Your July issue of Southbank Growth Advantage

25th July 2024 |

- Whisper it, but Big Oil is investing in lithium – and this small cap could capitalise

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

Whisper it, but Big Oil is investing in lithium – and this small cap could capitalise

One year ago, we advised you purchase a stock to take advantage of a powerful “collision” of forces at play in the energy markets.

Ashtead Technology Holdings (AT), we said, was the perfect way to capitalise on a collision of old and new energy, set to thrive no matter how the markets evolve and the transition towards clean energy develops.

As we outlined, Ashtead, as a subsea equipment rental and solutions firm, was able to serve an oil and gas industry that was still working overtime following Russia’s invasion of Ukraine whilst simultaneously increasing its exposure to an offshore wind segment that was forecast to see rapid growth.

In short, it had placed itself at the centre of the so-called “energy trilemma”, a three-way push-pull of energy security, affordability and sustainability.

As you will no doubt recall, in early May, less than ten months after the recommendation, we sold Ashtead at a 125% gain, a huge endorsement of the underlying investment thesis.

As such, we have been busy looking to find another company that can similarly straddle old and new energy, one that is again at the core of the energy trilemma.

After a lot of searching, and a lot of researching, we believe we have found such a stock.

Although unknown to most energy market observes, this small-cap stock in question is moving to the heart of global battle to reshape the lithium industry in its attempts to reinvent how a metal key to the green energy transition is produced.

This is a battle that has sucked in tech startups, entrenched mining giants and – notably – oil producers, all looking to gain influence over an industry expected to grow to more than $10 billion in annual revenue within the next decade.

The last category is where our latest recommendation comes in.

You see, for major oil companies, lithium production offers the prospect of selling a new product with relatively little added cost.

That’s because lithium is found in saltwater deposits – and in oil brine – that exist naturally or as byproducts in oil fields.

In fact, salty brine deposits across Europe, Asia, North America and elsewhere are filled with roughly 70% of the world’s reserves of the metal, according to U.S. Geological Survey estimates.

For decades, drillers have simply disposed of that brine by pumping it back into the ground and not bothering with the lithium. But what was once considered waste is now looking much more valuable.

The fact that oil producers such as Exxon, Chevron and the like extract water containing traces of lithium as part of fossil fuel production could help the oil industry morph into the world’s largest lithium supplier.

This is no hyperbole.

Just think of the decades’ worth of research and data accumulated by the oil industry on the sediments that lie in North America alone.

The significant investment in borehole infrastructure, historical production data, expertise in production, and access to co-located resources like fresh water and reagents provides oil and gas producers with a substantial market advantage.

These companies already possess extensive knowledge about the aquifers and the feasibility of drilling into them, as they have previously conducted such operations while drilling for oil. Consequently, they can bypass the costly and high-risk exploration phase.

Oil and gas producers are facing pressure to reduce carbon emissions from operations, including from their own shareholders, so moving into the lithium space at relatively little cost is a win-win for them.

After all, while oil demand may only grow by ~1% per year to 2030, lithium demand is expected to grow by CAGR 15-20% to 2030.

Big Oil entering lithium

With those demand projections in mind, it’s no wonder Big Oil is already looking to extract the silver-white metal needed in batteries for electric vehicles, solar panels and wind turbines.

The oil and gas industry is increasingly investing in low-grade brines, with companies like Chevron, Equinor, and Schlumberger (through its NeoLith project in collaboration with Panasonic) showing significant interest.

They are following the lead of developers such as Standard Lithium and specialty chemical maker Lanxess in Arkansas.

Recently, Exxon Mobil CEO Darren Woods informed analysts that the company can produce lithium “at a much lower cost” than traditional mining methods. The oil major, is taking a diversified approach to lithium extraction, acquiring 120,000 gross acres in the Smackover formation in South Arkansas, which potentially contains up to 4 million tonnes of lithium carbonate equivalent (LCE), enough to supply 50 million electric vehicles.

The brine resources are vast.

Researchers at the University of Pittsburgh recently said lithium found from the wastewater from the Marcellus Shale gas wells in Pennsylvania could supply 40% of the metal used in the US alone.

But up to now, the oil majors have kept any development work outsourced to junior firms until one of them figures out a successful model to extract the lithium.

You see, the energy companies here aren’t talking about mining in the traditional sense.

Traditional methods of lithium mining are brine evaporation ponds and hard rock (spodumene) mining. Brines take months or years to purify the lithium with huge water use and heavy implications for the local environment, while hard rock mining of lithium is just as intensive and harmful as for any other metal.

But oil brine requires a different set of tools – specifically, an early-stage technology that promises a third option of lithium extraction: direct lithium extraction, or DLE.

DLE seeks to hasten extraction while reducing water consumption – all at a fraction of the cost. DLE consists of relatively small, modular machines that suck brine from the ground and separate the lithium, much like a coffee filter.

This technology is far less destructive than traditional mining; it operates on a much smaller scale, for one, and it doesn’t require carbon-heavy evaporation ponds that miners typically use to process lithium.

While DLE technologies vary, they aim to extract about 90% or more of the lithium from brines, compared to about 50% using ponds. This means it’s economically feasible for them to target lower grade resources such as found in oil brines.

For oil producers, DLE offers the tantalising prospect of filtering lithium from water that is already extracted alongside hydrocarbons.

Typically that water must be injected back underground at a cost. However, DLE offers the prospect of filtering lithium from that brine before it is reinjected back underground without the use of traditional evaporation ponds. This will allow the oil firms to turn a cost centre into a profit.

However, it’s important to note that this has never before been done at commercial scale.

Extracting lithium from brine is a complex chemical process. There have also been practical considerations to address, such as tackling pipe corrosion.

Multiple DLE approaches are under development, with sorption, ion exchange resins, and solvent extraction leading the charge towards commercial scale.

Within the DLE space, most are drilling into brine reservoirs and have business models like traditional junior miners, with high capex, a long permitting process, high risk, and lots of dilution for early investors.

One DLE company is targeting the oil and gas industry specifically

But the company we’re recommending today has developed a novel DLE technology tailored specifically for the oil and gas industry.

It is a founder-led, critical local resource company in North America with an advanced DLE technology that is scaling fast, a huge target market and a unique value proposition relative to its competitors.

The company is able to take produced water from the wellhead, remove various inorganics, and recover 95%+ of the available lithium via its unique sorbent, allowing the lithium to undergo further refinement into high-quality lithium carbonate or hydroxide.

It is a true industry leader, offering best-in-class technology along with the lowest operating costs among its peers. It is now well positioned to be the preferred choice for oil and gas producers and water treatment companies seeking a further revenue stream and operational savings.

Unlike many of its peers, this company is on a fast-track to commercialise its DLE technology.

The company has recently announced a 100-fold increase in its processing capabilities, with the scale-up showing lithium recovery rates of up to 99%, even with brine concentrations as low as 31 mg/L.

This means it offers the possibility of low initial capital expenditure while unlocking lithium from locations that would typically be deemed uneconomical.

This achievement confirms its ability to extract lithium from oilfield brines, setting the stage for commercial operations in the third quarter 2024, when its first field unit will be deployed.

In short, this company is set to become North America’s first commercial producer of lithium hydroxide and lithium carbonates from oilfield brine.

The firm’s name is Volt Lithium and it is our next Southbank Growth Advantage recommendation.

