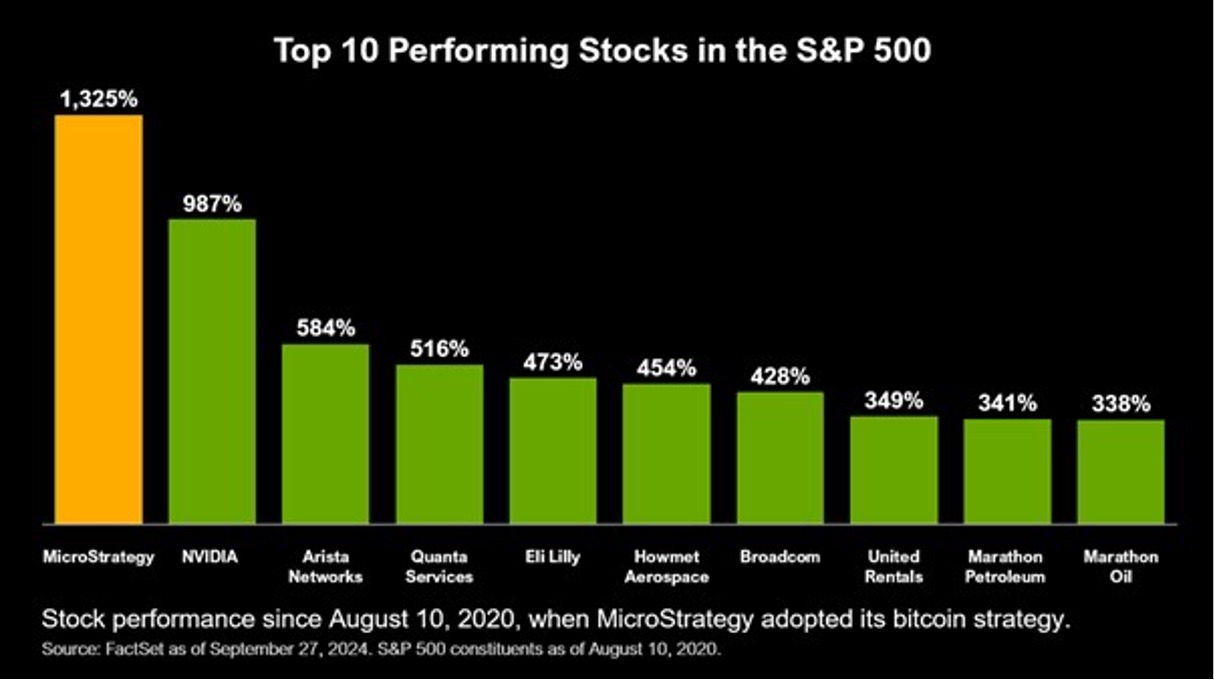

The best performing stock in the S&P 500

Saylor has turned MicroStrategy into what the company now says is “the world’s first Bitcoin development company”:

MicroStrategy (Nasdaq: MSTR) considers itself the world’s first Bitcoin development company. We are a publicly-traded operating company committed to the continued development of the bitcoin network through our activities in the financial markets, advocacy and technology innovation.

My take is that this strategy is a winning one, and that Saylor’s going to keep pushing that forward indefinitely. Whatever number of bitcoin I write about here, as you read this, the chances are that the number is higher, much higher.

In a recent interview with CNBC, Saylor explained the company’s strategy:

“We’re basically giving people different types of bitcoin exposure,”

“MicroStrategy’s mission is to securitize bitcoin and serve as the institutional bridge between traditional, mainstream investors and bitcoin.”

And it’s a relatively simple strategy: sell stock, buy bitcoin. That’s what it continues to do.

As per Saylor’s X post, he’s also made sure to remind people that since MicroStrategy adopted its bitcoin strategy, it’s the best performing stock in the S&P 500.

Source: Michael Saylor via X.com

The rising value of bitcoin directly benefits the company’s stock price due to the perception that MicroStrategy’s value is closely tied to its bitcoin reserves.

But what it’s also actively doing is raising more money to buy more bitcoin to add to its treasury.

It does this by raising capital through equity issuances and convertible debt offerings.

Essentially, the company is using the market’s faith in a longer-term higher price of bitcoin to finance more bitcoin acquisitions.

Here’s (sceptic) Peter Schiff’s take on it:

Source: @PeterSchiff via X.com

It’s worth noting that when the company issues new shares of its stock, the money goes into buying more bitcoin, but this process also dilutes holders as it increases the total number of shares. This potentially reduces the value of each share unless the price of bitcoin rises enough to offset this.

Thus far, the price of bitcoin offsets this, and by some margin. And I think it will continue to do this long term, by some margin.

Then there’s the debt issuance. Here the company borrows money by issuing bonds that can convert into stock. In fact, it expects it to convert to stock. A 2024 offering was a 0% bond (in other words, the buyers get no interest payments at all) but with a conversion price 55% above the purchase price at an implied price of $672.40.

The return from the rise in the stock price is better than the return on normal bonds. Plus, as this continues, the company continues to add bitcoin to its balance sheet returning what Saylor describes as “Bitcoin Yield”.

MicroStrategy essentially transforms itself into a bitcoin investment vehicle, or a “bitcoin development company” as noted above.

Apple or MicroStrategy?

Here’s another way to consider what MicroStrategy is doing…

Apple is a company that offers products. Those products are devices. If you like them, you buy them. Apple banks the revenues and generates a profit.

It reports on this and that flows through to eventually give some kind of determination on the value of Apple. Last quarter Apple made a $14.7 billion profit. The company trades at a price-to-earnings ratio of 36.56-times which gives it a market cap of over $3.7 trillion.

MicroStrategy also sells products. Just not the consumer kind. It sells a bitcoin product and the company itself, often to institutional buyers. This product isn’t to everyone’s taste. Those who like it hold a long view on the price of bitcoin and the importance of bitcoin in global finance, and therefore a long view on MicroStrategy. As these products are bought, MicroStrategy uses the revenues from these products to buy bitcoin.

That bitcoin it buys is the “yield” Saylor talks about.

Now, as Saylor pointed out in a recent quarter, the company had a “yield” of 88,820 bitcoin. Or at a price of $92,000, $8.2 billion for the quarter.

