Your February issue of Southbank Growth Advantage

27th February 2025 |

- The accidental discovery that could change the world

- Buy List update

- What we’ve been reading and looking at this month

The accidental discovery that could change the world

In 1987, in the remote village of Bourakébougou, Mali, water drillers were hard at work, attempting to tap into a new water source for the local community.

The arid land had made life tough for the villagers, and fresh water was a precious resource.

As the drill bit cut deeper into the earth, the team noticed something unusual: a faint, almost imperceptible hissing sound coming from the borehole.

At first, they thought little of it – it wasn’t uncommon for pockets of gas to be released during drilling. But then came the moment that changed everything.

Taking a break from the relentless heat, one of the workers casually struck a match to light his cigarette. In an instant, a whoosh of flame erupted from the well, sending a terrifying column of fire into the sky.

The men recoiled, stunned.

The fire raged on, refusing to die out.

It took a fire crew weeks to snuff out the flames and cap the well.

Spooked by the incident, the villagers shunned the site, and for two decades, the borehole remained an abandoned curiosity – until 2007, when a wealthy Malian businessman and politician named Aliou Diallo acquired the rights to prospect in the region surrounding Bourakébougou.

Diallo, the chairman of Petroma, an oil and gas company, suspected there was more to the strange borehole than met the eye.

In 2012, he funded tests on the old water well. The results were staggering.

The borehole was releasing gas composed of 98% pure hydrogen – a naturally occurring resource that had long been dismissed as impossible to find in large underground accumulations.

At the time, the prevailing wisdom among scientists and energy experts was that hydrogen, the most abundant element in the universe, simply didn’t exist in large, accessible pockets beneath the Earth’s surface.

If it did, it would quickly escape into the atmosphere, never forming the kinds of underground reservoirs that have made oil and natural gas so valuable.

But the Bourakébougou discovery turned that belief on its head.

A well was drilled, and the hydrogen kept flowing. The villagers even managed to pipe some of it into a generator, producing clean electricity decades before “green energy” became a global buzzword.

For years, the discovery remained an anomaly, a strange but largely overlooked quirk of geology.

However, as the world searched for clean energy alternatives, scientists began revisiting the event in Mali.

What if Bourakébougou wasn’t a fluke? What if hydrogen really was stored underground in vast quantities – waiting to be tapped like oil and gas had been for over a century?

Fast forward to today, and the world is waking up to what could be the biggest energy revolution since the discovery of oil: natural hydrogen.

Also known as geological, white or even “gold” hydrogen, this resource is poised to transform the energy landscape.

Experts predict that natural hydrogen could be abundant, cheap and clean. The US Geological Survey estimates that up to 10 quadrillion tonnes of natural hydrogen could be stored underground worldwide, a staggering figure that dwarfs our current hydrogen production from fossil fuels and electrolysis.

And just like that, we might be on the verge of a new gold rush.

Why natural hydrogen could be a game-changer

If you’ve been following the clean energy debate, you know that hydrogen is often hailed as the fuel of the future. It’s lightweight, energy-dense, and when burned or used in fuel cells, it produces nothing but water vapour.

Hydrogen is a fuel that could replace hard-to-electrify molecules combusted by factories and commercial ships and vehicles.

Currently, around 90% of the hydrogen produced worldwide is used as a raw material in the chemical industry, in the manufacture of fertilisers (ammonia), solvents and fuels (methanol), and as a reagent in the refining of crude oil.

But this percentage could well change, as producers of steel, cement, glass and metals consider using hydrogen to decarbonise their activities. Hydrogen could replace fossil fuels when electrification is not possible or too costly.

The problem? Hydrogen production today is either dirty or expensive – or both.

- Grey hydrogen: the dominant form today, made from natural gas using steam methane reforming (SMR), emits large amounts of CO2.

- Blue hydrogen: essentially grey hydrogen with carbon capture technology to reduce emissions – but still dependent on fossil fuels.

- Green hydrogen: produced by splitting water using renewable electricity, but incredibly costly due to high energy input and infrastructure challenges.

Now, enter natural hydrogen.

Unlike these methods, it requires no energy-intensive production process – it’s already there, underground, waiting to be tapped.

Extracting it is as simple as drilling a well, just like we’ve done for oil and gas for over a century. That makes it not only significantly cheaper than green hydrogen but also far less environmentally damaging than grey or blue hydrogen.

Unlike fossil fuel stores, which take millions of years to form, natural hydrogen is continuously replenished.

And unlike hydrogen produced from natural gas or wind or solar power via electrolysis – “grey” and “green” hydrogen, respectively – its natural counterpart requires no water and little energy to extract while taking up very little land.

These advantages make natural hydrogen a much cheaper resource than green hydrogen, certainly. The cost of natural hydrogen is estimated at €0.50 per kilogram, while green hydrogen costs roughly €5 per kilogram.