Volt Lithium Corp (VLT): standing out from the crowd

As said, Volt stands out by targeting the brines left behind in underground oil and gas reservoirs. These are currently viewed as a waste product by the O&G company, cleaned and reinjected to the well once the fossil fuels have been extracted. Volt will insert itself into this existing system, and extract valuable lithium to be converted into either carbonate or hydroxide.

Volt, previously called Allied Copper, is looking to partner with the oil and gas companies to use their existing infrastructure to lower capex/permitting needs and thus solve many of the challenges faced by other DLE companies, who have to go to debt or equity markets with huge funding needs for exploration, drilling wells, building production and transport infrastructure, and permitting.

To get into the industry, it doesn’t need so much capital if you’re partnering with businesses that have infrastructure in place. And, environmentally, there are almost no issues. No new wells, no new mines. The systems are already in place, they are just fitting into it.

The feasibility studies and environmental permits required by traditional projects are hugely expensive and time consuming, and not having to go through this is an absolutely massive time-saving for the company. We can expect its time-to-market to be significantly faster than the competition because of this strategy.

Volt is targeting the Permian Basin, in Texas. This is by far the largest opportunity in this space, simply due to the size and scale involved. It produces 19 million barrels of lithium-infused brine per day, making it one of the largest potential sources of lithium in the US. For every barrel of oil produced in the Permian, 4.5 barrels of water are also produced.

Texas also has a slightly different set of regulations to other states with large shale fields, like the Marcellus and Haynesville regions. There, payments must be made to either the mineral resource (underground) owner, or the surface land owner when the water comes into their possession. In Texas however, these don’t exist, and an ownership transfer occurs to Volt free of charge. That, as well as the sheer scale of the opportunity, makes the Permian a great place for the company to commence operations.

This is the source of Volt’s opportunity. The water is already extracted by an existing operator, Volt only wants to borrow it briefly to extract the lithium, before giving it back to be reinjected.

By partnering with oil firms, scaling fast and accelerating time to market, Volt has a DLE solution for the lithium market today. This is unlike anything I’ve seen elsewhere.

Rapid improvements in scale, with high efficiency

Volt has already proven its technology at a pilot project in Alberta, Canada, at a place called Rainbow Lake. It has run this pilot extensively in recent years with a high focus on reducing operational costs. This has gone very well, with the company recently announcing a two-thirds reduction in operating costs in under a year.

As said, it has also scaled up production capacity to 96k litres/day, which is 100x more the previous reported capability. Alongside this uplift, it has managed to maintain a 99% lithium extraction rate, as well as improving some key operational aspects like extraction time.

Volt is managing to scale efficiently, which is a classic tripping point for many emerging technologies. And what’s more, it has achieved this at very high extraction rates and at low cost, two of the key challenges for DLE players.

As a result, it has signed a groundbreaking agreement with an oilfield operator in the Delaware Basin, which has brought a $1.5 million investment to build a field unit on its site. This project is critical, as all other players in the basin will be watching to see if Volt can deliver value for its partner.

This agreement has the potential to consummate into a full-blown partnership, resulting in more capital and a plan for full deployment into the company’s operation.

This partnership arrived after nearly a year of due diligence and was no mean feat. Getting an agreement over the line with a major operator is a huge achievement. Hopefully more agreements are in the pipeline.

The idea is that Volt can reduce operating costs for these companies by performing some of the water cleaning process it already does on their behalf, saving them one step in their waste processing.

Progress in the pilot project is encouraging. Testing in February of brine associated with Cabot Energy and Cenovus oil wells dating from the 1960s showed a cost of just $2,885 per tonne of LCE versus $8,057 in May. This compares extremely favourably to current lithium prices at around $11,500/tonne, which are themselves around multi-year lows.

Certainly, this strategy will also allow Volt to start small, with lower upfront costs and very early cash flow positivity.

A traditional mine, even before the first tonne of ore is pulled out of the ground, needs to be built at profitable scale, let’s say for 20,000 tonnes of lithium plus per year. That needs tens, maybe hundreds of millions of dollars of upfront costs, which needs to be raised based on careful forecasting and engineering plans. It’s a risky and expensive business.

Volt, meanwhile, can start generating cash flow from a single small project with just a few million dollars of capex, growing organically with operating cash flow funding future projects. This is a unique proposition in mining that greatly lowers the risk profile of the business at this early stage.

What is also unique is that Volt’s proposition appeals both to an oil and gas industry looking to reduce operating costs and to ESG funds by encouraging electrification with no additional need for drilling and without the huge water footprint of brine ponds.

Catalysts abound

Volt has already proven its ability to surge on positive news, rising around 35% in a single day on Wednesday 17 July, as it announced a 100-times scale-up in its processing capabilities.

As said, the scale-up has shown lithium recovery rates of up to 99%, even with brine concentrations as low as 31 mg/L. This achievement confirms Volt’s ability to extract lithium from oilfield brines, setting the stage for commercial operations in the third quarter 2024, when its first field unit will be deployed.

That in itself will be an important catalyst to potentially push the stock to higher ground, though there are two other near-term catalysts that could also send the stock shooting higher.

Firstly, we still don’t know the name of its first partner in the Delaware Basin, but we know that companies like Exxon and Occidental Petroleum are looking actively at DLE.

The naming of that partner could be a big moment if it’s a big enough name and certainly if success in their joint field project attract others firms to look at Volt’s technology.

Certainly, if Volt can prove its capabilities at scale, the numerous other confidential conversations its CEO has admitted to having with major Permian Basin operators could be converted into new partnerships.

Secondly, on the sales side, offtake agreements with major automakers would also help get more institutional investors on board. Tesla, for example, imports 40% of its lithium from China, and has a large battery plant that is in Texas, just like the Permian, so there’s an obvious candidate right there. But Stellantis, GM and others are all scaling up the battery side of things.

So you can have big oil and gas names on one side and big EV and automaker names on the other, both giving the stock near term catalysts, while the long-term share price will be driven by operational growth and lithium price movements.

Understated, strategic, accomplished

Volt’s management is a little unusual for a small, growth, technology company.

Typically bold, optimistic and gung-ho – managers of such companies are used to pandering to the Silicon Valley/San Fran VC crowds, who want huge target markets, rapid growth projections and the rest. Those investors have trained growing small companies to pose as the next Amazon or Tesla.

However, Alex Wylie, president and CEO of Volt, operates a little differently.

He’s not trying to raise tens of millions of dollars for the upfront capex on a traditional mine. When he speaks, he constantly references early cash flows, and organic, self-funded growth. He often alludes to shareholders, and his respect for them and the importance of treating them well, and not diluting them unnecessarily.

For example, when asked why the company only raised $1.5 million with its first strategic partner in the Permian, he said that was simply what the company needed to get the field project up and running on site, no more or less.

This suggests capital discipline and patience, two valuable traits in a CEO.

He is also reasonably understated and quiet about the possible opportunity size or the extent of its technological advantage, saying he felt blowing a load of smoke would just attract the attention of their competitors, giving the game away. He “wants to let the results speak for themselves” when the time comes. He deals in proof, not promises.

I also believe it helps that he co-founded the business and has brought it this far, suggesting a degree of personal mission and ambition with this project, and not any other – unlike you see with some mercenary CEOs.

