Your June issue of Southbank Growth Advantage

27th June 2024 |

- 300 years, 3 miles and £132 billion of British genius

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

300 years, 3 miles and £132 billion of British genius

Philosophiæ Naturalis Principia Mathematica (Principia) is one of the most important scientific works ever.

It is the work of Sir Isaac Newton, published in 1687 which lay the foundations for classical mechanics, mathematics, physics and science.

When Newton wrote this seminal works he was a professor at Trinity College, Cambridge, England.

Source: Google Maps

You can see Trinity College in the Google Maps screenshot above.

Newton is arguably the greatest British inventor and scientific mind there’s ever been in terms of impact on our world. If there were to be a name that perhaps would come close, it would be that of Stephen Hawking.

But it should also come as no surprise that Hawking too did his most impactful work at the very same location, right in the middle of Cambridge and even held the same position as Newton, Lucasian Professor of Mathematics.

So, there’s at least two of the greatest scientific minds in history that you can trace right back to the quaint and beautiful city of Cambridge in the English countryside.

What if we told you there was a third though?

A name that arrives almost exactly 300 years after Newton walked the ground at Trinity College. A name that you probably don’t often associate as being as impactful on science and our world as you do Newton or Hawking.

But arguably a name that’s just as (if not more) important than both…

In fact, if you jump on a bike, in about 18 to 20 minutes just three miles down the road from where Newton and Hawking toiled away, you’ll find this building,

This is one building of several that occupy a large technology park just down the road from Trinity College. This isn’t a college per se, but it is part of a large technology park… a different kind of campus.

And it’s here that you’ll find the future of the United Kingdom. The epicentre of Great British innovation, science and technology. The engine room for British economic growth and Britain’s chance to again be a commander of global markets.

In these buildings is over 45 years of the world’s most important innovation, invention and scientific discovery that is the cornerstone of the world we live in today.

Newton… Hawking… this company.

In our view it should be held in the same regard. And it’s this company at the centre of Great British innovation that we think also is at the centre of our future, and the most exciting British company for investors in the world today.

To understand exactly how important though, let us wind back the clock to the 1980s.

A computer in every classroom

In the 1980s the BBC explored the new and exciting world of personal computers with a programme they called The Computer Literacy Project.

The aim was very simple: to help people, and more specifically children, understand, learn and explore the world of computers. This all came about after Dr Christopher Evans hosted and produced an ITV documentary that became very popular called The Mighty Micro.

Source: YouTube

In this Evans predicts the rise of the computer revolution

“We’re on the brink of the computer revolution. It’ll run its course not in a century but in one or two decades. It’s an era when well amplify the power of our brains many, many times in the way that the machines of 100 years ago amplified the power of our muscles.”

He talks about microprocessors and how people know what they are, but not how impactful they’ll be. It’s well worth a watch as it very accurately looks at how our world will change thanks to these tiny technologies.

Thanks to this documentary and the insight it gave, the BBC took a far greater interest in programmes related to computers and the future of microprocessors.

The BBC went on to produce 267 programmes for viewing, and has a complete archive of clips, shows and information that you can still view today (here if you’re interested).

Part of this project was also the commissioning of a new kind of computer it called the BBC Microcomputer System, or just BBC Micro for short. The aim was to get a BBC Micro into every classroom in the UK.

Source: Microbit.org

Maybe you were at school when these hit the market and hit the schools. We’d love to hear from you about your memories and experiences with these if you’d take the time to write in and let us know.

The BBC Micro was designed to allow kids to learn about programming and information which was then broadcast in the BBC programmes, providing a connection between the work at school and then the shows broadcast in the home.

The BBC Micro was built by a small start-up computer company called Acorn which was founded by Chris Curry and Hermann Hauser. Its offices were based in Cambridge, where Hauser had received his PhD in 1977.

This little company was originally contracted to deliver 12,000 BBC Micros by 1982.

However by 1982 Acorn had sold more than 24,000. And by the time the BBC Micro’s lifespan ended in 1994, over 1.5 million had been sold across the UK and Europe.