Natural hydrogen has the potential to dominate the hydrogen market simply because it is the lowest-cost, lowest-emission hydrogen available.

How much hydrogen are we talking about?

The estimates are jaw-dropping. As previously mentioned, there could be up to 10 quadrillion tonnes of natural hydrogen waiting beneath the Earth’s surface.

That’s vastly more than the 100 million tonnes a year of hydrogen that is currently produced and the 500 million tonnes predicted to be produced annually by 2050.

In fact, it’s enough to supply global energy needs for hundreds of years.

Most natural hydrogen is likely to be found in unreachable locations that are either too deep or too far offshore. However, geologists state that if just 1% was recoverable, that would be enough hydrogen to keep the world going for at least two centuries – even if there was a surge in demand for hydrogen.

Hydrogen experts are beginning to believe we may have seriously underestimated how much natural hydrogen exists.

Recent drilling projects in France, Australia and the US have confirmed that this isn’t just a one-off discovery in Mali, it’s a global phenomenon.

New surveys are revealing that hydrogen seeps are far more common than previously thought, and now, with the right technology and incentives, a major exploration effort is underway.

If even a fraction of the projected reserves turns out to be commercially viable, it could completely disrupt the hydrogen supply chain. This would make hydrogen a mainstream energy source far sooner than expected.

The market potential for natural hydrogen

The discovery of natural hydrogen is still in its early days, but what is clear is that more and more companies are now entering the space. They are all eying up a natural hydrogen industry that could be worth $75 billion industry by 2030.

Unlike traditional hydrogen production, which requires massive capital investments in electrolysers or carbon capture technology, natural hydrogen just requires drilling expertise and infrastructure that already exists from the oil and gas industry.

Little wonder than there were some 40 companies searching for natural hydrogen deposits by the end of 2023, up from just 10 in 2020.

Up until now, the industry has largely been the preserve of small companies, venture capital funds and individuals with deep pockets and an appetite for risk. But major energy companies, once sceptical, are now assessing their options.

Once bigger companies start putting larger amounts of money in, this will undoubtedly accelerate the development of natural hydrogen significantly.

But right now, junior exploration companies offer perhaps the most upside. These are the equivalent of early-stage oil explorers, taking risks on drilling and discovery

After scouring the market extensively, one London-listed company stands out.

You see, while many energy explorers are only just waking up to the opportunity, this company has already struck hydrogen – and potentially lots of it.

Even more interestingly, it wasn’t focused on hydrogen when it made the discovery. It had been mainly drilling for another valuable resource, helium, when it stumbled upon vast, high-purity hydrogen flows in Montana. That fortunate accident has catapulted the company towards the front of the natural hydrogen race.

This isn’t just a speculative land grab either. Early readings suggest it’s sitting on something truly substantial. If these flows prove commercially viable, it could be sitting on one of the most valuable hydrogen discoveries to date.

And it doesn’t stop there.

The company’s helium operations – a crucial element for high-tech industries – are nearing production, adding another layer of potential upside for investors.

So, who is this pioneering hydrogen explorer?

Its name is Helix Exploration PLC (AIM:HEX).

Helix Exploration PLC (AIM:HEX): leading the charge

Helix Exploration started as a helium-focused company but has recently made a game-changing hydrogen discovery at its Ingomar Dome Project in Montana.

The company’s Clink #1 well has reached a depth of 8,030 feet, encountering significant shows of helium and hydrogen across multiple formations, including the Amsden, Charles and Flathead formations.

Notably, the deeper Cambrian strata revealed high-purity hydrogen concentrations peaking at an impressive 10.3%. This discovery positions Ingomar as a potential site for the first large-scale hydrogen production in the US.

CEO Bo Sears called the find “beyond anything we have ever seen”, noting that the hydrogen readings from their well are significantly higher than industry expectations. Although early mud logging has shown concentrations of over 10%, experts say the true undiluted underground concentrations in the ground will be much greater. If this proves commercial, Helix may have one of the most valuable clean hydrogen assets on the planet.

This discovery sets Helix apart from other companies that have been exploring theoretical hydrogen reservoirs. That’s because Helix is one of the only companies with an operational well showing hydrogen production. This puts it at the front of a pack of companies that might be able to commercialise natural hydrogen at scale.

Financially, the implications are enormous.

The global hydrogen market is valued at over $100 billion annually. Helix stands to receive significant incentives from the US government’s tax credit programme for clean hydrogen.

These credits alone could be worth over $183 million. With hydrogen currently selling for approximately $7/kg, potential revenue from its discovery could exceed $427 million annually.

Strategic diversification with helium projects

Beyond hydrogen, Helix’s helium operations serve as a crucial hedge against market shifts. Helium is in high demand across aerospace, healthcare and semiconductors, making it well positioned to capitalise.

The company’s flagship Rudyard Project in Montana spans 6,674 acres, where helium concentrations of up to 1.3% have been confirmed.