His co-founder Marty Scase is also still there on the board, too, alongside the former commander of the Canadian army, a PHD chemist, a finance exec and an oil and gas exec – so a very strong mix of fossil fuel, finance, chemistry, operations and company-specific expertise.

Strategically, I’m very impressed as Volt has clearly differentiated from its competitors, with a low-cost path to production, a focus on operational efficiency and a solid history of timely execution and technological progress.

I’m certainly very impressed by Wylie, and it seems like he’s built a good team around him with a good track record.

On a path to commercialisation

The financial state of the company must be framed in terms of its path to commercialisation.

We have made clear that, financially, this will be a faster and much less capital-intensive path to production than for most other “junior miners” you might compare it to.

Costs might be up to $20 million for a DLE plant on site, which the CEO expects to jointly-fund with the relevant oil or gas partner. This compares to hundreds of millions for traditional mines or brine systems. He wants to work in partnership with the industry and believes a 50/50 cost and ownership is a good way to achieve this.

This will mean low upfront capex and a swifter, slower ramp in cash flows. They will start small but grow organically, rather than building to 100% scale before the first tonne is mined.

Thus, we should think of it more like a traditional non-commodity business when it comes to financial forecasts.

In terms of its capital structure, it has around $3.1 million of cash and equivalents, following the recent announcement and zero long-term debt.

Then, this time last year, it gained $6.8 million via an equity raise. Volt was running low on cash before this recent strategic investment. Now that the share price is doing better, it’s certainly possible more will be raised from equity markets in the next 12-24 months.

It is currently a very capital-light business, but that’s because commercialisation is just beginning. The current set-up tells us very little about how things will look in 2-4 years’ time. The important thing is the capex and cash flow dynamics of that commercialisation, as we’ve outlined.

In terms of valuation, they are valued like an early-stage venture but have a very advanced project profile. This mismatch is where I see the opportunity.

If lumped in with the broader DLE industry, you would think it is also many years away from production and delivering any returns, but this is wrong. Volt’s unique approach will make it first to market, and as markets wake up to this fact the revaluation could be swift and extensive.

More broadly, there has been a recent, violent move in small-cap stocks, especially in North America. Long neglected as more and more capital flowed to the big winners from the AI trend, the suddenly very real possibility of falling interest rates has given them a boost.

However, they have fallen a long way behind large caps in relative terms, so if this is the beginning of a rotation or catch-up trade, there is a long-term tailwind behind Volt, and this is a great time to be getting in.

Be aware of some key risks

There are five key areas of risk for the company, despite the many advantages it seems to have. These are around company-specific things, namely its technology, execution, and competition as well as the broader issues of lithium prices and regulation.

Technology: a large part of the investment case rests on two key things: the ability to maintain extraction rates at much larger scale, and the ability to further reduce operating costs per tonne at greater scale.

The latter is likely, as scale and time generate feedback loops that naturally lower costs through efficiency and power, while the former tends to be one of the key challenges to emerging technology companies.

Hitting 98% extraction rates in the lab or at a small-scale pilot is very different to doing it with billions of litres of water on site in Texas, and we must watch the ramp up closely for signs of deterioration in technological performance.

Execution: a failure in the current field project could set the company back years as it has to prove and regain the trust of potential industry partners. Volt must continue to execute on its milestones in a timely way that demonstrates operational progress.

Competition: I have explained why I believe Volt stands out from the DLE crowd, but it is a fast-moving space and with many other players chasing technological improvements, a breakthrough elsewhere could see other methods dominate. We cannot know if that will come, or from where, but we must remember that DLE is currently 0% of global lithium production and already has many competitors vying to break into the market – this is not an uncompetitive arena.

Lithium price: this is almost entirely out of the company’s control, but is massive factor in its share price performance. This is the classic risk in commodities investing: the team, project, and tech can be as wonderful as you like but for long periods, these can all be outweighed by a falling product price. The reverse is also true though, and quality operational performance will win out through a cycle.

Regulatory: changes in the tax structure around transfers of resource ownership in Texas to mimic those in other oil-producing states could increase average operating costs for Volt’s process. Other, unforeseen regulations will also undoubtedly impact Volt, and while I believe politics will favour it whoever wins in November, it looks like being a volatile six months regardless and that can deter investment in the meantime.

The stock has run up recently so let’s hold fire for now

As said, Volt has a huge market, a unique and advantageous strategy and is on a fast track to commercialisation. It’s led by an adept management team, with very well mitigated risks, and an attractive financial profile looking forwards, all in a massively overlooked sector with powerful long-term drivers in lithium.

However, since it announced a 100-fold increase in its processing capabilities on 17 July it has gone on a tear, rising from C$0.23 to C$0.42 today.

This has been incredibly frustrating to watch but I fully expect the price to weaken as some of the recent euphoria dissipates.

Although I remain excited with the company’s prospects and still feel it’s very cheap relative to its future opportunity, I don’t want you to overpay in the short term, hence why I putting a buy limit of C$0.37 on the stock – a level I will continue to monitor.

As such it will go on our watch-list but as soon as it dips to C$0.37 or below in intraday trading it will go into the model portfolio as a BUY.

Ticker: TSXV: VLT

ISIN: CA92873W1005

Market cap: C$54 million

52-week high/low: C$0.15 – C$0.42

Buy up to: C$0.39

Big Breakthroughs

Sam:

The last couple of weeks has seen a significant acceleration in the capabilities of various AI models from some of the world’s biggest tech companies.

Elon Musk recently announced that his xAI team had the “most powerful AI training cluster in the world,” operating on 100,000 Nvidia H100 GPUs.

Source: Elon Musk via X.com

For what it’s worth, that’s around $3 billion in Nvidia GPUs.

But that wasn’t the really big news or important release for AI…

Only a day later Mark Zuckerberg and Meta released an upgrade to their Llama 3 model, Llama 3.1.

Now when you see “upgrade” in this context, it’s important not to just assume it’s like upgrading your operating system with a slightly better interface.

What Meta has released here is monumental. I think it warrants a closer look because the speed at which these AI models are increasing is becoming exponential. As scared as some people might be about it, understanding it is paramount to not being afraid of what’s in development.

So… what is Llama 3.1?

Llama 3.1 is the latest iteration of Meta’s open-source AI models. Technically there’s a few version of Llama 3.1 but the one we’re interested in is Llama 3.1 405B, with the “B” standing for billion, so 405 billion parameters.

This model, along with improved 8B and 70B versions, can handle a much wider range of tasks. These tasks include answering general knowledge questions, solving complex mathematical problems, translating languages, and using tools to assist with coding and content creation.

But one of the biggest and notable improvements in Llama 3.1 is its expanded context length of 128K tokens.

Confused yet? Let me explain more…

This means the model can process and understand much longer pieces of text, making it ideal for summarising long documents, carrying on extensive and more complex conversations, or doing a far greater job of analysing detailed reports. This extended capability significantly enhances its use in real-world applications.

Now what’s also fascinating about this is the decision to make it open-source AI.

As I’ll explain a little later in our section on what we’ve been looking at this month, historically, companies have sought to control their tech and protect their “moats” at all costs. This is also true of AI technology.

By releasing such an advanced model as open source, Meta is democratising access to cutting-edge AI technology. This move allows researchers, developers, and organisations worldwide to utilise high-performance AI without the substantial costs typically associated with proprietary models.