This approach will challenge traditional financial thinking, but that yield is about 55% of the profits Apple made for the same quarter.

MicroStrategy is not currently worth $1.95 trillion (55% of Apple’s market cap). But if you’re of the view that its bitcoin yield for shareholders is the same as profit that Apple generates for its shareholders, then you start to see where some of the crazy bullish takes on the value dynamics of MicroStrategy might lie.

For example, that $8.2 billion yield over four quarters is $32.8 billion. At a price-to-earnings ratio the same as Apple’s at 38.6-times, MicroStrategy’s market cap would be around $1.2 trillion – 14-times higher than it is now.

And that’s just based on bitcoin’s current prices. What do these numbers look like at $1 million per bitcoin? And with thousands more bitcoin adding to its balance sheet, just how valuable could MicroStrategy get?

For the UK investor, MSTR is a godsend

As mentioned earlier, what makes MicroStrategy appealing to UK investors is because the ability to invest in bitcoin in structures like ISAs and SIPPs is still very tricky and very hard.

You can’t buy bitcoin in an investment ISA, or Junior ISA, or SIPP. You also can’t buy the bitcoin exchange-traded funds (ETFs); they’re simply not offered in UK investment accounts.

So, if you’ve got a wad of cash in a personal pension you want to invest in bitcoin, how do you do it? Well, you should be looking at the company that owns more bitcoin than any other company or government in the world right now, MicroStrategy.

Because it’s a regulated, publicly listed company on a major exchange, you can buy MicroStrategy in any high street brokerage and investment account, or personal pensions that allow for direct stock ownership.

It’s easy, familiar and gets you exposure to bitcoin in places where otherwise you don’t have many options.

Risks

Now, bear in mind, this is no ready-made, steady-as-she-goes, blue-chip stock. It’s highly volatile and inherently tied to bitcoin.

There’s instances where MicroStrategy has somewhat decoupled from bitcoin’s price, but that doesn’t mean it’s immune to its wild price swings. A heavy fall in bitcoin will result in a heavy fall in MicroStrategy. It is quite likely that should bitcoin tumble hard, MicroStrategy would tumble harder. That much is very clear.

However, it’s because of the relative stability in bitcoin’s price that Saylor and the company has been able to sell more stock and grow the value of the business.

It’s primed and positioned for a strong and fast explosion higher if bitcoin takes off again. Remember, being tied to bitcoin’s price makes this inherently volatile, and high risk.

If you’re looking at MicroStrategy as an alternative to bitcoin, that’s fine, but my view is that this needs to be a long-term strategy. There will be volatile price swings short term. Getting in at the wrong time can certainly impact any long-term potential gains.

Furthermore, while the company is now very much a “bitcoin development company”, there’s significant key-man risk here. Saylor is revered in the bitcoin world and is very much the driving force for the company’s strategy.

If he were no longer in control and at the helm, there’s a great deal of risk as to what the direction of the company would then be. If, for whatever reason, Saylor were ousted, left or disappeared, re-evaluation of the position must be considered.

Other companies are also moving towards a similar strategy. Some of those include MARA Holdings, Semler Scientific and Genius Group. They’re all a long way from where MicroStrategy is right now and may never catch up. MicroStrategy now owns over 2% of all bitcoin that will ever exist, and that number will continue to grow under this strategy.

So, it’s fair to say it’ll lead this approach for a long time, maybe forever. But this is still a high-risk play as it’s tied to bitcoin and crypto markets. If you invest, use your risk capital and be prepared that you may take a loss on this position if everything moves against our view.

Buying instructions and action to take

Right now, this process of Saylor selling stock and issuing debt is keeping the stock price from shooting higher as bitcoin rockets higher.

But that won’t last long. Once he’s done selling “at the money” (ATM) stock, the price is expected to rise. I want you in, before that happens. And then the expectation in the new year is that MicroStrategy is also added to the S&P 500 indexes and passive investment capital flows into the stock further pushing the price higher.

For the UK investor, MicroStrategy is one of the best ways to play the bitcoin investment megatrend – particularly in circumstances where direct ownership of bitcoin is simply not possible.

My take is that both should be a part of a strategy – bitcoin direct ownership is something I think all investors should have. But also, from a practical sense, I understand that not all investors want the hassles that come with that, and that buying a stock is far more palatable.

In absence of the bitcoin ETFs, MicroStrategy is a great option to get exposure to the rise of bitcoin. It of course comes with risks as a form of leveraged play from within the company to add to their bitcoin holdings. So, it is high risk.

But if you take a long-term view, none of that matters in the short term and this may be one of the most exciting (but absolutely high risk) and profitable investments you’ll ever make.

Action to take: buy MicroStrategy (NASDAQ: MSTR). Current price $326.46. Buy up to $390. Set a stop loss at $175.

PS But it isn’t just MicroStrategy that I see as the only opportunity I see to ride bitcoin’s next big price surge. To find out exactly what I mean by that and how to get the details of three more stocks that I’m sharing with my Predictive Edge members, you can catch my just-released presentation here.

Big Breakthroughs

James:

In this section, I won’t focus on a major breakthrough per se. Instead, I want to discuss a potential Black Swan scenario for the coming year – one that could potentially become the most groundbreaking development in the nuclear market in a generation.

It is this: in 2025, Germany will look to reverse its anti-nuclear stance, either by reopening its old nuclear plants or committing to building its own fleet of small modular reactors (SMRs).

If you know anything about Germany’s history with nuclear power, this might sound far-fetched – an absolute about-turn. This is a country where opposition to nuclear energy has been almost cultural, shaped by disasters such as Chernobyl and Fukushima.

In fact, back in 2011, Angela Merkel bowed to public pressure and promised to phase out nuclear completely. By April 2023, Germany had gone all in on this promise, closing the doors on its last nuclear plants and pinning its hopes on renewables under the Energiewende programme.

But now? Well, the decision looks more like a self-inflicted wound, and the consequences are piling up. Energy imports are skyrocketing, electricity bills are through the roof, and the environmental benefits aren’t living up to promises.

Before ditching nuclear, Germany was an energy exporter. Now it’s the opposite. Between 2022 and 2024, the country’s import/export balance swung by a jaw-dropping 50 terawatt-hours (TWh).