Production is set to begin by Q4 2025, with additional wells planned, each expected to generate $4 million in pre-tax cash flow annually.

To fast-track operations, Helix acquired a processing plant for just $500,000, set to launch by early summer 2025.

Independent consultant Aeon estimates the northern dome of the site alone holds 355 million cubic feet of helium, potentially generating $115.2 million in net revenue over 12.5 years. Aeon values these reserves at a net present value (NPV) of $77.9 million with an internal rate of return (IRR) above 1,000%. In-house projections push NPV to $145 million with total revenue reaching $220 million.

CEO Bo Sears confirms the company is fully funded to bring Rudyard online. Early cash flow will support exploration, M&A and self-financed expansion.

Helix plans to drill two more wells in early Q2, taking advantage of lower seasonal costs. Each well costs just $1.2 million to drill, allowing for rapid scaling. The final step before production is securing a membrane system for helium separation.

Rather than locking into fixed contracts, Helix is engaging multiple buyers to optimise pricing. “We’re gathering off-takers now,” says Sears. “I don’t expect any issues with that.”

Beyond Rudyard, Helix holds 52 leases at the Ingomar Dome, with a prospective helium resource of 2.3 billion cubic feet – potentially up to 6.7 billion.

The 16,512-acre site has an estimated NPV of $304 million. The goal? Prove commercial viability at both Rudyard and Ingomar, securing near-term revenue while their hydrogen ventures progress.

Strong financial footing to progress

Helix is moving at an impressive pace, progressing from its April 2024 initial public offering (IPO) – where it raised £7.5 million – to first gas by late 2025. Most peers take two to three years to achieve this, but Helix is on track to do it in just 18 months.

The company remains fully funded for operations, ending the fiscal year (30 September) with £4.96 million in cash and securing an additional £5 million in January 2025.

This capital will support drilling at Rudyard once Clink One is completed, as well as further development of the Ingomar Dome. Helix is targeting helium production in 2025, with positive cash flow expected soon after.

For the year, the company reported a £2.17 million operating loss – typical for a business heavily investing in exploration. But with Rudyard’s wells projected to generate $15 million to $25 million in free cash flow annually, Helix is positioned to self-fund future growth.

The speed of execution has been remarkable. Just ten months post-IPO, Sears and his team have consistently delivered on milestones. Helix’s January 2025 raise of £5 million at 15p per share – 50% above its IPO price – demonstrates strong investor confidence.

The IPO was heavily oversubscribed, and despite having the option to raise more initially, the company’s ability to secure capital at a higher valuation signals strength.

With funding secured and development accelerating, Helix is in a strong position to capitalise on its helium assets while minimising dilution. The foundation is set for a significant re-rating as production nears.

This is extremely high risk

While Helix is making impressive progress, investing in a small-cap natural resource company carries high levels of risk.

From regulatory hurdles to infrastructure challenges and the unpredictable nature of exploration, there are plenty of moving parts.

On top of that, while an exciting concept, natural hydrogen – one of Helix’s big bets – is still an unproven industry. Unlike helium, which already has an established market and extraction methods, natural hydrogen is still a big question mark.

Here’s what investors should keep in mind.

Company risks:

- Small, illiquid share with high volatility

Helix is still a small player, with a market cap of around £24 million. That means its shares don’t trade in high volumes, making liquidity an issue. If you need to exit your position quickly, you might struggle to find a buyer without taking a hit on price.

Small-cap stocks also tend to be more sensitive to market sentiment. Good news can send shares soaring, but any bumps in the road can trigger sharp drops.

- Regulatory and permitting challenges

The natural resources sector comes with a lot of red tape. Helix needs to secure drilling permits, environmental approvals and operational licences, and these can take time. Changes in regulation – especially around environmental policies – could delay projects or drive up costs.

Montana, where Helix operates, is generally resource-friendly, but that’s never a guarantee. The regulatory landscape can shift. That could impact Helix’s ability to get projects off the ground as quickly as planned.

- Infrastructure and development risks

Finding helium or hydrogen is just step one – the real challenge is getting it out of the ground, processed and delivered to market. Helix has taken a smart step by acquiring a helium processing plant, but getting it up and running smoothly is another story.

Power supply, pipeline connections and transportation logistics all need to fall into place. If infrastructure delays crop up, it could slow down production and revenue generation.

- Exploration and production uncertainty

Even with promising early results, exploration is never a sure thing. Helix has confirmed helium at Rudyard, but further drilling needs to prove consistent, commercially viable production. Unexpected geological issues could make extraction trickier than expected.

Plus, even if reserves are solid, flow rates need to hold up over time. Investors banking on a quick ramp-up to cash flow should keep in mind that the subsurface doesn’t always cooperate.