The aim of this is to foster innovation. With open access to Llama 3.1, developers can experiment, create new applications, and improve existing processes. The shared nature of open-source projects also means that improvements and new discoveries can be quickly disseminated and built upon by the global community, accelerating overall progress in the AI field.

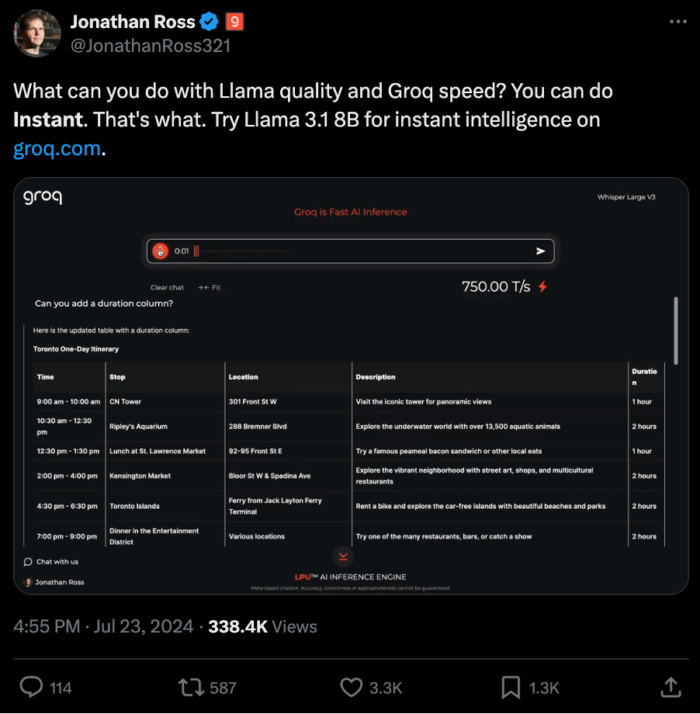

So what might that look like in an actual real-life situation. Well thankfully there’s already an example online, albeit this is Llama 3.1 8B… and if 8B is this good, you start to get an idea of what 405B can do.

You’ll see below a tweet from Johnathan Ross (not the UK talk show host) that shows a video of what it can do. Head to this link here and make sure to have your sound on.

Source: Johnathan Ross via X.com

So what does this mean for Meta?

Well, Meta is not just releasing a powerful model; it is building a comprehensive ecosystem around Llama 3.1. This includes partnerships with over 25 major companies like AWS, Nvidia, Google Cloud and Microsoft Azure. These collaborations ensure that developers have the infrastructure and tools necessary to deploy and scale Llama 3.1 effectively.

In other words, you might end up using AI in your day-to-day life, and “under the hood” it’s Llama AI models doing all the AI grunt work.

Of course it’s not all just about Llama. We know there are other competing AI models, including OpenAI’s GPT-4 and Google’s Bard. This healthy competition, and the progressive approach to open-source Llama from Meta, is really a win-win for the speed of which AI can move forward.

Meta’s release of Llama 3.1 marks a significant milestone in the evolution of AI. Not only could this dramatically accelerate the speed and adoption of AI into all industry globally, but it may also prove to be a significant level up for Meta as a company as well.

It makes me think that its name change to Meta a couple years ago, due to its vision on the metaverse, was a little premature. Maybe it should have waited to call itself something a bit more AI focused…

Buy List update

European Metals Holdings (AIM: EMH)

At the time of writing, European Metals Holdings is trading around £14.12, 2.6% down over the last month, with the stock now 57% underwater in the model portfolio.

European Metals part owns the Cinovec lithium asset in the Czech Republic, one of very few advanced-stage, large-scale lithium projects in the European Union with a mineral resource of nearly 7.4 million tonnes of contained lithium carbonate equivalent.

The project is being developed by Geomet, a joint venture between EMH and Czech-state-owned CEZ.

Shareholders continue to wait for news of the publication of the delayed definitive feasibility study (DFS) for the Cinovec project.

Originally slated for release in the first quarter, the DFS delivery has been postponed owing to continued engineering work and social and environmental engagement efforts.

Although the company says these efforts have unearthed potential improvements to the lithium processing component of the study, we still don’t know exactly when the process will be completed.

Meanwhile, lithium prices languishing near three-year lows are hardly helping matters.

With that in mind, let’s move to the stock to a HOLD while we wait for news of the DFS.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF has fallen by 5% over the month to trade last at around £5.31 at the time of writing, putting it around 41% below our £8.96 entry price.

LITG is designed to capture the full lithium cycle, encompassing activities from mining and refining lithium to the production of batteries, reflecting its comprehensive investment strategy within the evolving battery technology and electric vehicle market.

It seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Global Lithium Index.

The ETF maintains significant positions in major players within the electric vehicle (EV) and battery sector, including Tesla, BYD, LG Energy Solution, TSD and Samsung SDI.

By owning mining, refinery and battery production companies in the fund, Global X has its fingers in multiple parts of the lithium industry.

Of course, the ETF is expected to benefit from increased demand for the silvery-white metal from EV, renewable energy storage and mobile device industries.

However, increasing supply of the white metal, particularly in the China market, has caused lithium prices to fall since hitting record highs in 2022.

However, once lithium inventories clear, we should see prices pick up.

With the ETF providing easy access to a secular growth trend that’s nowhere near ending, LITG remains a core position in the Southbank Growth Advantage portfolio. It remains a BUY.

Central Asia Metals (AIM: CAML)

Central Asia Metals (AIM: CAML), a mining company with operations in Kazakhstan and North Macedonia, has lost 5% over the last month to 194.20p at the time of writing, leaving it 30% underwater in the model portfolio.

The group’s principal business activities are the production of copper at its Kounrad operations in Kazakhstan and the production of lead, zinc, and silver at its Sasa operations in North Macedonia.

In an announcement on 11 July, CAML said that during the first-half of the year, Kounrad achieved copper production of 6,608 tonnes, slightly down from 6,716 tonnes in the first six months of 2023.

Meanwhile, Sasa produced 9,014 tonnes of zinc-in-concentrate and 12,872 tonnes of lead-in-concentrate, compared to 9,764 tonnes and 13,734 tonnes, respectively, in the same period last year.

As of 30 June, CAML had $56.4 million in cash.

Looking ahead, CAML said Kounrad was on track to meet its full-year copper production guidance of 13,000 to 14,000 tonnes. But Sasa was expected to achieve production towards the lower end of its 2024 guidance, with zinc-in-concentrate ranging between 19,000 to 21,000 tonnes and lead-in-concentrate between 27,000 to 29,000 tonnes.

“Kounrad performed well during the second quarter of 2024, bringing first-half production into line with prior years, after facing some difficult winter weather conditions in the first quarter of this year,” said chief executive officer Nigel Robinson.

“Production at Sasa in both the second quarter and the first half 2024 has been impacted by a modest reduction in mined tonnage, owing principally to the short-term challenges inherent in the transition to a new mining method.

“This transition, which continued during the quarter, will be of material benefit in the longer-term, by sustaining the life of both the underground mine and its associated tailings storage facilities.”

Robinson said the company looked forward to an improvement in mined tonnage at Sasa during the second half, as the mining transition progresses.

“However, taking into account the production levels achieved during the first half, we expect full-year production at Sasa to be towards the lower end of our previously announced guidance,” he added.

In a separate announcement, CAML said that CEO Nigel Robinson will step down on 1 October after leading the company for more than six years.