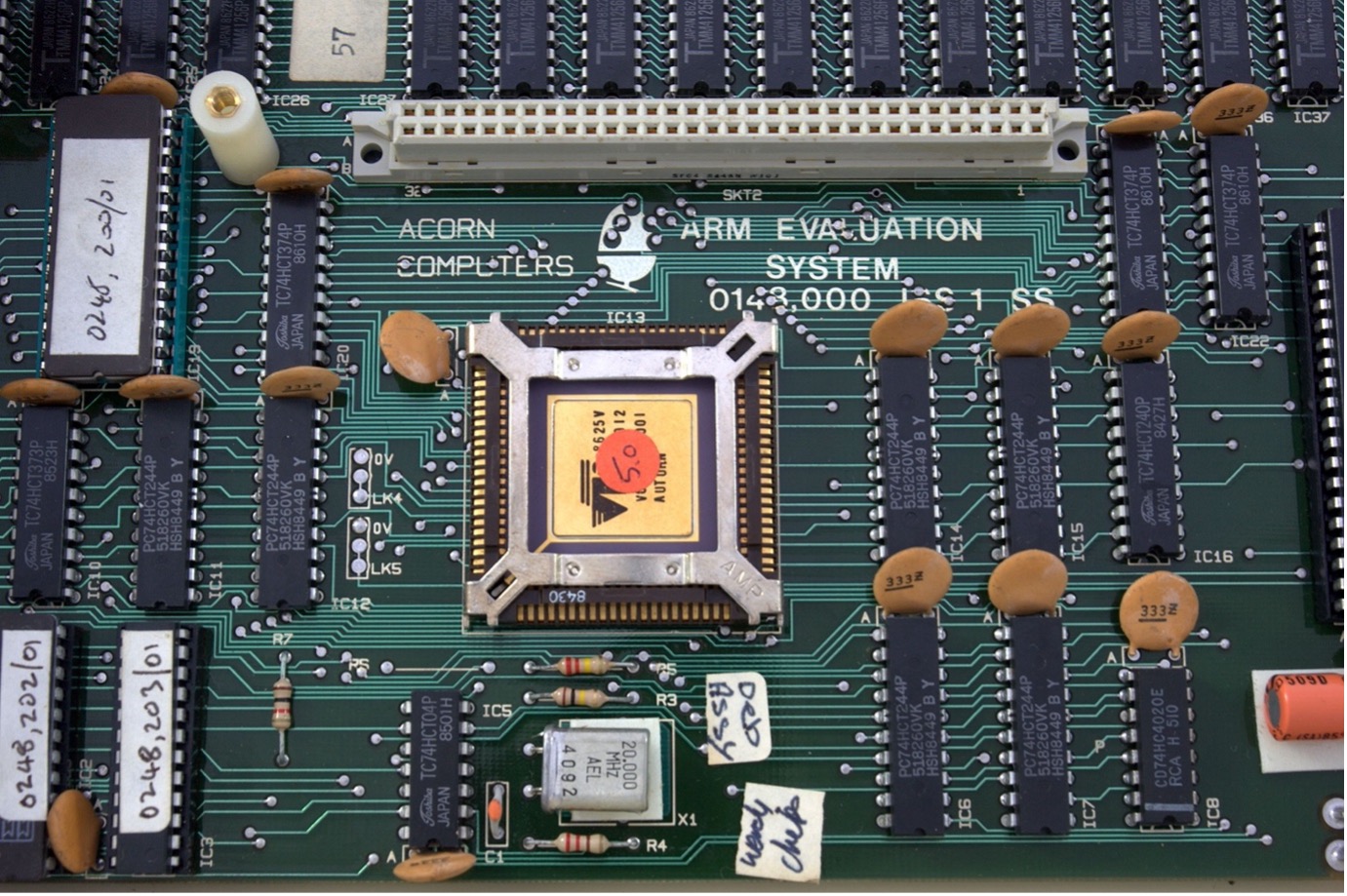

Acorn was also developing its own “chips” for these computers. You can see one of its early chips used in the BBC Micro here:

Source: Wikipedia Creative Commons – “Peter Howkins” – Own work

The name of this chip was the ARM1.

The success of BCC Micro of course meant that Acorn would go on to produce another microcomputer, the successor to the BBC Micro.

This would be known as the Acorn RISC Machine Archimedes. Or the ARM Archimedes.

And again Acorn was now in full development of its own architecture and designs for the chips to be used in these computers, including the ARM2.

However nothing quite led to the initial success and heights of the BBC Micro. And by the end of the 1980s, Acorn reached a fork in the road and made a decision that will forever go down in history.

In 1990 Acorn spun out a separate company called Advanced RISC Machines (ARM). By now Arm technology was widely recognised as being at the forefront of chip design. Which led to a company called Apple getting involved with Arm.

And over the next decade Arm would closely work on chip design and licences to companies, like Apple for its computers and notably smaller handheld devices like the 1997 Apple Newton personal digital assistant (PDA) device – the forefather of the iPhone.

Such was the growing success of Arm’s chips that by 2005 as the explosion of mobile phones gripped the world it’s estimated that 98% of all mobile phones sold worldwide had at least one Arm processor in them.

And you’ve probably figured out by now that the company in focus today, and your latest recommendation here at Southbank Growth Advantage, is Arm Holdings Plc (NASDAQ:ARM).

The greatest British company in history?

Quickly, grab your smartphone wherever it might be.

Or maybe if you’re reading this on your smartphone, it’s already in your hand.

What you are holding right now (your smartphone) is much, much more than what you might think. It is literally artificial intelligence in your hand.

It doesn’t matter if you’re holding an Android operating system phone, or an iPhone, or some other Chinese spy phone with another operating system (just kidding… or am we?).

Most likely it will have a function in there where you can just “ask” Siri/Alexa/Google/President Xi any question you like and it will try find an answer.

Most people don’t think of all this as “AI” but the truth is it’s a form of machine learning that pulls on data from the internet, the cloud and data centres to find an answer to your question.

If you’re on a computer too, you’re probably running Microsoft Office, or you’ve got Dropbox, or use Slack for work.

All of these applications and devices now integrate AI in one form or another.

AI is everywhere already and most people are truly yet to wake up to exactly what that means, and, importantly, how it works and who profits from the AI boom.

Much like the early-to-mid 2000s, there’s a pretty good chance that your smartphone has Arm technology inside. If you’re running anything Apple, that chance is even greater. And if you’re on a device that uses any of Apple’s M-series chips, M1, M2, M3 or the latest M4, then its 100% guaranteed that you’re packing Arm there under the hood.

When Apple recently announced its move into AI, it noted that “Apple Intelligence” would only be available on “Apple silicon” – namely its A17 Pro and M-Series chips.

Source: Apple WWDC24 livestream on YouTube

As Sam recently explained in an edition of AI Collision:

… what is Apple silicon? Let me try to break it down for you…

The Apple M series chips, including the M1, M1 Pro, M1 Max, M1 Ultra and M2, are Apple’s “custom” silicon designed specifically for its Macs and iPads.