Natural hydrogen risks:

- Still much to learn

Scientists are still figuring out how natural hydrogen forms deep underground, how it moves and how best to extract it. If the deposits turn out to be more scattered than expected, large-scale commercial production could take longer – or never fully materialise. This isn’t oil or natural gas, where the playbook is well understood – natural hydrogen is still a bit of a mystery.

- Potential for high extraction costs

Even if natural hydrogen is abundant, getting it out of the ground cheaply is another matter. If significant reserves require deep drilling, production costs could climb quickly, making the economics less attractive. What looks like a game-changer today could end up being a much more expensive process than expected.

- Location and transport challenges

One major hurdle for hydrogen is that deposits might not be anywhere near where the demand is. Unlike helium, which has an existing transport infrastructure, hydrogen logistics are still in development. Storage and transportation costs could be a real challenge, potentially making some projects too costly to be viable.

A ground-floor opportunity in a game-changing sector

Investing in Helix is not for the faint-hearted, but for those who can stomach the volatility, the upside could be enormous. This is a company moving at lightning speed in the helium space while positioning itself as an early leader in natural hydrogen – an industry that has the potential to redefine global energy markets.

Helix isn’t just drilling holes and hoping for the best. It’s backed by a sharp management team, fully funded for its next phase and already making moves to secure production and sales channels.

The helium side alone has the potential to generate substantial near-term cash flow, providing a financial backbone for what could be its real prize: unlocking its natural hydrogen resource.

If its discoveries prove commercially viable, the company could be sitting on a resource that helps redefine global energy markets. While there are still major scientific and logistical questions to answer, those who get in early – before the market fully wakes up – stand to benefit the most if the sector takes off.

Timing matters. The stock is still small and relatively under the radar, but Helix is cashed up, moving quickly and has a steady stream of news flow ahead.

With leadership that knows how to execute and a strategy that bypasses industry middlemen, the company is maximising its profitability potential.

Of course, every new energy breakthrough starts with a leap of faith. Natural hydrogen was little more than a scientific curiosity until a lucky cigarette in Mali ignited a flame that burned for decades.

Now, the industry is racing to figure out how to tap this vast, untapped resource efficiently. Helix is one of the few companies at the forefront of this push.

For investors with an appetite for speculative, high-reward opportunities, Helix offers a rare chance to get in early on a potentially transformative industry. Natural hydrogen isn’t just a futuristic idea – it’s a growing reality. And Helix could be one of the names that helps bring it into the mainstream.

Action to take: buy Helix Exploration PLC

Ticker: AIM:HEX

ISIN: GB00BPK66X70

Market cap: £23.3m

52-week high/low: 29p/10.05p

Buy up to: 23p

Source: Hargreaves Lansdown

Buy List update

Sprott Uranium Miners ETF (LSE:URNM)

This exchange-traded fund (ETF) has a diverse array of uranium miners from Cameco through to NexGen Energy, Paladin, even Yellow Cake. But we’ve now been holding onto this ETF for the better part of two and half years and it’s total return so far is just 11%.

ETFs can provide diverse exposure to a particular theme. But they can also wash away potential gains from overdiversification.

By all means, uranium, nuclear and the demand for both is only heading higher. But it’s just not reflected in the ETF. My view is that it’s so diversified that we’re never going to get a meaningful return, which we could get from direct nuclear energy investments.

As such, while it’s still on an 11% gain for us, let’s take the small profit, exit and look to put that capital to use in more explosive opportunities.

Action to take: SELL Sprott Uranium Miners ETF (LSE:URNM)

Recursion Pharma (NASDAQ:RXRX) (formerly Exscientia)

Our Exscientia recommendation merged into Recursion Pharmaceuticals in 2024. Since then the Recursion stock has been going strongly. This is no doubt in part to the investment of Nvidia in the company.

In Nvidia’s most recent 13F filing (the report that shows what it’s invested in) the company still had its Recursion holdings, which was good news. But it was a 13F filing form Softbank that saw Recursion’s stock price pop higher, disclosing a holding in the company.

This saw the stock price top $12 briefly. But in the last week, with a selloff in tech and anything AI related, the stock price is back around $8.60. That said, while we certainly want to ride the waves as and when they come like this, we want to minimise downside for this play.

A perfect example of what can happen when mega-cap companies are invested and then sell the stock can be seen with the stock price of SoundHound AI.

The stock halved in price after Nvidia disclosed in the 13F that it no longer held SoundHound. We want to avoid such a situation should Nvidia or Softbank publish their next 13F and it doesn’t show Recursion on the list.

That would send the stock heavily lower.

As such, we’re not exiting the stock, but we are putting a stop exit on it at the adjusted entry price of $7.28. If the stock price hits $7.28 and under, exit the position for a 0% outcome.

Ideally it’s upwards from here, the selloff in tech and AI is done and its profits for this play. But to protect our backside in the event it all goes belly-up, put a stop exit at $7.28 for Recursion Pharmaceuticals (NASDAQ:RXRX).