The AIM-traded firm said Robinson would be succeeded by Gavin Ferrar, its current chief financial officer, who had been with CAML for a decade.

Robinson will remain on the board initially as an executive director until 1 April 2025 to support the transition before continuing to serve as a non-executive director.

The company also said Louise Wrathall, the executive director of corporate development, will assume the role of CFO on 1 October.

Weaker copper prices are also likely weighing on the stock. Since rising to a record in May, copper prices have fallen by around 15% amid rising exports from China, shifting the market into a surplus.

However, as we said last month, Central Asia Metals still looks good value, with City analysts expecting earnings will soar 27% year on year in 2024.

This means the company is trading on a forward price-to-earnings (P/E) ratio of around 10.3 times. At the same time, a price-to-earnings growth (PEG) ratio of 0.4 suggests the share is undervalued.

Finally, Central Asia Metals carries a huge 9.16% dividend yield for 2024.

Of course, the miner’s bright earnings forecasts are underpinned by a strong outlook for copper prices given favourable demand and supply dynamics.

With its ultra-low-cost operations, CAML could certainly thrive in the years ahead.

As such, CAML is a BUY under 310p.

Foresight Sustainable Forestry Company (LON: FSF)

Foresight Sustainable Forestry Company, which invests in UK forestry and afforestation assets, continues to hover under 97p, around 11% down in the portfolio, ahead of its £167 million takeover from private equity firm Averon Park.

Averon Park offered to buy all of FSF’s shares at 97p each, with FSF set to delist immediately after the deal goes through.

Shareholders of Foresight Sustainable Forestry Company have now overwhelmingly voted in favour of the takeover, with the acquisition set to be finalised by a court-sanctioned scheme of arrangement that’s expected to be held on 26 July and then become effective on 30 July.

As such, the stock will now be sold from the model portfolio at 97p. We wish the company well now that it’s in private hands.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation, the world’s largest gold miner, is trading around $47.70, 14% up on the month. The stock remains 27% below our $65.39 entry point.

Rising hopes of a US interest rate cut in September, uncertainty around US elections and global geopolitical risks have boosted gold’s safe-haven appeal, lifting it to record-highs.

Bullion hit an all-time high of $2,483.60 on 17 July.

After market close on 24 July, Newmont reported a profit for its second quarter that increased from the same period last year and beat analyst expectations. The company benefited from robust production and higher prices.

The company’s bottom line totalled $853 million, or $0.74 per share. This compares with $155 million, or $0.19 per share, in last year’s second quarter.

Excluding items, Newmont Corporation reported adjusted earnings of $834 million or $0.72 per share for the period.

The company’s revenue for the quarter rose 64.2% to $4.40 billion from $2.68 billion last year.

Attributable gold production rose to 1.61 million ounces in the second quarter from 1.24 million ounces a year earlier, while average realised gold price was $2,347 per ounce in the quarter ended 30 June, compared to $1,965 per ounce a year earlier.

Newmont’s all-in-sustaining cost, which reflects total expenses associated with production, rose to $1,562 per ounce of gold from $1,472 per ounce a year earlier.

The precious metals miner continues to expect total annual attributable gold production of 6.9 million ounces.

Newmont remains a BUY under $100.

Stellantis NV (NYSE: STLA)

We recommended multi-car brand giant Stellantis at $22.84 in the January issue. At the time of writing, its shares are trading at $19.60, putting it 14% down in the model portfolio, after falling 5% over the last month.

The stock reached an all-time high at nearly $30 on 25 March but has since fallen back, in part due to an industry-wide sell-off sparked by concerns over EV demand and more recently on the European Commission’s decision to slap tariffs on imported Chinese EVs.

Like many automakers, Stellantis continues to be wary of the influx of Chinese-made electric cars making their way into Europe.

According to Reuters, CEO Carlos Tavares said that the company is “ready to fight” the brutal challenge of the Chinese EV offensive.

“We are going to be challenged and I would say brutally challenged by the Chinese offensive on the European market,” Tavares said on 22 July during the opening of a new EV production line in Serbia.

“At Stellantis, we are ready for the fight,” he added.

The former Yugo plant in Serbia is a key part of Stellantis’ fight with the influx of Chinese-made EVs.

Production costs are lower at the Serbian Kragujevac factory than in Poland, France and Italy, which will help keep prices down.

“We are going to demonstrate to them that … we are hard-working, we are going to demonstrate to them that we have the right technology, we are going to demonstrate to them that we are a very fierce competitor,” added Tavares.

In company results released on 25 July, net income fell 48% in the first six months of the year to €5.6 billion, with the company blaming lower volumes and an unfavorable sales mix as inventories in the US remained high.

Margins declined significantly in North America, where shipments fell 18%, mainly due to lower volumes, product mix headwinds and negative net pricing, the company said.

The company pledged additional measures to cope with a steep drop in sales.

Stellantis has already extensively cut costs, with €500 million more in savings to slated for the second half of the year.

“The company’s performance in the first half of 2024 fell short of our expectations, reflecting both a challenging industry context as well as our own operational issues,” Tavares said in a statement, adding that the carmaker is taking “corrective actions” to address the problems.

Stellantis reiterated it’s launching 20 new vehicles this year to help boost momentum.

CFO Natalie Knight said price adjustments were possible in order to unload excess supply.

However, the company backed its guidance for 2024.

With the outlook for the second-half of the year better, the stock remains a BUY while it trades below its buy limit of $23.50.

Prysmian Group (IL: 0NUX)

Prysmian Group, which entered the model portfolio at €48.13 in the March issue, now trades at €63.66, around 8% up on the month and 32% up in the model portfolio.

Last month, the Italian cabling giant said its board of directors had approved the launch of a programme to buy back a maximum of €375 million of its shares. In a statement, Prysmian added that the board also decided to proceed with the early conversion of a €750 million convertible bond due in 2026 into capital.

The buyback programme involves a maximum of 8 million shares, equal to around 3% of the company’s share capital, said Prysmian, adding that it will be implemented from 10 June 2024 until 10 March 2025.

As of 12 July, the company had purchased a total number of 977,195 shares for a total consideration of €56.9 million.

In operational news, the company said it has performed what is said to be the industry’s first installation of an HVDC cable at a water depth of 2,150 metres.

Prysmian completed the sea trial tests for ultra-deep installation of a 500 kV HVDC MI cable at a 2,150-metre water depth, stating that this is industry record-breaking as it is the first time an HVDC cable is laid at such a depth.

According to the company, the success of the sea trials is the result of many laboratory tests and this non-metallic armoured cable, designed with a composite material based on high-modulus synthetic fibres, shapes the new generation of cable technology.

The cable will be employed for the €1.7 billion Tyrrhenian Link, awarded in 2021 by Terna. Under the contract, Prysmian will design, supply, and install a total of over 1,500 kilometres of submarine cables to support the power exchange among Sardinia, Sicily and Campania, reinforcing the Mediterranean energy hub.

The installation is carried out by cable laying vessel (CLV) Leonardo da Vinci.

The stock remains a buy under its buy limit of €60.

SilverCrest Metals Inc (TSX: SIL)

SilverCrest Metals, recommended in the May issue at C$12.55, has gained 15.62% over the last month to trade last at C$12.88.

In a market update, the silver producer announced a strong second quarter at its Las Chispas Operation with record revenues of $72.7 million, a 34% increase in treasury assets and robust precious metals production.