These chips are thanks to detailed engineering from Apple’s in-house teams but they also very much rely on Arm architecture and advanced manufacturing processes from TSMC.

Apple’s M series chips are based on ARM (NASDAQ:ARM) architecture, specifically ARMv8 and ARMv9. ARM provides the architecture and design blueprints for these processors that are widely recognised for their high efficiency and low power consumption.

That makes them ideal for devices like iPads, iPhones, and compact devices like Macs and MacBook.

Apple licenses the Arm architecture and that’s when it takes it in-house, and designs its own custom CPU and GPU cores based off ARM tech. This means that while Apple uses Arm’s architecture as a starting point, the final design and performance characteristics of the M series chips are unique to Apple.

Not only is this the perfect example of how a company like Arm generates their revenues, but it also shows just how important Arm is to the rollout of AI technology.

But it’s not just Apple that’s reliant on Arm, and not just smartphones that Arm is suited for.

Microsoft is pushing forward on its next lineup of PCs that will all be branded with Copilot+.

This means Microsoft PCs will be inbuilt with its AI, Copilot, and even have a dedicated Copilot button on the keyboard to quickly and easily call up their AI to help you with things.

And what is the chip architecture that these will all be based off? Yes, it’s Arm.

This is the integration of AI into our lives in a very easy and seamless way that we’ve been writing about for several years now. And interestingly what we’re seeing develop today is very much like those early days of the BBC Micro, in that at the core of all this are the “chips” enabling this future to take place.

And with these Microsoft AI PS, with Apple’s “Intelligence” and like the BBC Micro, it is Arm technology that is the heartbeat of it all. Qualcomm, Samsung, Apple and Microsoft are just some of the big names that lean on Arm for their existence.But there’s one more that maybe even isn’t the company it is today without the backbone of Arm tech behind it.

The failed Nvidia takeover

Nvidia has long been a partner of Arm. In fact, its Tegra chips were all Arm based. Tegra has been used in the automotive industry for decades now. You’d be hard pressed to find a car on the road today that doesn’t pack some form of Nvidia Tegra kit in it, which is all based on Arm system-on-a-chip (Soc) technology.

More recently Nvidia’s Grace CPU, a key piece of technology for their datacentres and rollout of AI into datacentres, and their first ever data-centre-specific CPU, is again all based on Arm.

The rumours are that by the end of the year another new Arm-based chip it dubs “Blackhawk” will come out and combine with Nvidia’s Blackwell GPUs for the most cutting-edge chip set for our AI-enabled world to date.

In short, Nvidia and Arm go hand in hand.

So much so that in 2020, Nvidia announced its intent to acquire Arm Holdings from SoftBank for $40 billion (Arm wasn’t listed at this point, but owned by Softbank).

The proposed acquisition raised significant concerns among Arm’s customers and competitors, as it would have given Nvidia control over critical technology used by many of Arm’s rivals.

Regulatory hurdles and opposition from multiple quarters, including companies like Qualcomm, Microsoft and Tesla (Elon was quite vocal in his disapproval of the deal), meant that ultimately the deal stalled, and then in 2021 collapsed.

But here’s the thing. If a company like Nvidia was hell bent on buying up Arm, right in the midst of its own strategy pushing hard down the AI chip pathway, clearly it saw something and knew something that the rest of the world didn’t.

Then again, for 40-odd years Arm has been at the pinnacle of microprocessors, semiconductors and the latest in high-performance technology. There’s no indication that this British company that exists right in the heart of this country and is a global powerhouse of technology is reversing gear any time soon.

In fact, we expect that even with an eye-watering valuation of $160 billion that Arm is on track to become the first British company in history to reach a valuation of $1 trillion.

The path to $1 trillion

When you’ve got a roll call of customers like Microsoft, Apple, Qualcomm and even Nvidia, it’s fair to say you’re a critical piece of the world’s technology puzzle.

As we continue down this path of AI technology rollout, increasingly the news flow on next generation chips indicates that much of it is going to be thanks to Arm.

But as I say, it comes with an eye-watering valuation already.

At a market cap of $172 billion and at a price-to-earnings ratio of 550, there’s plenty of sceptics that suggest ARM is already grossly overvalued.

From a purely quantitative perspective, that might very well be the case. And you should factor in that risk when considering buying the stock or not.

They might be right. That based purely on the value analysis of the company and its financial position on current earnings, it’s pricey.

But that’s not what we’re basing our judgement on here entirety. Yes, that’s a factor, and it should be noted that for the full year 2024 (ending 31 March 2024) it reported net income of $306 million.

It’s easy to do the maths on that to see the 550-times earning and $172 billion valuation being hard to absorb. But our expectations are that investing in Arm is not all that different to investing in Nvidia four or five years ago, coincidentally enough around when Nvidia itself was trying to buy Arm.

And we guarantee you this: when Nvidia was a $168 billion company back then, the idea of a $1 trillion valuation and then some was well off the radar too. But the speed in which AI technology is not just rolling out, but also developing, we don’t think is yet fully appreciated by the market and investors.

While Arm might not be exactly the same kind of company, our experience indicates that it carries the same kind of hallmarks that Nvidia has going back a few years.

Namely that it’s often overlooked and it’s not very well understood unless you’re either involved in the industry or have a long-standing history of understanding the company. Investors take a cursory look at it and just assume it’s overvalued. But then when you’re able to see its importance in the future of technology and high-performance computing, you can see demand for its tech isn’t going away.