That shift isn’t just inconvenient; it’s expensive. Germany now relies on costly imported energy, made worse by sanctions on Russian gas. Consumers and manufacturers are paying the price, and many companies are moving operations abroad to escape these high costs. The German economy is faltering, with some calling it a slow process of deindustrialisation.

Then there’s the cost of the Energiewende itself: a staggering €700 billion.

Contrast that with a study in the International Journal of Sustainable Energy, which estimates Germany could have spent just €36 billion keeping its nuclear plants running and building new ones. The cherry on top? This route could have slashed carbon emissions by 70%, compared to the modest 25% reduction achieved so far.

Germany’s ambitious climate goals, including achieving net zero by 2045, face critical challenges. Electricity demand is expected to jump by over 30% by 2030, driven by electrification and economic growth. Renewables alone are looking unlikely to meet all of this demand, particularly as Germany also phases out coal by 2038.

Enter nuclear power, the steady, low-carbon energy source Germany abandoned too soon. Advanced technologies such as SMRs are particularly intriguing. These compact reactors are safer, faster to build and can be scaled up or down based on energy needs.

So why do I think nuclear is making a comeback in 2025? It’s all about politics.

Snap elections are scheduled in Germany for February 2025. The Christian Democratic Union (CDU), led by Friedrich Merz, is expected to take the reins. The CDU has been openly critical of the Green-led coalition for shutting down nuclear plants during an energy crisis.

Merz himself isn’t shy about discussing nuclear power. While he’s acknowledged that restarting old plants would be challenging, he’s keen on exploring SMRs and other innovative nuclear technologies. A CDU-led government might even commission studies to see if reopening existing facilities is feasible or push forward a domestic SMR programme.

But here’s where things get interesting: nuclear power is now more popular than the Green Party itself. How did that happen?

Recent investigations revealed that Green Party officials misled the public about utilities’ willingness to keep nuclear plants running. Contrary to their claims, several plants could be restarted with relatively minor repairs, new fuel and rehired staff.

This revelation has dented the Greens’ credibility, and with Germany in an energy crunch, the public are looking for practical solutions.

Globally, nuclear energy is experiencing a renaissance. Poland is building its first nuclear plants from scratch, while Italy, which previously exited nuclear, is considering a comeback.

At COP29 in Baku, International Atomic Energy Agency (IAEA) head Rafael Grossi called a German nuclear revival “logical”, arguing that it’s essential for balancing energy security with climate goals.

Of course, reopening Germany’s nuclear plants won’t be easy. Many have been partially dismantled. Restarting them will require significant investment. But experts say the technical and financial hurdles aren’t insurmountable with the right political will.

SMRs, in particular, offer a clean slate. Their modular design means quicker construction and easier integration into Germany’s existing grid. Plus, they address long-standing concerns about safety and nuclear waste, making them a palatable option for a country still cautious about atomic energy.

By 2025, Germany’s energy and economic crises, paired with shifting political winds, will make a nuclear comeback not just logical but necessary. A CDU-led government could reopen the conversation about nuclear energy, possibly restarting plants or spearheading a bold SMR initiative.

The stakes are huge, but so is the potential reward. If Germany can embrace nuclear again, it could set an example for other nations wrestling with similar challenges. Reintegrating nuclear into its energy mix would signal a new era of innovation, resilience and climate leadership.

2025 might just be the year Germany takes a bold step back toward the nuclear future it once abandoned.

While this is not guaranteed to happen, it is certainly possible. If it does, it would be profoundly significant not only for Germany and Europe but also prove that even the most entrenched policies can change when circumstances demand it.

Buy List update

Dot Digital (LON: DOTD)

Dot Digital has been in our portfolio for over a year and a half now. The marketing platform company had been integrating AI into its services. We had expected this would boost the company’s profile and add value to the growth-focused company.

But in the last year and a half, the company’s stock price has not reflected growth at all. The price is around the same it was when we first entered. While there’s been some swings higher and lower, there has been no meaningful returns.

While we like long-term plays, we do need to see some sign of the ability to at least deliver sizeable, short-term performance to boost the stock higher. We’ve not got that at all from Dot Digital. As such, we think this capital would be better allocated to bigger more explosive investment opportunities in areas like AI, nuclear, AI infrastructure/bitcoin miners, quantum computing and high-tech energy solutions.

Action to take: SELL Dot Digital (LON:DOTD)

Aura Energy (LON: AURA)

Admittedly, Aura’s stock price has not accurately reflected the company’s prospects with its Tiris project and, of course, the huge potential of Häggån.

The stock is sitting in a sizeable loss for us at the moment. However, that’s more a by-product of limited capital and volumes for junior miners in both Australia and the UK where the company is dual listed.

We expect the resources cycle to pivot and lead to greater interest, investment and capital flow in 2025 and into 2026. Furthermore, the nuclear story is only getting stronger, and the demand for uranium we only see as a long-term bull market. This means that while Aura isn’t where we want it to be, with news recently like the upgrade resource of Tiris, we firmly believe the company is close to a serious run-up with mining and resources markets getting hotter in 2025.

We stick with the position and have conviction the stock can turn around its performance.

Arm Holdings (NASDAQ: ARM)

Arm has just stepped into the courtroom with Qualcomm.

The outcome here is uncertain. If Qualcomm wins, then other companies will be able to effectively have a looser rein as to what they can do with Arm designs. If Arm wins, then the industry is kept beholden to its designs and the company’s IP is kept tighter and closer to home.

That said, whoever loses is likely to appeal, so this could drag on for a while. It is significant, and the outcome may cause us to reconsider the position dependent on exactly what the judge lays out.

Still, Arm is a long-term critical supplier to the world’s AI rollout. This case is frustrating and a handbrake on the company’s stock price, but with clarity from it, we do believe Arm can move forward, whatever the outcome.

We’ll keep an eye on things. If anything needs to change, it will. But if not, it still forms one of the most important companies in AI and certainly one of the most important companies in the UK.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF has fallen by over the month to trade last at around £6.04 at the time of writing, putting it around 32% below our £8.96 entry price.

The ETF allows investors exposure to the lithium and battery sectors.