The company reported significant increases in gold and silver prices, contributing to its financial growth and operational success.

SilverCrest also boasted impressive processed grades and recoveries, positioning it well to meet its annual sales guidance, which also highlights its operational efficiency.

The stock remains a BUY up to C$16.

Aura Energy (LON: AURA)

Aura released an investor presentation mid-month highlighting the significance of its Tiris project and the potential resources of Häggån in Sweden. This gave the stock a handy boost sending it higher to around 8.5 GBp.

The stock has traded with some volatility since, but we still expect that Sweden will unlock uranium mining and that will be a major catalyst for Aura Energy to shoot higher in the long term.

We stick with the position.

CleanSpark (NASDAQ: CLSK) and Hut 8 Corp (NASDAQ: HUT)

Both stocks have been volatile around the positive and negative news flow around bitcoin and subsequently its market price.

After a period of decoupling from the bitcoin movements, they now look to be trading more in lockstep with bitcoin’s price. The assumption is the market had oversold the stocks post bitcoin’s halving, and there was a period of readjustment. Notably this is due to the realisation that bitcoin miners in terms of GPU infrastructure likely play a long-term important role in not just bitcoin infrastructure, but also AI infrastructure.

Nonetheless, the positive momentum behind bitcoin thanks to the Trump administration being very pro-bitcoin has been a significant tailwind for both bitcoin’s price and that of the miners.

We expect that to continue through to the big catalyst of the US elections in November. Should Trump get in, we think bitcoin will fly. Should the Democrats retain power, well it might be a choppy few months. But long term, we still think the bitcoin price and that of the miners is higher for longer.

Cyngn (NASDAQ: CYN)

Cyngn’s volatility continues, and while the company has regained Nasdaq listing compliance, its stock price is still heavily down.

But as we’ve seen, this stock can and does move hard and fast – just, unfortunately, in both directions at the moment. We’ve had days where it will be up 100% in a day, and then trade sharply lower. As frustrating as that is, we still think the company can commercialise the tech and that autonomous warehousing systems is a significant market, which it continues to penetrate.

We will remain with the position but will lower its reverse-stock-split-adjusted buy limit to our adjusted entry price of $34.69.

Oklo Inc (NYSE: ALCC)

Oklo has also been volatile in trading. It has been moving in tandem with the wider market as growth stocks were heating up, then with the cool down and selling off of tech and growth in the last week or two.

Nonetheless, the company continues to progress forward. Mid-month it demonstrated successful stages in its fuel recycling processes.

Oklo estimates its recycling programmes can save up to 80% on fuel costs, which only goes to provide for more efficient and cost-effective reactors for energy creation. Again, this is a long-term investment. Although month to month there will be developments and volatility, long term we see this as one of the most exciting energy plays in the market today.

Inside the lives of James and Sam

Sam:

Warning: humblebrag incoming.

I’ve been gearing up in the last week for the Olympic games. I’ve made sure I’ve got all the right sport channels (it’s all on Eurosport here in Portugal). I’ve also prepared my boys to understand a bit about the Olympics and that they get to choose between Australia and Great Britain.

Their future inheritance solely depends on their choice.

Just kidding. They’ll choose the one that wins the most… and we all know who that will be…

But for all the fun and games (quite literally) of the Olympics, and even though it’s in Paris, I have no desire to go there this year. Maybe in Brisbane 2032 I’ll go with the family. Good enough and my eldest might even be competing…

There’s also a good chance neither will be competing in the “regular” Olympics, and instead they’ll be competing in the “new” Olympics.

To understand what I mean by that (and here comes the humblebrag) I’m going to wind back the clock one-and-a-half Olympiads (six years).

On 13 July 2018 in one of my previous publications I wrote the following:

Fact is that video gaming is as much a sport as chess, tennis or snowboard half pipe.

And what you might not realise is it may even become an Olympic Sport. ESPN is taking e-sports primetime. But the International Olympic Committee (IOC) is taking it mainstream.

The 27th of July is the important date for ESPN.

But the 21st of July might just be even more important. On the 21st the IOC and the Global Association of International Sports Federations will meet.

On the agenda is eSports. They will seek to determine just how sport-like this is. And quite likely how the can market and leverage the increasing global appeal.

Now this may result in an eSports Olympics. That could be like the Summer or Winter Olympics. Maybe also held once every four years but solely different esports.

Or maybe there’s an event at a winter or summer Olympics that’s solely esports.

I think the first option is more likely. Imagine that every year there was an Olympic event. That way in between Olympic four-year cycles there would be other Olympics to fill the void. A huge money-making opportunity.

Then just a few days ago, the International Olympic Committee (IOC) published this landmark announcement:

IOC enters a new era with the creation of Olympic Esports Games – first Games in 2025 in Saudi Arabia

History was made today when the International Olympic Committee (IOC) decided to create Olympic Esports Games. The first edition will be held in 2025 in the Kingdom of Saudi Arabia.

So that means there’s the Summer Olympics, the Winter Olympics and as I first noted six years ago, and which is now very much exactly what I predicted, the eSports Olympics.

In short, I was right. And for me, that’s pretty much made my month!

James:

Jealousy is an unspoken emotion of all football fans, and I’m not the one to prove an exception to this particular rule.

On the evening of Wednesday 10 July, just ten minutes after I had watched England beat the Netherlands in the semi-finals of Euro 2024, my phone rang – and all sense of euphoria and excitement at what I had just witnessed on television quicky turned to disproportionate envy.

On the other end of the call was my twin brother.

He hadn’t called to analyse the game or discuss Ollie Watkins’ brilliant last-minute winning goal, but instead to triumphantly tell me that he had already secured a ticket for the final against Spain in Berlin, just four days away.

But he didn’t just have a ticket. He had already booked flights, too. He was definitely going – unlike me, who most definitely wasn’t.

This was a problem, let’s be clear.

Despite securing tickets, I had missed out on going to both England’s semi-final and final of the preceding European Championship games at Wembley in 2021 because I had been struck with Covid and decided to stay away from the stadium, good citizen that I am.

Back then, I spent most of both games watching from the sofa in an extreme quandary, desperately wanting England to win but also tormented at the prospect of my brother and friends gloating at the fact that they had witnessed England ending all those years of hurt in person and that I had missed out.

I had got away with it that time as England lost the final but I couldn’t let it happen again. I just couldn’t risk it.

So just minutes after I had been making plans to watch the final with my family on television, I was now determined that I would be at the final in Berlin, come what may.

But the problem was that tickets weren’t easy to come by, at least not at vaguely realistic prices. My brother had secured his ticket from a friend of ours with an “in” at Uefa – and only had to pay face value.

I quickly called that same friend who told me that there was a possibility that his Uefa contact could secure one more ticket but it was very much a long shot and I should pursue other alternatives.

Two days of exhausting all possible options to secure a ticket at what I deemed an acceptable price followed. On Friday evening, my fate seemingly clear, I was eying up a ticket from a secondary ticketing website at an eye-watering price when my friend with the Uefa contact called me.

Although the Uefa ticket still hadn’t come through, he had just been offered the chance to buy two tickets – again at face value – from another friend of his who was a Club Wembley member who couldn’t make it to Berlin. If I wanted them, I had to take them both, not just the one. This was an offer that was too good to be true and I snapped it up with the proverbial two hands.