We also believe you can draw a parallel with Nvidia. Demand for Nvidia chips is only heading north, and its next generations of chips will improve on what is already a wide technology moat. That’s all based heavily on Arm as well. We expect that Arm will ride the Nvidia coattails and continue to increase revenues, increase royalties and increase its net profits, plus smash analyst expectations as it’s repeatedly done over the last year – just as Nvidia has done year on year for the last few years.

Add the fact Nvidia is just one customer, and the likes of Apple and Microsoft and their involvement is only getting deeper, and for us, Arm is and should be the cornerstone of any British investor’s portfolio for the long term.

We’d go so far to call it the greatest British company in history and as we say above, quite possibly it could be the first to reach a trillion-dollar valuation over the next five years.

Risks

As we’ve seen, from a purely quantitative aspect, Arm looks overvalued. We don’t see it that way, but the market can move the stock price harder than our views can.

We’ve seen with Nvidia what a dash of negative sentiment can do to a valuation in a short space of time, wiping billions off valuations.

Arm is not immune to this. Should the AI train decide to park itself at a station for a while, or at least the excitement around the investment theme taper off, we would expect a period of Arm’s stock price trading sideways, and quite possibly lower back towards the $100 mark.

Furthermore, in the last year Arm’s stock price has tripled. Yes, it’s already shot out the gates, after listing on the Nasdaq in 2023 after a long and drawn-out highly anticipated IPO.

You see Arm used to be traded on the London Stock Exchange. Remember, it spun out of Acorn in the 90s. It also listed on the LSE. It would go on to then be taken private and owned by Japanese conglomerate Softbank. That also led to the attempted Nvidia buyout.

But with that thwarted, and Softbank wanting to cash in some chips (long story there for another day), Arm listed on the Nasdaq.

And it’s gone from strength to strength since. Partially because of the rise in AI and also because of its long-standing and highly impressive customer base. And also a little bit because Nvidia itself has disclosed it owns around $150 million worth of Arm now anyway.

Is a future Nvidia takeover on the cards? Probably not. It would be tough to get it past regulators. But it does prove that Nvidia and Arm are stitched together seemingly for the long term.

But that comes with risk too. Maybe Nvidia’s tech gets caught up to by the likes of AMD? Maybe it divests its stake in Arm?

Maybe an Arm competitor, like Intel, ups their game and starts to become more relevant again? We must also consider that Arm, as important as it is, is a direct competitor with Intel.

And Intel has long-standing relationships with big tech and is a key supplier of chip technology to the world. We don’t see Intel leapfrogging Arm, not now anyway. And while AMD might catch up to Nvidia, we also don’t see a leapfrog taking place.

But it must be considered we can be wrong, and that both competition and technology risk come into play here, which could adversely impact Arm’s stock price.

Buying instructions

Risks considered and understanding Arm’s history and deep involvement in the future of AI and future technologies to be rolled out by the world’s leading big tech companies, we think long term Arm is a company to hold in your portfolio.

It is inherently British, one of the country’s greatest success stories that is often overlooked as important to Britain and the world, but yet is as important as names like Newton and Hawking are.

Action to take: BUY Arm Holdings (NASDAQ:ARM). Arm trades with a current price of $161.82. Buy up to $175. Set a stop loss position at $80.

Big Breakthroughs

James:

Here’s a breakthrough of sorts: seven Chinese solar companies most people haven’t heard of are alreadyproviding more usable energy for the global economy than Exxon, Chevron, Shell, BP and the rest of the so-called Seven Sisters that once dominated oil production.

That’s according to a blockbuster analysis released earlier this month by Bloomberg anyway.

The financial news and analysis firm reached the headline conclusion by converting the barrels of crude and cubic metres of gas produced by the big petroleum companies into a measure of energy – exajoules.

While one exajoule of electricity would be able to power Australia, Italy or Taiwan for a year, the biggest seven oil giants – Exxon, Chevron, Shell, TotalEnergies, BP, ConocoPhillips and Eni – extract around 40 exajoules of petroleum energy from the ground per year, or just shy of 18 million barrels per day.

That’s a lot of energy, make no mistake, and certainly more than the five-ish exajoules of electricity produced by the solar panel output of China’s seven largest solar companies: Tongwei Co, GCL Technology Holdings Ltd, Xinte Energy Co, Longi Green Energy Technology Co, Trina Solar Co, JA Solar Technology Co, and Jinko Solar Co.

But here’s the thing: the vast majority of the exajoules produced by the big petroleum companies is wasted, mostly as heat.

In fact, only about a fifth of the chemical energy in freshly pumped crude ends up being turned into kinetic energy moving cars and trucks because oil refineries and vehicle engines fritter most of it away as useless heat and noise, according to the Bloomberg analysis.

Gas turbines are a bit more efficient at turning methane into power but still end up operating at about one third efficiency once you account for losses from gas well to electrical socket. As a rough estimate, only about a quarter of the energy coming out of an oil company’s wells gets turned into useful power.

But this still isn’t the whole story.

Bloomberg looked at the energy that each group of producers can deliver before their current capital investments wear out – in the ten years or so before an oilfield depletes, or the decades before the manufacturing equipment in a solar plant wears out or becomes obsolete.

On that basis, Bloomberg says, “clean power moves clearly into the lead,” with seven solar companies showing up among the top ten producers and four big oil and gas companies – Shell, ConocoPhillips, BP, and Eni – coming in last.

But, again, there’s more to it than that.