Global X Lithium & Battery Tech UCITS ETF (LON:LITG)

The Global X Lithium & Battery Tech UCITS ETF is holding steady at around £6 – still about 33% below our £8.96 entry price.

This ETF gives investors broad exposure to the lithium and battery sector, tracking the Solactive Global Lithium Index. It holds a mix of lithium miners, battery producers and EV manufacturers, covering multiple stages of the lithium supply chain.

If you’ve been following lithium prices, you’ll know they’ve been on a wild ride. Back in December 2022, lithium hit a staggering $80,000 per tonne, only to crash to $13,000 by January 2024.

The drop was largely due to an oversupply problem. New lithium projects flooded the market, adding to already high inventory levels, while demand didn’t quite match up to earlier forecasts. As prices fell, mining projects were shelved and the market began adjusting to shifting priorities from both the public and private sectors.

But there are signs that the worst may be behind us. Citibank analyst Kate McCutcheon believes the lithium market has found its bottom. She points to expected production growth of 30% to 50% at Contemporary Amperex Technology, the world’s largest battery manufacturer, and an even larger 50% to 100% increase at BYD, the Chinese EV maker backed by Warren Buffett’s Berkshire Hathaway.

She also highlights a strong battery manufacturing order book in the last three months of 2024, which should keep momentum going into early 2025. Another bullish indicator is that major Chinese manufacturers appear to be running full production schedules during the Chinese New Year period, potentially as a hedge against the risk of new Trump-era tariffs.

Although the market won’t recover in a straight line, long-term demand for lithium remains strong.

Statista forecasts global demand to rise from 292,000 metric tonnes in 2020 to 2.5 million by 2030. That’s a massive jump. While there will undoubtedly be bumps along the way, the overall trajectory seems clear.

There are already signs of renewed activity. In the week leading up to 21 February, bidding activity in China surged after a period of stagnation in late 2024 and early 2025, according to S&P Global.

For now, the ETF remains a HOLD while the market continues to find its footing.

SilverCrest Metals Inc (TSX:SIL)/Couer Mining Inc (NYSE:CDE)

SilverCrest Metals made its debut in the May issue of Southbank Growth Advantage at C$12.55.

Last October, the Canadian miner struck a deal to be acquired by Coeur Mining in an all-share transaction valued at a cool US$1.7 billion.

And after some anticipation, the deal officially wrapped up on 14 February 2025, with SilverCrest trading at C$15.01.

So, what does that mean? Under the agreement, Coeur acquired all of SilverCrest’s outstanding common shares. In exchange, SilverCrest shareholders received 1.6022 Coeur common shares for every SilverCrest share they held.

Now that the dust has settled, here’s how things shake out: SilverCrest shareholders now own about 37% of the combined company, while Coeur shareholders hold the remaining 63%.

Coeur operates in several key locations, including Mexico, Nevada, Alaska and South Dakota. On the other hand, SilverCrest’s flagship asset, the Las Chispas mine in Sonora, Mexico, is one of the highest-grade, lowest-cost silver operations around.

In fact, in 2023, its first full year of production, the mine churned out over 10.25 million silver-equivalent ounces, all at a very low cash cost of just $7.73 per ounce.

With the addition of Las Chispas, Coeur now becomes a global silver powerhouse, producing 21 million ounces of silver and 432,000 ounces of gold annually.

Together, the combined company will run five mines in North America, with three – Rochester in Nevada, Palmarejo in Mexico, and Las Chispas – being top-tier silver producers.

As we mentioned when the deal was first announced, this acquisition makes a lot of sense.

Remember, SilverCrest had a pipeline issue – as a single-asset company, its mine life was limited, with Las Chispas expected to last just eight more years. Meanwhile, Coeur faced a cost issue – it had relatively higher costs. But this merger solves both problems.

The strong cash flow from Las Chispas will give Coeur the financial muscle it needs to ramp up its aggressive exploration efforts over the next few years. This includes advancing SilverTip, its exploration project in British Columbia, to the next stage.

To sum it up: the new, combined company is set to be a silver mining giant – bigger, stronger and well-positioned to thrive as sentiment in the sector continues to improve.

A key point behind this deal is that miners are scrambling to secure reserves, driven by soaring demand for silver and an ever-growing supply gap.

So, now that the deal is done, your SilverCrest shares should have been converted into Coeur shares.

As a result, Coeur Mining will now appear in the model portfolio with an adjusted entry price of US$5.72, based on the terms of the deal. The buy limit has been updated to US$7.

Central Asia Metals (AIM:CAML)

Central Asia Metals has edged up around 3% over the past month, sitting at roughly 158p. That still leaves it about 43% underwater in the model portfolio. However, recent moves in the copper market could provide some much-needed support.