Two dilemmas followed.

One, I needed to find a friend who wanted to take the second ticket off my hands and, two, I had to work out exactly how I was going to get to Berlin.

Looking at the (non) available flight options, I decided to lump the problems together. I would get to Berlin by car (via Eurotunnel LeShuttle) – but as my EV and its 150-odd miles of range was not up to the task of driving the 1,000 miles to Berlin in any acceptable timeframe I would need to find a friend who both had the wheels and wanted the ticket.

One call later to an old friend from school and both problems were solved. He would both take the ticket off my hands and drive us all the way to Berlin. We decided we would set off the following morning – one day before the game on Sunday night in Berlin. Another mate then heard whispers of our plans and said he’d like to join us too – and would take his chances on getting the “Uefa” ticket if it came through.

What followed was a quite brilliant trip, despite the disappointing result in the match. The three of us were on LeShuttle at Folkestone by 2pm on the Saturday, before driving another 5 hours from Calais to Dortmund where we decamped at a motorway-side hotel for the night. The friend who made the last-minute decision to join us in the car found out that night that the Uefa ticket had come through, so he was especially buoyant.

An earlyish start the following morning meant we arrived in Berlin at around 3pm, with plenty of enough time to check-in to our hastily booked hotel and to sample some of the pre-match festivities with my brother and around ten other assorted friends who had made similar last-minute trips and all had a story to tell.

Although the match was compelling, and the stadium atmosphere electric, the game ultimately ended in disappointment for England fans, though it was fair to say Spain deserved their victory. All the Spain fans we met after the game were gracious winners.

We were back on the road the following morning and drove all the way back to Calais – and then London – in one go.

That journey passed by in a haze of petrol stations and onshore wind turbines that dotted the German and Benelux landscape, giving clean energy some manner of revenge against fossil energy that had triumphed in transporting us to and from Berlin. What a trip!

My brother (left) and I before the big match!

Crypto Corner

MtGox is over (a decade on)

Sam:

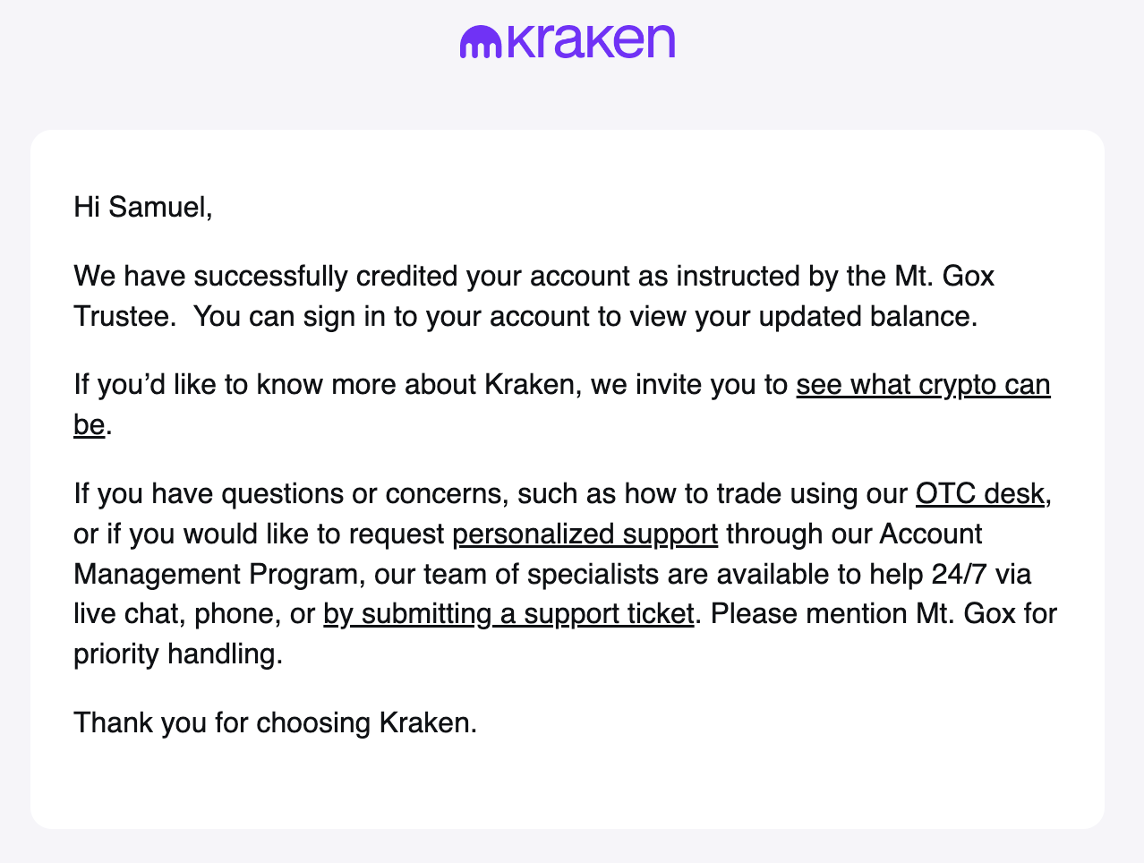

Last week I got an email:

From: MtGox Bankruptcy Trustee

Subject: [MTGOX] Completion of Cryptocurrency Repayment / 仮想通貨弁済の完了について

(日本語は英語の下部に記載されています。)

Dear Sir or Madam,

1 Completion of BTC/BCH Repayment

On July 16, 2024, the Rehabilitation Trustee made a blockchain transfer of the BTC/BCH amount repayable to you as the Base Repayment and the Early Lump-Sum Repayment or the Intermediate Repayment. This transfer was made to Kraken, which you designated as your Designated Cryptocurrency Exchange etc. on the MTGOX Online Rehabilitation Claim Filing System (i.e., the system accessible via https://claims.mtgox.com/; “System”). In accordance with the Rehabilitation Plan, the repayment took effect at the time the transfer was recorded on the blockchain.

This was followed by an email from Kraken to say the bitcoin and Bitcoin Cash would be credited within seven to 14 days.

Then on Tuesday evening this week, I got the following from Kraken:

I checked my account.

Yep. It was all there. Well, I say “all” but it was a fraction of the actual bitcoin that was on MtGox when it shut down and went bankrupt ten and a half years ago.

Ha. A decade to recover a portion of bitcoin held on an exchange.

It feels like a badge of honour. But in reality, it’s a badge of stupidity.

And I want my badge to be your lesson that hopefully you never have to deal with.

You see, holding bitcoin on exchange, any exchange is somewhat risky. But then again, holding any asset with any third party is inherently risky. And yes, that includes your bank.

That’s because at any given time you can be shut out, frozen out, or simply see your account closed.

You might think that’s impossible with the banks. But then again hopefully you saw the news last week when there was a “mass IT outage” worldwide thanks to some failures of IT services company CrowdStrike and a bunch of Microsoft-based systems.

As the BBC noted:

A report on Bloomberg was a little more direct:

The point being that accounts were frozen and access was shut out for people all over the world.

It may not have ever happened to you. It’s happened to me before. But getting shut out of access to your cash is horrific. It usually gets resolved. But unless that’s handily between 9am to 5pm, Monday to Friday (and in the correct time zone), then you’re in a spot of bother.