You see, according to Bloomberg, these figures still don’t account for the lifetime energy production of a solar panel, just simply what it makes in a year. Most modern solar panels carry a 25-year warranty, meaning that they will be generating electricity for decades, while oil and gas sold this year will be used within a month or two and then it’s gone forever.

On that time scale, the seven top solar companies generate 110 exajoules of energy, compared to a mere 24 across the seven oil and gas giants, Bloomberg states.

In fact, Bloomberg found that the panels produced by Tongwei alone in 2024 will contribute around 27 exajoules of electricity to the grid, while the oil and gas pulled out of the ground by Exxon this year will account for a mere six exajoules.

Put another way, all seven of the biggest petroleum producers combined will contribute less energy from their products this year than just Tongwei’s long-tail solar production.

Yes, solar is intermittent but the calculations here assumed a 17% solar capacity factor. That compares to 20% well-to-wheel efficiency assumption for crude and 38% well-to-wire for gas.

Meanwhile, MBOE (one thousand barrels of oil equivalent) reserves efficiency is estimated at 25%. Panel efficiency loss is accounted for by assuming solar panels have an operating life of 22 years, lower than the typical 25-year warranty to account for 1% degradation per year.

These changes amount to “a remarkable shift,” says Bloomberg journalist David Fickling.

“Around the middle of the 20th century, the predecessors of the major international oil companies attained such power that they were nicknamed the Seven Sisters, a group of energy producers with such global scope and influence that they could make or break governments.”

While many of them are still trying very hard to do that, “seven Chinese companies have a bigger stake in the power source of the 21st century than the Seven Sisters of oil that dominated the 20th,” he notes.

That shift helps explain the “geopolitical angst” surrounding the meteoric growth of clean technology in China, he adds.

Of course, any comparison between oil and solar can be criticised for comparing apples with oranges.

Certainly, the big difference between what’s in this particular fruit basket is that oil and gas are both storable and dispatchable, while solar isn’t. Furthermore, petroleum’s chemical uses, which are increasingly a larger part of the barrel, are a lot harder to displace than its energy uses.

It goes without saying that this is not a perfect comparison between oil & gas and solar because, as Fickling himself states, it is comparing the lifetime output of a year’s production of capital goods (solar panels) with the lifetime output of a stock of consumable goods (petroleum reserves).

But, that said, it’s still worthwhile to think about the utilisable energy that an existing stock of investments will produce over their useful lives, and this is what this analysis shows.

In any case, if the numbers are to be believed, then they certainly say this: the oil age is ending faster than many people realise.

Buy List update

European Metals Holdings (AIM: EMH)

At the time of writing, European Metals Holdings is trading around £14.11, having shed over 30% over the last month, with the stock now 57% down in the model portfolio.

European Metals part owns the Cinovec lithium asset in the Czech Republic, one of very few advanced-stage, large-scale lithium projects in the European Union with a mineral resource of nearly 7.4 million tonnes of contained lithium carbonate equivalent.

The project is being developed by Geomet, a joint venture between EMH and Czech-state-owned CEZ.

In the absence of news, the market is likely losing patience with the ongoing delay of the publication of a definitive feasibility study (DFS) for the Cinovec.

Originally slated for release in the first quarter, the DFS delivery has been postponed owing to continued engineering work and social and environmental engagement efforts. According to the company, these efforts have unearthed potential improvements to the lithium processing component of the study.

In particular, EMH announced it resolved to improve the location of its lithium processing plant to the Prunéřov site.

Although the revised location has had an effect on the timing of the DFS, the company has said the change is expected to have a positive outcome on the capex and opex per tonne of the project.

In late April, the company said EMH’s advisers will commence finalising the DFS process taking into account the new site.

However, we still don’t know exactly when the process will be completed.

Ongoing weakness in lithium prices is undoubtedly pressuring EMH shares, too, with spot prices of lithium carbonate in China sliding to the lowest since August 2021 amid concerns over a glut and slowing demand growth.

Although prices stabilised earlier this year, the supply-chain is still working to clear inventories, resulting in customers holding off purchases. The bearish sentiment has wreaked havoc on the stock prices of most producers, including Albemarle and Piedmont Lithium.

However, for EMH, specifically, there is much to remain optimistic about, especially as the EU’s Critical Raw Materials Act (CRMA) has now entered force.

As well as legislating for shorter and simplified permitting processes for European critical raw materials extraction projects, the CRMA provides the framework for the designation by the European Commission and member States of projects deemed “strategic projects”.

Such designated projects will receive political and financial support to enable the projects to reach production in the shortest timeframes possible, helping to afford the EU a degree of critical raw materials independence whilst contributing to the green transition.

As Europe’s largest hard-rock lithium mining and processing project, the Cinovec project is applying for – and is expected to receive – strategic project designation under the CRMA. This could arrive later this year.

Remember, the project has already been granted strategic process status under the EU’s Just Transition Fund.

The stock remains a BUY below its 45p buy limit.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF has fallen by 9% over the month to trade last at around £5.65 at the time of writing, putting it around 37% below our £8.96 entry price.

LITG has significant positions across different parts of the lithium supply chain, from mining and refining the metal, through battery production. It seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Global Lithium Index.

By owning mining, refinery and battery production companies in the fund, Global X has its fingers in multiple parts of the lithium industry.

Of course, the ETF benefits from the surging demand for the silvery-white metal from electric vehicle (EV), renewable energy storage and mobile device industries.

However, increasing supply of the white metal, particularly in the China market, has caused lithium prices to fall since hitting record highs in 2022.

However, once lithium inventories clear, we should see prices pick up.