The company runs two key operations: the Kounrad copper mine in Kazakhstan and the Sasa lead-zinc mine in North Macedonia. Kounrad, in particular, remains a standout, ranking among the world’s lowest-cost copper producers with C1 cash costs of just $0.78 per pound.

While there hasn’t been much company-specific news driving the stock, it has found support in the broader copper market.

President Donald Trump has directed the US Commerce Department to investigate potential import tariffs on all forms of copper, a move that has traders rethinking global supply chains. Copper futures on the Comex in New York jumped as much as 4.9% in response before giving back some of those gains.

This latest tariff talk follows Trump’s earlier decision to impose a 25% tariff on steel and aluminium imports starting 12 March. The copper investigation falls under Section 232 of the Trade Expansion Act, which allows the president to impose trade restrictions on national security grounds.

Trump took to social media to argue that the “Great American Copper Industry has been decimated by global actors attacking our domestic production.” The Commerce Department now has up to 270 days to investigate and report back.

With copper prices reacting to these developments, Central Asia Metals may get some tailwinds. For now, we’re keeping the stock as a HOLD.

Volt Lithium (TSXV:VLT)

Volt Lithium, which joined the Southbank Growth Advantage last August at C$0.37, has seen a 3% gain over the past month, last trading at C$0.33. While still down 11% in our model portfolio, the stock has been battling through some warrant pressure, which now seems to be in the rearview mirror.

The company has developed proprietary direct lithium extraction (DLE) technology designed to extract lithium from North American oilfield brines. This innovation is crucial for securing a stable domestic supply of critical minerals.

Big news from Volt: the recent successful 24-hour continuous run of its Generation 5 Field Unit in the Permian Basin, Texas, marks a major milestone.

On 12 February, the unit processed 11,573 barrels, surpassing the 10,000 barrels per day (bpd) milestone. Notably, Volt built and deployed its largest DLE system in just four weeks – an impressive feat. Further testing is underway to determine peak throughput capacity. Lithium stockpiling has also begun, setting the stage for future sales.

This tiny microcap has a working DLE system that can be replicated and scaled up. Its partnership provides substantial access to additional brine sources, enabling rapid expansion within the US lithium market. In terms of de-risking, it doesn’t get much better than this.

Volt’s Gen-5 unit is fully modular, meaning scaling up is as simple as adding more units and larger tanks. The first full-scale commercial system will process 100,000 barrels per day, with an expected annual cash flow of around $21 million.

Applying a multiple of 15x, Volt’s valuation could hit approximately US$315 million. And that’s just phase one. If it scales up to a 500,000 bpd unit, the numbers jump to a staggering US$1.57 billion in potential valuation!

Lithium remains a critical mineral for US production. Volt’s position in the Permian Basin – where 19 million barrels of brine are produced daily – puts it in a league of its own. No other company has demonstrated successful DLE operations at scale on this brine.

Despite all this progress, Volt is still flying under the radar. The stock is trading at levels last seen in April 2024, back when it was only running lab tests. Fast forward to today: proof-of-concept is established, a 10,000 bpd DLE unit is running in Texas and the path to a 100,000 bpd commercial system is well underway. You’d like to think investors will catch on sooner rather than later.

Volt remains a BUY under C$0.50, with substantial upside potential as it advances towards large-scale commercialisation this summer.

Newmont Corporation (NYSE:NEM)

Newmont Corporation, the world’s largest gold miner, has climbed 5% over the past month and is now trading at $43.58. While that still puts it 33% below our $65.39 entry point, the company is showing solid momentum, helped by strong earnings and rising gold prices.

Newmont just reported a sharp turnaround in profitability, posting a US$3.35 billion profit for 2024, a big swing from the $2.5 billion loss it booked the previous year. In the December quarter, adjusted net income came in at US$1.40 per share, well above analysts’ expectations of $1.08 per share.

Production remains robust. Following its acquisition of Australia’s Newcrest in 2023, Newmont cemented its position as the world’s top gold miner. It produced 6.8 million gold ounces for the year, along with 1.9 million gold-equivalent ounces from copper, silver, lead and zinc.

It has also benefited from soaring gold prices. The company’s average realised gold price in the December quarter was $2,643 per ounce, up from $2,004 a year ago. With uncertainty surrounding the US presidential election and rising tensions in the Middle East, demand for gold as a safe-haven asset has pushed prices to all-time highs.

On the balance sheet front, Newmont has made progress in reducing debt, cutting it by $1.4 billion over the past year. With strong production, record gold prices and improving financials, the company is well positioned for the months ahead.

Newmont remains a BUY under $100.

Prysmian Group (IL:0NUX)

Prysmian Group remains 25% up in the model portfolio, though it has slipped 8% over the past month to €60.26. Despite this short-term weakness, the company continues to deliver solid results, reinforcing its long-term growth potential.

Italy’s Prysmian expects adjusted core profit to rise by as much as 22% this year. This is helped by the full impact of its $4.2 billion acquisition of Encore Wire in 2024.