It seeks to provide returns similar to those of the Solactive Global Lithium Index by holding shares in a broadly diversified cross-section of industries that range from lithium miners to battery producers, all the way to the producers of electric vehicles.

By owning mining, refinery and battery production companies in the fund, Global X has its fingers in multiple parts of the lithium industry.

The lithium hydroxide price has slid nearly 90% since touching a peak of $85 per kilogram in December 2022, after soaring by more than sevenfold during the previous 18 months.

So far, around a dozen lithium producers have temporarily shut loss-making mines, trimmed output or delayed expansions, which should start to support prices.

The ETF remains a HOLD in the portfolio while the market finds its feet.

Central Asia Metals (AIM: CAML)

Central Asia Metals (AIM: CAML) is 151.40p at the time of writing, leaving it around 45% underwater in the model portfolio.

The company operates Kazakhstan’s Kounrad copper mine and the Sasa lead-zinc asset in North Macedonia. The Kounrad mine, in particular, remains one of the lowest-cost copper producers globally, with C1 cash costs of $0.78 per pound (C1 costs being the standard metric in copper mining to denote the basic cash costs of running a mining operation).

In the absence of news, the stock has weakened in line with falling copper prices that have fallen sharply in the second half of 2024 amid intensifying demand worries, a downtrend that could continue if core economic data from the US and China continues to underwhelm.

However, the future outlook appears promising, especially given forecasts of rising demand for copper.

Global copper consumption is expected to climb by 30% between 2023 and 2035, according to McKinsey & Company. Meanwhile, supply is likely to fall short due to delays in new projects and declining production from existing mines.

But with the stock still showing short-term volatility, let’s keep the stock as a HOLD for now.

Volt Lithium (TSXV: VLT)

Volt Lithium, which entered the Southbank Growth Advantage portfolio on 2 August at C$0.37, has fallen, trading last at C$0.28, putting it 26% down in our model portfolio.

The company has developed proprietary direct lithium extraction (DLE) technology aimed at extracting lithium from North American oilfield brines, contributing to a secure critical minerals supply chain for the region.

On 10 December, it announced a field study agreement with Wellspring Hydro to test its DLE technology in the Bakken Formation, North Dakota. Supported by an initial $450,000 grant from the State of North Dakota, this field study seeks to validate the viability of extracting lithium from oilfield brine in one of the most significant oil-producing regions in the US.

Volt expects an additional $50,000 in funding from the grant upon completion of the study and plans to apply for up to $2 million in additional funding in early 2025 – meaning there’s up to $2.5 million on the table in grants from North Dakota.

This is major. Most companies struggle for years to get any grant and this one is very meaningful and a significant percentage of the cost of building a DLE plant.

Partnering with an oilfield water solutions company also seems an excellent match for Volt. However, what’s also significant is that the company now has a foot in the two largest oilfields in the US: its existing field operation in the Permian Basin, which it operates with an unnamed partner, and a second field unit in the Bakken formation in North Dakota.

Although the Bakken produces smaller volumes of brine than the Permian, lithium concentration is around 50% higher in the latter formation, meaning more lithium is produced for every barrel of brine processed.

But that wasn’t it.

On 18 December, Volt announced it had scaled up its US field operations to process over 2,500 barrels per day (equivalent to 480,000 litres per day) from the Permian Basin in Texas. It also said it has now completed over 200 operational runs in the field since commencing operations and achieving first lithium production in September 2024.

The current field unit is so-called generation 4, but the company said it is also set to commission a “larger generation 5 field unit” during January 2025 that will process up to 10,000 barrels per day (1.9 million litres per day).

Certainly, transitioning from its generation-4 to a generation-5 unit (larger 4x) that processes 10,000 barrels per day so soon is very impressive.

We like the Volt for many reasons, not least of which the fact it keeps delivering on time, meeting every milestone it sets. Remember, this is a small Canadian company bringing the world a revolutionary DLE tech to change the way lithium is extracted.

Although the share price remains under pressure from funds that took the previous financing (by selling the shares and keeping the free warrants), the company is now significantly de-risked with financing out of the way. The path is now clear for the large commercial unit to be built by mid-2025 when lithium extraction will start in full force.

Soon enough, the oil industry will recognise Volt as the first in the world to get the DLE unit working in the field, and all at a fraction of the Capex of its peers.

The stock remains a BUY under its buy limit of C$0.50.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation, the world’s largest gold miner, is trading around $37.02. The stock is now 43% below our $65.39 entry point.

Newmont has sold its Cripple Creek & Victor Gold Mine in Colorado for up to $275 million to another Denver-headquartered company, SSR Mining Inc.

Newmont expects the transaction to close in the first quarter of 2025, subject to conditions being met, according to a news release.

Newmont announced at a 2023 year-end earnings call to investors last February that it planned to sell six mines in total, including the Cripple Creek & Victor Gold Mine.

Divestitures and other sales Newmont announced this year are expected to produce total gross proceeds up to $3.9 billion, according to Newmont. The company held $8.55 billion of debt at the end of September, up from $5.58 billion a year ago, but showing net debt of nearly $5.5 billion after factoring in cash.

Strong gold prices, which have hovered near record levels in recent months, continue to add a favourable backdrop. Newmont also anticipates its strongest production volumes for the year in the final quarter, aligning with its strategic efforts to optimise its asset base.

Newmont remains a BUY under $100.

Prysmian Group (IL: 0NUX)

Prysmian Group remains around 27% up in the model portfolio to around €61.13.

It has announced two big deals over the last week.

Firstly, on 13 December, Prysmian said it had signed a capacity reservation agreement with Transpower New Zealand, the country’s national grid operator, worth around €250 million.

Under the agreement, the Italian cable maker will install a new submarine interconnection across the Cook Strait with an overall capacity of up to 1,400 MW, replacing existing infrastructure nearing the end of its operational life.

This will provide “significant benefits to the country, ensuring reliable and cost-effective electricity supply, while supporting the increasing electricity demand in New Zealand,” Prysmian said in a statement.

The contract is expected to be finalised in the first quarter of 2026 with a notice to proceed expected by June of that year, and commissioning planned in 2031, the statement added.

Prysmian noted that two-way power links are crucial for New Zealand, especially when hydroelectric generation in the south suffers due to dry weather conditions, as in 2024. The island country has no power connections with other countries, it noted.