With the ETF providing easy access to a secular growth trend that’s nowhere near ending, LITG remains core position in the Southbank Growth Advantage portfolio.

Central Asia Metals (AIM: CAML)

Central Asia Metals (AIM: CAML), a mining company with operations in Kazakhstan and North Macedonia, has fallen 9% over the last month to 202p at the time of writing, still leaving it 27% underwater in the model portfolio.

The group’s principal business activities are the production of copper at its Kounrad operations in Kazakhstan and the production of lead, zinc, and silver at its Sasa operations in North Macedonia.

The stock has likely fallen in line with weaker copper prices, which have dropped around 13% from last month’s record highs of $11,100 a tonne.

Although copper prices are still relatively high, Chinese buyers are contending with stalling property and industrial sectors, likely resulting in deferred purchases. As a result, warehouses in the country are full of unsold copper, marking the biggest surplus in four years.

However, Central Asia Metals still looks good value, with City analysts expecting earnings will soar 27% year on year in 2024.

This means the company is trading on a forward price-to-earnings (P/E) ratio of around 10 times. At the same time, a price-to-earnings growth (PEG) ratio of 0.4 suggests the share is undervalued.

Finally, Central Asia Metals carries a huge 8.2% dividend yield for 2024.

Of course, the miner’s bright earnings forecasts are underpinned by a strong outlook for copper prices given favourable demand and supply dynamics.

With its ultra-low-cost operations, CAML could certainly thrive in the years ahead.

As such, CAML is a BUY under 310p.

Foresight Sustainable Forestry Company (LON: FSF)

Foresight Sustainable Forestry Company, which invests in UK forestry and afforestation assets, has risen 32%over the last month to around 96.06p at the time of writing, putting it around 12% down in the portfolio.

It’s not hard to find the reason for the spike in prices: Foresight Sustainable Forestry’s acceptance of a £167 million offer from a private equity firm Averon Park to take it private.

Management at the forestry investment firm said it was in favour of a £167 million offer from Averon Park, adding that the company will delist immediately after the deal goes through.

Averon Park offered to buy all of FSF’s shares at 97p each.

The deal is expected to complete at some point in the third quarter.

Richard Davidson, FSF’s chairman, welcomed the offer and said he believed it “represents good value for shareholders”.

“The structure of the deal means investors can continue to participate in the compelling investment fundamentals presented by the forestry and carbon credit industries through a private structure,” Davidson said in a statement.

Averon argued that FSF’s public status has hindered its ability to raise additional capital, grow its valuation and improve liquidity.

By taking it private, Averon says it will be able to “allocate further capital” to FSF, positioning it in a better spot “to achieve its growth aspirations… and thereby deliver its environmental potential.”

The stock will remain in the model portfolio until the deal completes, at which point it will be sold at 97p.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation, the world’s largest gold miner, is trading around $41.90, 1% down on the month. The stock remains 36% below our $65.39 entry point.

After completing a $17.14 billion takeover of Newcrest last year, Newmont is now looking to execute on plans to divest eight assets, trim its workforce and cut debt.

Newmont is looking to offload its Eleonore and Musselwhite mines and a development project in Canada, a mine in Colorado in the US and the Akyem mine in Ghana. In Australia, the assets up for sale include the Telfer gold mine and a 70% stake in the Haverion copper-gold project that it owns with Greatland Gold.

The miner in February said it aims to realise over $2 billion in cash from portfolio optimisation with Newcrest and will focus on growing its core assets as part of its transformation strategy.

The company has benefited from a 15%-odd jump in gold prices this year, with gold demand rising largely due to global macroeconomic uncertainty.

Newmont remains a BUY under $100.

Stellantis NV (NYSE: STLA)

We recommended multi-car brand giant Stellantis at $22.84 in our January issue. At the time of writing, its shares are trading at $20.59, putting it 10% down in the model portfolio, after falling 8% over the last month.

The stock reached an all-time high at nearly $30 on 25 March but has since fallen back, in part due to an industry-wide sell-off sparked by concerns over EV demand and more recently on the European Commission’s decision to slap tariffs on imported Chinese EVs.

Some European automakers fear a possible trade war would hurt not only their business in China but also their own imports of Chinese-made cars.

Stellantis has already said it is now looking to shift output of some Chinese-brand electric vehicles to Europe in the latest sign of how carmakers are changing their regional strategy in the aftermath of Brussels’ announcement to apply additional tariffs on Chinese-made EVs of up to 38%.

Stellantis said in May that it would sell EVs from Chinese carmaker Leapmotor at its European dealerships from September.

“A certain number of [Leapmotor] products will have to be assembled in Europe,” Stellantis CEO Carlos Tavares confirmed at Stellantis’s annual meeting in Detroit in mid-June.

Tavares said the tariffs were above levels at which the company had previously agreed it would make sense to import rather than to produce locally.

According to Daniel Schwarz, an automotive analyst at Stifel, Chinese OEMs will likely accelerate their construction of production capacity in the next three years in Europe.

“In [the] short term [tariffs are] a positive for European carmakers, but long-term it’s a negative as they will lead to long-term more investments in Europe by Chinese companies, more capacity and the price pressures will be similar to what we see in China right now,” he said.

Stellantis has long warned that a wave of cheaper Chinese models would outprice European rivals, though Germany’s Mercedes and BMW – which rely much more on the Chinese market – have loudly lobbied against increased protectionism, fearing retaliation from China.

The stock is a BUY while it trades below its buy limit of $23.50.

Prysmian Group (IL: 0NUX)

Prysmian Group, which entered the model portfolio at €48.13 in the March issue, now trades at €57.98, 5% down on the month but still 20% up in the model portfolio.