Strong cash generation remains a key highlight, with free cash flow for the year reaching €1,011 million – up nearly 40% – and yielding 6.3%. Full-year adjusted EBITDA (earnings before interest, taxes, depreciation and amortisation) climbed 18.4% to €1,927 million, with a healthy margin of 11.3%.

Growth accelerated in the fourth quarter, with organic revenue up 6.9%. Transmission continued to be a standout, delivering a 33.7% surge in revenue and an impressive 15% EBITDA margin. Power grids also posted solid numbers, with organic growth of 7.4% and a 13.5% margin.

Prysmian remains committed to shareholder returns, with a proposed dividend increase of 14.3% to €0.80 per share. Looking ahead to 2025, the company forecasts adjusted EBITDA between €2,250 million and €2,350 million and free cash flow in the range of €950 million to €1,050 million.

Fourth-quarter results were largely in line with expectations, though some investors remain cautious over potential tariff risks in the US.

Despite these concerns, Prysmian continues to execute well and remains a strong long-term play. The stock remains a BUY up to €85.

Ashtead Technology Holdings PLC (AIM:AT)

Ashtead Technology Holdings is trading around 520p, down 10% over the past month and sitting 12% below our recent entry at 590p.

Originally focused on supplying subsea services to the oil and gas sector, Ashtead has successfully expanded into the rapidly growing offshore wind market. The company specialises in renting out high-tech equipment that plays a critical role throughout the lifecycle of offshore installations.

Its technology portfolio includes surveying equipment, sensors and robotics that support installation, operation, maintenance and decommissioning. These tools are essential for ensuring the efficiency and longevity of offshore energy projects.

With no major updates over the past month, the long-term investment case remains intact. The stock is still a buy under 700p.

AirJoule Technologies (NASDAQ:AIRJ)

AirJoule Technologies, first recommended at $7.92 in the November issue of Southbank Growth Advantage, has dipped 3% over the past month to $7.37, leaving it 7% down in the model portfolio.

The company’s proprietary AirJoule technology is designed to efficiently extract water from the atmosphere. Its current prototype, the P5, can produce up to 200 litres of water per day while consuming just 130Wh per litre. With a cooling coefficient of performance (COP) above 10 – far exceeding the typical industry range of 3.0 to 3.5 – AirJoule has already demonstrated a significant technological edge.

Looking ahead, the company is gearing up for the launch of a pre-production unit in 2025, aiming to boost daily output to 360 litres while improving energy efficiency to 60-90Wh per litre. When operating purely as a water harvester, the system is expected to generate up to 1,000 litres per day, marking a major step toward commercial scalability.

Financially, AirJoule is in a solid position, with more cash than debt and liquid assets comfortably covering short-term obligations. The company expects to commercialise its technology by 2026, setting itself up as a key player in the growing market for sustainable water solutions.

With a strong balance sheet and a clear roadmap for innovation, AirJoule remains a compelling opportunity. The stock is still a buy below $11.

Solaria Energía Y Medio Ambiente SA (XMAD:SLR)

Since being recommended in the last issue of Southbank Growth Advantage, Solaria Energía has gained around 6%, showing early momentum as it positions itself at the intersection of two major trends – clean energy and artificial intelligence.

Solaria is a key player in renewable energy, but what makes it particularly exciting right now is its strategic push into the data centre market.

With AI driving an explosion in data processing demand, the energy needs of these facilities are soaring. Solaria is stepping in with a solution that combines its renewable energy expertise with efficient power supply for data centres, creating a compelling opportunity in a fast-growing sector.

Over the past month, the company has secured two major approvals from Red Eléctrica de España, reinforcing its ability to deliver large-scale energy solutions. It has received confirmation for the feasibility of access and connection to 225 MW of power demand for a data processing centre in the Basque Country.

This underscores Solaria’s capacity to support major infrastructure projects and strengthens its position in the renewable energy market.

Additionally, the company has secured approval for a 213 MW power connection for a data processing centre in Madrid South. Thanks to its already built infrastructure and guaranteed grid access, Solaria can develop these data centres in record time, providing substantial cost savings on electricity – an increasingly critical factor for AI-driven operations.

With a strong foothold in renewable energy and a strategic move into the AI-driven data centre space, Solaria is well-positioned for long-term growth.

The stock remains a buy up to €9.

What we’ve been reading and looking at this month

Are we running out of data for AI? Here’s why you should care

Ever wonder if AI will hit a ceiling? It turns out, we might be heading for a data shortage –and that’s a big deal.

This article by Epoch dives deep into this looming problem and why it matters for the future of AI.

Right now, large language models (LLMs), like ChatGPT and Gemini, thrive on human-generated data – text from books, articles, websites and so on. But here’s the catch: there’s only so much high-quality data to go around. As AI models get bigger, they’re gobbling up this information faster than we can create new content. At some point, we hit a wall.