Secondly, on 17 December, Prysmian announced it had signed a framework agreement with RTE, the French transmission system operator, for cables to connect two offshore wind farms.

The agreement spans the design, supply, installation and commissioning of submarine cable links for the Fos and Narbonnaise offshore wind farms, covering both the submarine and onshore parts.

These two contracts, expected to be finalised in 2026-2027, have a combined potential value of approximately €700 million.

Delivery and commissioning are ten scheduled for the period between 2031 and 2032.

The Fos Project, to be located along the Provence-Alpes-Cote d’Azur coast, will require some 300 km of cables, while the Narbonnaise Project, on the coast of Occitanie, will need 340 km of cables. The projects will provide individually a potential capacity of 750 MW.

The stock remains a buy under its buy limit of €60.

SilverCrest Metals Inc (TSX: SIL)

SilverCrest Metals, recommended in the May issue of Southbank Growth Advantage at C$12.55, has traded flat over the last month to last trade at C$13.14, leaving it 4% up.

The Canadian silver miner has agreed to be acquired by Coeur Mining in an all-share deal valued at US$1.7 billion. This is set to close in late Q1 2025.

The stock remains a BUY up to C$16.

Ashtead Technology Holdings PLC (AIM: AT)

Ashtead Technology Holdings was last seen at around 517p,, leaving it 12% below our recent entry point of 590p.

Ashtead has a history supplying subsea services to the oil and gas sector but has diversified into the fast-growing offshore wind market, specialising in renting out equipment crucial for the operations of installations throughout their lifecycle.

The company’s technology offerings include surveying equipment, sensors, and robotics essential for installation, operation, maintenance and decommissioning of assets.

A flurry of merge and aquisition deals has helped Ashtead see a surge in revenue in its 2023 full-year results, with revenue growing 51% to £110.5 million compared to £73.1 million in 2022.

The stock remains a buy under 700p.

AirJoule Technologies (NASDAQ: AIRJ)

AirJoule Technologies, recommended at $7.92 in the November issue of Southbank Growth Advantage, was last seen at $9.43, putting it nearly 19% up in the model portfolio.

The firm’s transformative climate technology is an energy-efficient system that both dehumidifies air and also harvests water from both humid and arid atmospheres to produce pure distilled water.

Currently, the tech remains in the prototype and testing phase, with preproduction units being assembled for evaluation by potential customers and an impressive list of partners.

The company is working towards delivering its first commercial-scale preproduction units in mid-2025, and entering full commercialisation the year after.

The stock remains a buy below $11.

Inside the lives of James and Sam

James:

It’s finally happening.

Three years and four months after we started renovating our house, I can now finally say we are ready to move in.

It’s been one hell of a journey, with emphasis on the word “hell”.

As many of you will know, we originally contracted a supremely dodgy design and build firm to refurbish our house in south-west London, which we bought in spring 2021 and have still never slept a night in.

We were told the job would only take six-to-nine months – that was only the first of many subsequent lies and other forms of deception that have come our way since.

Although the fight against those builders is still ongoing, so far encompassing three different sets of solicitors, one barrister and (so far) five other similarly affected families, the wholly respectable set of new contractors we employed earlier this year are now rushing to get the house ready for us to move in next week.

OK, the house still won’t be entirely finished, though that matters little at this stage. We just want to get in. Deborah, my partner, put her foot down and told everyone who mattered that, come what may, we would be in by Christmas – so that’s what we’re doing.

Even though we’ll be surrounded by boxes, it’s exciting to think we’ll wake up on Christmas Day in our home.

It will certainly make daily life less challenging next year, all living under one roof during the week and near our kids’ schools.

So, yes, it should be a very happy Christmas for the Allen household.

Whatever life has thrown at you this year, I sincerely wish you and your families a happy Christmas too. Have a great one.

I’ll continue to keep an eye on the portfolio and will alert you if anything urgent pops up, but for now, that’s all from me this year.

Take care and see you in 2025.

Sam:

As it’s December, there’s only been one thing on the minds of the people in the Volkering household…

Christmas!

However, this is our first Christmas as a family in Australia, and I will openly say it now, Christmas in Australia sucks compared to the UK.

The UK does Christmas better than anyone. It makes us quite homesick when we’re at the beach and it’s 28 degrees, when back in the UK it’s cold, snowy and super festive.

OK, it’s not all bad here, but we do miss a British Christmas.

Still, that doesn’t mean we don’t go full throttle into the festive spirit. The advent calendars are out, the Christmas tree is up, decorations and lights abound and the food and grog ordering for Christmas lunches and dinners is extraordinary.

My wine bill for the month isn’t helped by the fact my brother is a sommelier (not his real job, just his hobby) but it does mean the next week or so will be filled with the good stuff, quite literally.

With a large family out here, it does mean a lot of present buying and trying to figure out which cousin and kid gets what, what our own kids need to write to Santa to ask for and what they can ask us for.

Thankfully when my boys emailed Santa their lists (he has an email address this year and even replies personally to them) he made sure he was able to get everything they asked for… even the “two margarita pizzas” my three-year-old has asked jolly St. Nick for this year, along with other things.

But in the process of getting ourselves and everything ready for Christmas this year, I spent a bit of time browsing the pages of various sites trying to find that perfect little something for everyone in the family.

One of my go-to places every year around this time is The Verge. That’s because it almost always has great lists of things to buy for the tech nerd (like me) and also great fun ideas for others.

Although we’re close to Christmas, there’s still time to get some of these things if you’ve not completely finished off your shopping – The Verge Holiday Gift Guide.

Anyway, it is Christmas, and here at Southbank I’ll be taking a couple of weeks with the family for the summer holidays here. I’ll be back early January, when we’ll have another edition of Southbank Growth Advantage for you.

If anything urgent happens to the stocks in our portfolio in the meantime, we will still get anything out that needs to be sent. That’s rare based on experience, but it will be done if needed.

That said, it’s most likely you’ll hear from us again in 2025.

So Merry Christmas, Happy New Year and see you again in 2025.

Crypto Corner

Sam:

This is your incoming president of the United States of America.

The ”Gold Paper” is the explainer document (like a whitepaper) for World Liberty Financial – a Trump-backed crypto project.