Earlier this month, the Italian cabling giant said its board of directors had approved the launch of a programme to buy back a maximum of €375 million of its shares. In a statement, Prysmian added that the board also decided to proceed with the early conversion of a €750 million convertible bond due in 2026 into capital.

The buyback programme involves a maximum of 8 million shares, equal to around 3% of the company’s share capital, said Prysmian, adding that it will be implemented from 10 June 2024 until 10 March 2025.

As of 21 June, the company had purchased a total number of. 418,000 shares for a total consideration of just over €24 million.

The stock remains a buy up to €60.

SilverCrest Metals Inc (TSX: SIL)

SilverCrest Metals, recommended in the May issue of Southbank Growth Advantage at C$12.55, has since fallen around 11% to trade last at C$11.14.

The stock has inched lower in line with a fall in silver prices, which have hit a six-week low under C$29 amid a stronger US dollar and Fed officials’ hawkish comments on rate cuts.

Amid a high inflationary environment, the silver and gold miner has chosen to hold precious metals on its balance sheet.

Speaking to the Investing News Network, Chris Ritchie, president of SilverCrest Metals, said the company had paid off all its debt on the Las Chispas operation in Mexico, which went into production about two years ago, so had to decide what to do with the cash it had coming in.

“What we did is we took every single penny we spent from day one, all the way through to the end of the mine – and we assumed inflation in the future years of production,” said Ritchie during the interview.

“And we divided it by the amount of gold and silver we have today. What we came up with was that our total cost, our true cost … was in the neighbourhood of about US$25 an ounce.”

At the time, silver was around US$18 to US$19, and SilverCrest realised that selling its ounces would be locking a loss.

“The fact that we are sitting there digging up real money — money that’s better than the fiat currency – we want to hold it. We want it on our balance sheet.”

The stock remains a BUY up to C$16.

HydrogenOne Capital Growth (LON: HGEN)

HydrogenOne Capital is a tricky company to properly value in the market. While the stock trades at around 52 GBp, in the company’s most recent portfolio and net asset value (NAV) update the NAV per share is 103.56 GBp.

That means the stock price is near on a 50% discount to NAV. So, the question exist, why? Well, what makes it tricky is the value of HydrogenOne is tied up in private companies. Even if the current NAV is worth 103.56 GBp per share, the ability to realise the full value of that is impossible to determine.

While it has great portfolio companies like Sunfire GmbH which accounts for 20.9% of the NAV, the truth is actually realising that the NAV portion only comes when either Sunfire IPOs and HydrogenOne can realise its holdings, or it’s taken over via a merger or buyout again where HydrogenOne can realise the value.

Add to the mix that the industries the portfolio companies operate in are still early stage, and this just makes the risk factors in accessing the full NAV far too high for the stock to trade alongside the estimated NAV.

That’s why it’s at such a discount. However, this is why even though the stock is trading down on the NAV, we expect in the long term for that gap to narrow as value is realised from portfolio companies and new opportunities emerge as well. It should stand to reason that investing in HydrogenOne is a long-term investment and should be viewed and approached as such.

That said, at the current discount to NAV we still do see it as a great opportunity to get access to some exciting, private hydrogen-related companies and potential profit from the HydrogenOne stock.

MPAC Group (LON: MPAC)

After a rocky two years since we first recommended MPAC Group, the stock price has finally returned to breakeven for us. The idea of automation in all forms of the supply chain is a long-term trend that we don’t see disappearing. As a leader in automation technologies in packing and product lines, our expectation is MPAC will continue to grow the company and ultimately the stock price.

There were plenty of times since we first recommended it when it was suggested and considered that exiting the stock was the way to go. However, our investment case behind the company around the implementation of automation and robotics was still sound and there was sufficient indication that the stock could return to where we entered.

It’s now just slightly below our entry, but there’s now continued momentum. We expect a solid 2024 will lift the company higher again and into profit for us. We maintain a buy limit of 525 GBp and stick with the position for a while longer.

Volex (LON: VLX)

Volex is another company in our buy list that’s been around a while. And for most of that time it has been in a loss position.

More recently it has moved into profit because our investment case is now continuing to come to fruition.

When we first wrote about the company in February 2022 we said:

The company is seeking to be the technology bridge between a more interconnected world.

When it comes to electronic products, the company leaves no stone left unturned. Volex manufactures almost any connectivity source you can think of, including power cords, cables, fibre optics, connectors and charging plugs.

These might seem a little boring. However, when you really think about it, these are the critical mechanisms through which our world is powered.

They are the lifeblood of today’s technologies and many nascent, fast-growing industries of the modern day.

These industries include artificial intelligence (AI), medical technology, data networks and, importantly, electric vehicles (EVs).

This was well before the AI boom kicked into overdrive later that year. But the investment case remains. Volex might not be a “sexy” stock, but it’s critical to the ongoing rollout of high technology in our world.

Everything needs power, cabling and connectivity. Volex is the kind of company that makes those things happen. They’re the bolts that are needed to hold up that bridge that you never think about but without, the bridge collapses.

That’s why we liked Volex, and why now the recognition of the quality of company is finally being seen by the market. We stick with the position and expect even bigger things in the short term for the company and stock price.

Inside the lives of James and Sam

Sam:

Take a look at the following picture.

What do you see here?

A big office building?

Correct.

Some gigantic fans or wind turbine things under construction?

Correct.