So, what happens when we run out? It could slow down AI progress, making it harder to build smarter, more capable models. It could also force AI developers to rely on AI-generated content, leading to a kind of “data inbreeding” that reduces quality and creativity. Worst case? We could see stagnation in AI’s ability to improve, affecting everything from chatbots to medical research breakthroughs.

The article lays out the facts, exploring how soon we might face this limit and what solutions – like synthetic data or better training techniques – could help. Whether you’re an AI enthusiast, a researcher or just someone curious about the future of technology, this is a must-read.

The future of AI might just depend on how we handle this data crunch.

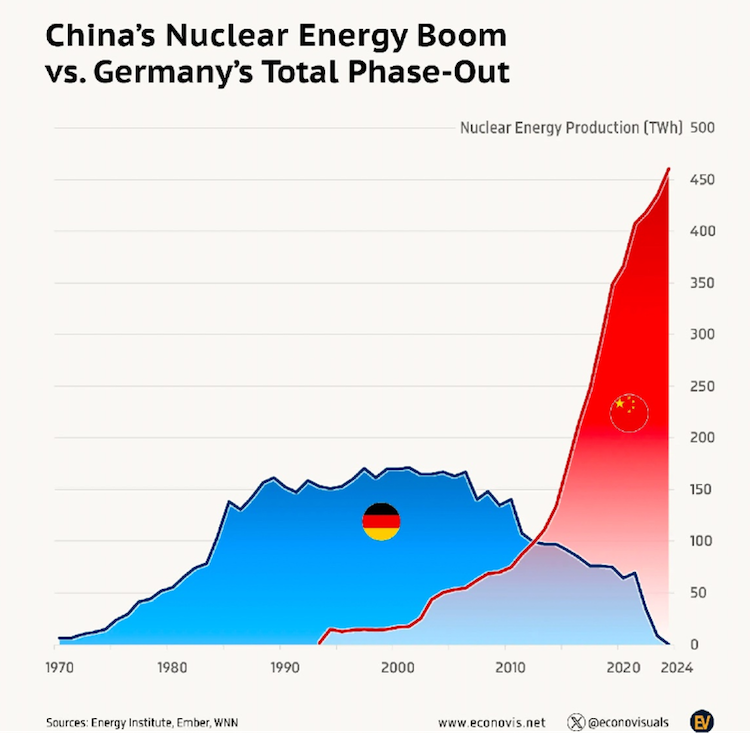

China’s nuclear energy boom versus Germany’s phase-out

Take a look at this graph on nuclear energy in China and Germany, which shows the mother of all contrasts.

From 2006 to 2023, China’s nuclear energy production surged by 690%, rising from 55 TWh to 435 TWh.

Meanwhile, Germany’s nuclear output plummeted from 167 TWh to zero, making it the only major economy to fully phase out nuclear power.

As you might know, Germany shut down its last nuclear plants in 2023, with 2024 marking the first year since 1962 with the country producing no nuclear electricity generation at al.

However, with Christian Democratic Union (CDU) leader Friedrich Merz recently winning the German election, and on track to take the reins of the EU’s largest economy, could we see Germany make the mother of all U-turns and embrace nuclear energy in some capacity again?

After all, Merz has taken a warmer tone toward nuclear energy than current chancellor Olaf Scholz. A CDU-led government could certainly reopen the conversation about nuclear energy, possibly restarting plants or spearheading a bold small modular reactor initiative.

It’s going to be fascinating to find out.

Hindenburg Research is closing – here’s why that matters

Hindenburg Research, the infamous short-selling firm that shook up Wall Street with its explosive reports, is shutting down.

Love them or hate them, their work had real consequences – some companies tumbled, investors lost billions and corporate wrongdoing was exposed.

But why is the firm calling it quits? This article by Frontline breaks it all down.

Founded by Nathan Anderson, Hindenburg made waves by targeting companies it claimed were overhyped or fraudulent. Its report on Nikola, for example, led to fraud charges against the company’s founder. Its takedown of India’s Adani Group wiped billions off its market value. But while some saw Hindenburg as a financial watchdog exposing corporate deception, others criticised its tactics as self-serving – after all, short sellers profit when stock prices collapse.

So why step away now? According to Anderson, the sheer intensity of the work – legal battles, high-profile feuds and relentless scrutiny – made it unsustainable. But it’s hard to ignore the broader implications: with Hindenburg out of the picture, will companies face less scrutiny? Or will other short sellers step up to fill the gap?

Interestingly, Anderson isn’t just walking away – he plans to open-source Hindenburg’s investigative methods, giving others the tools to dig into corporate finances. But whether that leads to more transparency or more market chaos remains to be seen.

Hindenburg may be gone, but its impact – and the debate over short selling – won’t be fading anytime soon.

James Allen and Sam Volkering

Editors, Southbank Growth Advantage