In the words of the Gold Paper,

Inspired by the vision of Donald J. Trump, World Liberty Financial, Inc. (“World Liberty Financial” or “WLF”) is pioneering a new era of Decentralized Finance (DeFi). WLF’s mission is to democratize access to financial opportunities while fortifying the global status of the US Dollar.

It goes on to talk about putting power back into the hand of people and away from powerful financial institutions, as well as yield generation and other DeFi projects it aims to integrate.

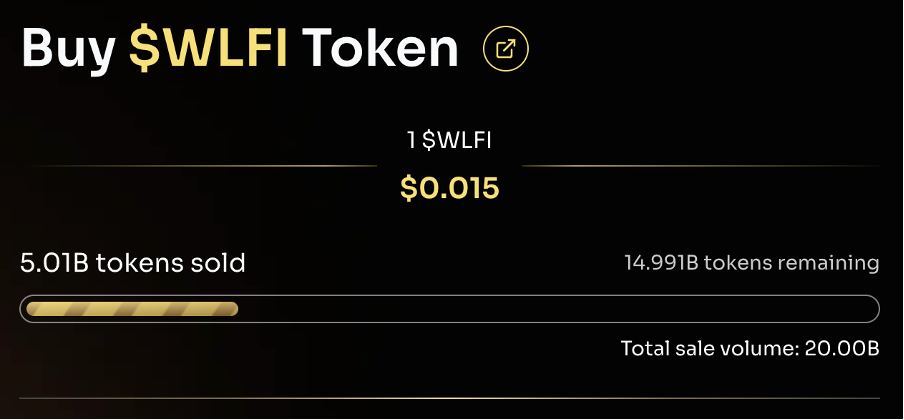

Then, of course, there’s the $WLFI governance token, which is currently in the middle of a pre-sale and isn’t going so well…

Nonetheless, this is a heavily Trump-backed decintralised finance (DeFi) project. Its website even shows the line-up of Trumps and their involvement:

It is fascinating that this is the next president.

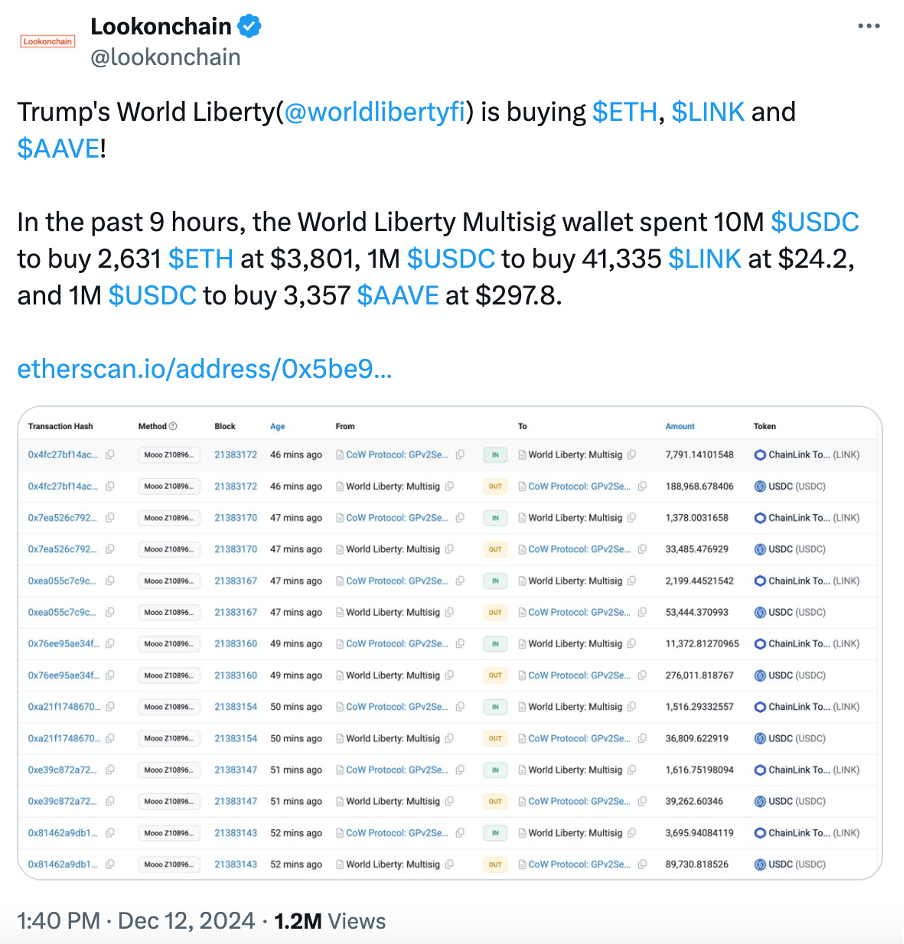

And what’s even more fascinating is that World Liberty has started to build a war chest of other crypto.

Just a couple of weeks ago, World Liberty’s wallets started buying up large amounts of DeFi crypto, like LINK and AAVE.

Source: Lookonchain via X.com

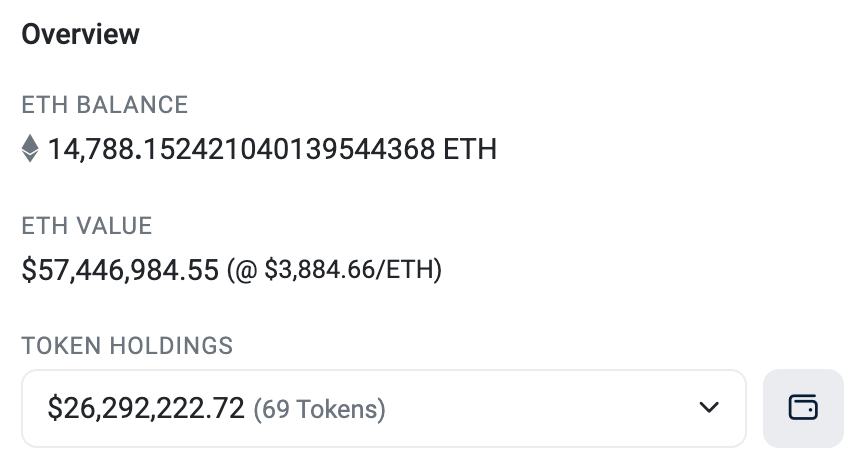

If you head to the actual wallet address you can see its total crypto holdings. This includes $57.4 million in ETH, $10.9 million in Coinbase Bitcoin, $6.3 million in USDC, $3.6 million in USDT, $2.2 million in AAVE and $2.1 million in LINK as the other biggest holdings.