But you know what was still operational? Bitcoin’s network. And any self-custody bitcoin wallet was easily and happily able to send bitcoin anywhere it was needed. If you needed to use bitcoin to pay for something, you still could.

The key takeaway here is that if you need to hold bitcoin on an exchange, I understand. Sometimes it is necessary. But in doing so, be aware that nothing is 100% safe when held by a third-party custodian.

For me, the security and certainty of having control and access over my own digital assets is paramount. It’s my failsafe against a financial system that’s increasingly unreliable, unfit and unpredictable.

Oh, and on the MtGox thing: all the MtGox bitcoin has now been distributed. And guess what? Plenty of us aren’t selling. That now means all the “sell pressure” from the German government offloading bitcoin, the fear around a huge dump of bitcoin to market from MtGox distributions… that’s all over.

Add to the mix the possibility that in a week Trump may announce he’s planning a US strategic reserve of bitcoin and for me the tailwinds coming are significant. I also expect that within the next month bitcoin is going to charge on to new all-time highs and beyond.

The second half of 2024 is going to be fun in crypto!

What else we’ve been looking at this month

James:

World’s largest solar plant featuring over 5 million panels switches on

A Chinese state-owned company just opened the world’s largest solar power plant.

Spread out across a 32,947-acre site in a desert region in the Xinjiang region in western China, the Midong solar project features more than 5.26 million PV panels of 650W each, for a total of 3.5 GW.

As well as the huge number of panels, the extensive infrastructure of the project includes the installation of 1.23 million supporting piles, five 220 kV booster stations, and more than 208 km of transmission lines connecting the array to the grid via a 750 kV substation.

The project will generate just over 6.09 terawatt hours of electricity each year – enough to power the country of Papua New Guinea for a year, though admittedly less than a tenth of 1% of China’s electricity demand.

The developer – a subsidiary of the China Green Development Investment Group – is a state-owned outfit with wind and/or solar projects in 12 provinces, according to the organisation’s website.

The project cost CNY 15.45 billion (US$2.13 billion) to build, a large outright sum to be sure, but equivalent to $0.61/watt all-in – which is actually cheap at the price. Indeed, the cost per kWh will probably fall under 2 cents per kWh, though that could double with the addition of batteries that allow solar to be discharged when the sun isn’t shining.

Of course, big solar farms such as this one tend to be located far from centres of electricity demand because of poor land availability in Chinese industrial areas. This means a growing need for expensive, long-distance transmission links.

But if you want to get a sense of what 5 million PV panels look like, then check out this video by Blue C Energy. As well as a few still images of the project, the video explains just how and why China is leading the charge in solar energy.

Indeed, China also recently announced plans for a new behemoth 8 GW solar farm in inner Mongolia as part of an $11 billion integrated energy project led by state-owned power company China Three Gorges Renewables Group – which, if built, will easily take Midong’s position as the largest solar plant on the planet.

The inside story of how Europe’s rocket programme lost big to Elon Musk

Earlier this month, Europe’s big new rocket, Ariane-6, blasted off on its maiden flight.

The vehicle set off from a launchpad in French Guiana on a demonstration mission to put a clutch of satellites in orbit.

According to reports, crews on the ground in Kourou applauded as the rocket soared into the sky.

Ariane-6, which already has a backlog of launch contracts, is intended to be a workhorse rocket that gives European governments and companies access to space independently from the rest of the world.

But worries persist that its design could limit future prospects.

Indeed, even though nearly €6 billion in subsidies have been pumped into the Ariane-6 programme, there seems little chance of it ever defeating Elon Musk’s SpaceX.

In fact, the best case is that it offers a way for Europe’s satellites to reach orbit without having to pay Musk – but at a premium price.

To find out what went wrong, you should read this excellent article by Politico that explains just how Europe’s rocket programme lost out to SpaceX.

As the article explains, in its heyday, Europe’s Ariane programme was a global workhorse for commercial and institutional missions into space but now it seems just another reminder of a continent that once led the world with speedy TGV trains and Concorde supersonic planes.

“Expensive, delayed and no longer cutting-edge tech,” says Politico.

“That description applies to Ariane 6 but also to swaths of Europe’s economy, with companies giving ground on solar panels, battery cells, electric vehicles, wind turbines and microchips to Asian and American rivals.”

It’s sad to say but Europe, in the realms of industry innovation at least, is quickly losing ground to the US and China.

This video shows that crude oil tanker

It’s not often you get to see an uncrewed surface vessel make a direct hit on a crude oil tanker, but that’s what you can see in this piece of propaganda released by the Houthis of Yemen.

The remarkable video shows their attack against the oil tanker MT Chios Lion, a Liberian-flagged, Marshall Islands-owned, Greek-operated crude oil tanker in the Red Sea.

The Houthi group has been targeting shipping in the Red Sea and Gulf of Aden over the last nine months, claiming its actions are in direct response to Israel’s war on Hamas in Gaza.

The latest attack, which took place on 16 July, was against a tanker transporting 100,000 tonnes of crude oil from Tuapse in Russia.

Although the tanker was damaged, luckily no injuries were reported. But it’s clear these continue to be scary times for tankers in the Red Sea.

Sam:

Zuck opens the doors, quite literally

There’s an age-old theory in investing that one of the value factors when assessing a company is its moat.

That means what protection it has against competitors and adversaries regarding its service or products.

A strong, wide moat means the company is well protected so that it and only it can properly commercially benefit from whatever it is that it does.

And you can see how a moat is valuable to a company, particularly if it’s in a highly competitive industry and it has something special no one else can do.

These protections are usually in the form of IP, patents and a whole bunch of legal hurdles that cannot and shall not be crossed through fear of litigation.

But then, some companies are coming around to the idea that protection of IP at all costs might be counterproductive to their success. And that releasing the shackles of IP and patent protection and open sourcing their protected materials might end up helping them be more profitable and successful.

Over the years we’ve seen that start to gather momentum. From a company like Toyota in 2015 deciding to open source and release all its hydrogen patents, to Tesla saying it wouldn’t take any legal action against anyone who used its patents and technology in good faith.

Then just this week, Mark Zuckerberg from Meta released a wide-reaching statement on the open sourcing of AI and what Meta is doing in order to progress its own company and AI in general in the long term.

It’s a great read and gives some insight as to Meta’s approach to its technologies and its AI advantage. The cynics might say but it’s just to line Zuckerberg’s own pockets, and maybe that’s the case. But if more companies open-source their tech, maybe it leads to a more profitable and prosperous world all round.

Trump tells… the TRUTH?!

Remember before Trump was shot, where he had that debate on CNN with Joe Biden? And that debate was essentially the beginning of the end for Biden’s presidency and potential second term?

In that (quite garbage) debate they both had a little childish argument about their golf handicaps and their abilities or lack thereof in the game of golf.

Loads of people thought they were both significantly extending the truth about their skills on the course.

So when one of the world’s leading golfers, current US Open champion and YouTube sensation Bryson DeChambeau, invited them both to take part in a series he does on his YouTube channel called “Break 50” only one of the presidents actually took him up on it, Trump.

Biden declined.

You should see this for yourself.

Yes, Trump’s golf swing is not conventional. Yes, his putting stroke is something that can only be seen to be believed.

But I will tell you this now. He’s bloody good at golf. And Bryson’s video of “Break 50 with Trump” proves it.

James Allen and Sam Volkering

Editors, Southbank Growth Advantage