The point of this information isn’t really anything to do with World Liberty.

The token sale thing? Honesty, I think this may very well end up in the realms of Trump’s NFTs, watches, sneakers and all the other stuff he’s tried to flog to people in the last few years.

But with all this going on, you have to keep coming back to this being the incoming president of the United States of America.

The world’s largest economy, most powerful military and soon-to-be “leader” in AI and crypto. Or at least that’s what Trump has been promising.

This World Liberty stuff is a sideshow. But it is categorical proof that Trump intends to be long bitcoin and crypto during his term. I get the feeling he’s going to lean heavily into the open regulation and growth of crypto in the US. That’s so he can come out of the presidency richer than ever – setting up Eric, Don Junior and Barron with untold wealth so that if any one of them decided to run for president in the future, they probably wouldn’t even need to look for donors.

For what it’s worth, my bet is if there’s going to be another Trump in the White House after Donald, it’ll be Barron.

Anyway, with just a few weeks to go until Trump is inaugurated and he can get to work on all the radical changes he’s been promising, it does feel like there’s simply no other major catalyst on the near horizon that’s as significant to the direction of the industry than that.

Thanks to open knowledge of his pro-bitcoin and pro-crypto stance, and the acceptance that a US strategic bitcoin reserve is a very high possibility inside his first 100 days, countries around the world are now starting to have conversations about following suit.

The European Parliament is discussing it. The Russians are said to be proceeding with it. You bet China is doing something (if it hasn’t already) and we know smaller nations like El Salvador and Bhutan, as well as states within countries, are proceeding with using and adding bitcoin to their treasuries.

In short, I still think everyone should have some exposure to bitcoin. In areas where you can’t get it directly, get it by proxy. That’s why we’ve recommended MicroStrategy today, and why we continue to have a holding of bitcoin miners in our portfolio.

(It’s also why it’s been a focus over at my other service Predictive Edge. In fact, I’ve got my eye on three under-the-radar crypto stocks that I believe could surge because of what we’ve discussing here. For more on that, just pop over here.)

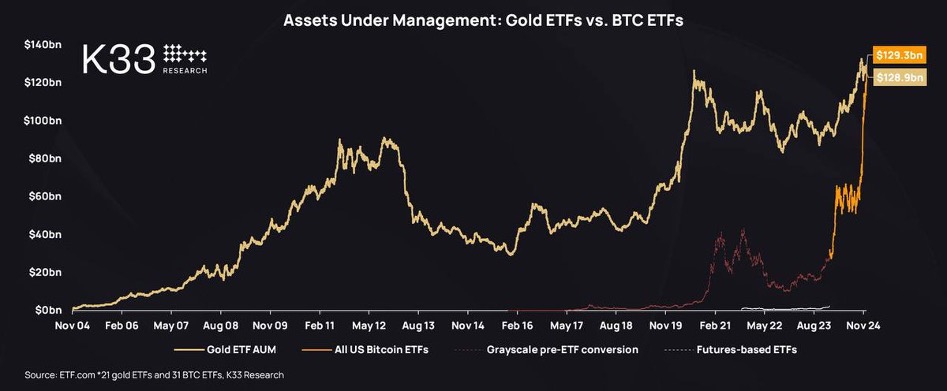

Finally, while we’re on the subject of widespread mass adoption and acceptance of bitcoin through all parts of the global financial system, let’s not forget how fast a journey this has been.

Remember, the bitcoin spot exchange-traded funds (ETFs) only launched at the start of this year and already they have more assets under management than gold ETFs.

Source: Cointelegraph

As I suggested to a mate, “Imagine being 10-0 up in the 94th minute of 95 mins and you get rolled 10-20.”

Just one more thing…

This is still early days. The train has left the station but it’s still very far from its destination, because when BlackRock is still just trying to get people to understand bitcoin, you know you’re still early.

Source: Bitcoin Magazine, via X.com

What else we’ve been looking at this month

James:

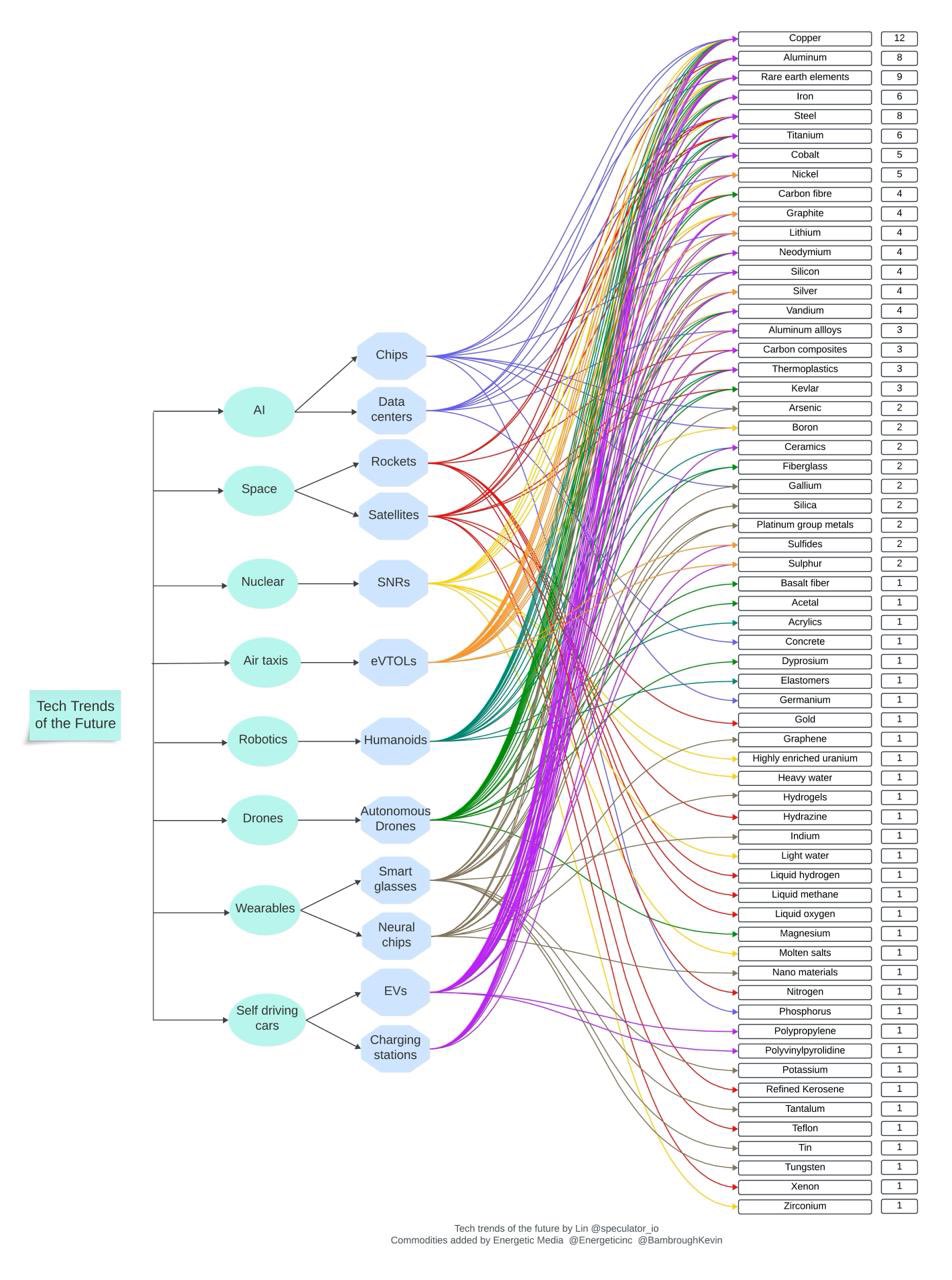

The key commodities underpinning tech’s future

Take a look at the below chart, which highlights some key commodities critical for tech’s future:

Source: Kevin Bambrough, X.com

Drawn up by Kevin Bambrough, a financial expert with over a decade of experience in commodities markets, the chart highlights the materials underpinning future technology.

But you might think it also reveals what you might consider a major oversight: while the technologies themselves have taken huge amounts of both attention and investment, the materials their industries require have been largely ignored.

Indeed, what the chart doesn’t show is that every single element to the right of the chart also requires further inputs for mining, refining and production, as well as vast power inputs. It takes resources to produce resources, after all.

As Bambrough explains, what this means is that, to meet future demand, commodity prices must rise, triggering an unprecedented supercycle. While markets will always chase tech, a real opportunity also lies in resource stocks, which he says are poised for significant revaluation.

According to Bambrough, energy and materials will soon dominate global market valuations once again.

Morgan Stanley survey shows value in renewables

A December survey from Morgan Stanley somewhat challenges the idea that clean tech stocks will struggle during US President-elect Donald Trump’s term.

Reported by ESG Today, the survey found that nearly 80% of 900 institutional investors expect sustainable assets to see gains over the next two years, driven by both fresh investments and general market appreciation.

The report attributes this outlook to the “maturing” of the environmental, social and governance (ESG) category, though that term is somewhat vague.

But what stands out is the forecast of improved performance for renewable energy and clean tech stocks. This may partly reflect a rebound after years of poor performance, as the sector is certainly overdue a recovery.

Dumping fossil fuels slowly, then all at once

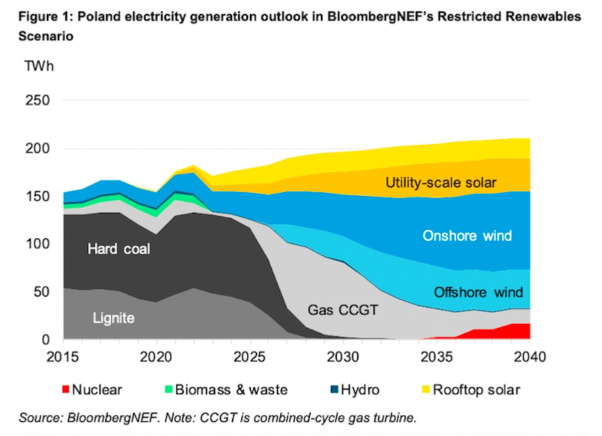

European Union’s most coal-reliant country is now speeding up its energy transition, as this chart by BloombergNEF testifies:

Poland reduced its reliance on coal for electricity from 96% in 1990 to 68% by 2020 – a 30-year transition. But the pace is accelerating.

Poland is set to phase out coal entirely by 2032, with Tauron Polska Energia SA, its second-largest utility, recently pledging to exit coal entirely by 2030.

Phasing out fossil fuels happens gradually – until it doesn’t.

Sam:

12 Days of ChristmAIs

I’ve been following 12 Days of OpenAI every day in December and it’s actually delivering some pretty cool stuff. So far, Day 6 has been my favourite. When you start to see just how quickly AI is advancing with natural conversation language, it makes the next couple of years really exciting as to where we could end up.

Go check it all out, and make sure to keep tabs over the holidays as to what else OpenAI has in store.

Saylor’s laser eyes

I’ve been absorbing a lot of the playbook of Michael Saylor in the last month. Clearly it’s what has led me to this month’s recommendation. But as some supporting evidence for why this came to be, I think it’s worth listening to what he has to say directly – plus something from Eric Trump as well.

x.com/saylor/status/1868704730098372625

youtu.be/pQ7fjpqzUS4?si=oBvwtVmqmJquSnjA

x.com/saylor/status/1866539391184711873

Largely speaking of mice

This is pretty off our usual topics, but I find these sorts of thing highly entertaining and fascinating. How scientists thought, experimented and ran tests in the mid to late 20th century created the foundations of a lot of the world we live in today. Which is why I believe that taking the time to read and understand a lot of work from the 70s helps to formulate my bigger view for our world tomorrow. This work in particular is about mice, but the deeper meaning extends to humanity and the world we live in today. It’s worth a read if you’re into abstract science from the early 1970s.

James Allen and Sam Volkering

Editors, Southbank Growth Advantage