According to Sawyer Merritt via X.com (renowned Tesla commentator and social media tech pundit) this is“Gigantic fans are now being installed at Giga Texas for Tesla’s new data center cooling system. This new data center will house 50,000 Nvidia GPUs for FSD training.”

And that is really what you see in the pictures.

But that is not what I see. Do you want to know what I see?

Here, I’ll show you.

The image above is an Nvidia GPU (graphics processing unit). These GPUs are the kinds of things that have existed in PCs for decades. These are the “chips” that people often refer to. You’ll find them (and endless variations of them) in servers, in PCs, in gaming rigs, in gaming consoles like PlayStations. When you see this, you are looking at “AI”.

And Nvidia has been at the forefront of development of all this for decades.

This specific GPU while it is an Nvidia GeForce RTX 4090, the rest of it is packaged up and made to look gamer-sexy by ASUS – even more specifically, its Republic of Gamers (ROG) division.

You can pick up a GPU like this for around £2,000.

To me, what Tesla’s data centre is, is just a very, very, very large GPU. And honestly, that’s exactly what it is. The fans on the ROG 4090, they do the same job those big fans will do at Tesla’s data centre.

The hardware underneath the ROG 4090, it’s Nvidia and is (more or less) exactly the same kind of hardware that will be underneath Tesla’s data centre.

I bring all this up because this month, I’ve not been doing much. Well that’s a lie, I’ve been doing normal things, but I’ve been neck-deep in research and working my head around a big idea I’ve been formulating for over a year now.

And today’s recommendation for Arm Holdings is a part of that.

My view is that the next evolution of “chips” like the ROG 4090 is going to be the datacentre-as-a-chip or DaaC for short.

It’s the idea that in order for “chips” to get infinitely faster, they are going to be packed into incrementally larger packages. They will all connect together, operating as one single entity, with gigantic fans and cooling systems, cabling and wireless technologies.

That AI as we know it will be like the ROG 4090 at the scale of the Tesla data centre. And that when we call on AI in whatever guise it may be, we’re just pulling that from a single chip – that just happens to be the size of a small village.

The opportunities that uncovers, from cooling to cabling to energy and even the metals needed for all this are endless.

So as boring as it might sound to most people, this month I’ve just been working on expanding and developing this idea, reading and researching what the next, next, next generation of chips and AI tech is going to look like and connecting a lot of dots to put the puzzle together.

James:

You might not be surprised to hear that I’m a big fan of e-bikes.

Until this week, I was the owner of not just one but two of them: an old beaten-up second-hand e-bike that I use to take my three-year-old daughter to and from nursery, and a much fancier – and more expensive – foldable version (or “foldie” to use the industry lingo) that I use as more of a commuting bike and when I want to whizz around on my own.

The former bike is the proverbial no-frills workhorse but the second one is much fancier and much more enjoyable to ride.

In fact, ever since I bought it back in 2019, it has proved quite simply a brilliant mode of transport, allowing me to accelerate away from all the other non-electric bikes on the road and giving me as much as ten pedal strokes more for my money.

I particularly enjoy dropping the proverbial hammer on the Mamil (middle-aged men in Lycra) brigade on the parks and roads and see them twitch with annoyance as I whizz past in my jeans and jacket.

So you might get a sense of my annoyance and disappointment when I saw this week that our garden shed had been broken into and that my e-bike pride and joy had been pinched, along with my girlfriend’s racing bike. (We store the other e-bike in the house so that escaped the thief’s attention.)

We’re not quite sure when the break-in occurred as we hadn’t actually used these bikes or accessed the shed for around four weeks, but it seems likely it took place not too long before discovery, if some reports on our road’s WhatsApp group are anything to go by.

I’ve been advised to report the theft to the police though I’m not exactly hopeful they’ll catch the culprit or retrieve my bike. I’ll also see what can be done from an insurance perspective so hopefully I don’t lose out too much financially, at least.

But I certainly now need to think if I want to replace the bike.

You see, although I loved my bike, I had started to use it less and less. That’s because, since I bought the bike five years ago, there has been an explosion in e-bike rental schemes such as Lime, Tier, Human Forest and Dott.

I had started to use these rental e-bikes much more than I used my foldie, put it that way.

After all, I don’t have to lug these hire bikes onto the train or worry about securing them and getting them pinched on the street or, yes, at home.

For me, these rental e-bikes are the ultimate urban last-mile solution. And judging by the amount of these power-assisted bikes I see on the roads, many others have reached a similar conclusion.

These modes of transport are small, quick and convenient to move someone around a crowded urban environment – all without the hassle of ownership.

The benefits, of course, are obvious. Previously, the last little leg of the trip to the home or to the office wasn’t always straightforward.

Public transport doesn’t take us exactly where we need to go, while parking is not always available where we exactly need it, meaning owning a car or any kind of vehicle is not always possible or even reasonable.

And, as I’ve found on my commute, walking is not always the quickest or the most convenient way to move around the city.

Instead of walking to and from the train station on my commute, I can instead hire an e-bike from Lime or the like to take me the “last mile” to the office instead. And as it’s an e-bike, the cycle is quick and pretty much effort-free.

So I’m of a mind to not actually replace my fancy foldie e-bike and continue to use the rental bikes instead.

There’s a potential investment in rental e-bikes here too, that’s for sure.

According to Allied Market Research, the global bike rental industry is on the up, rising in value from $2.1 billion in 2021 to $5.32 billion one year later, with a projected growth rate of nearly 20.62% until 2030.

This potentially offers investors a lucrative opportunity to capitalise on what is clearly a burgeoning sector.

Lime alone saw a record setting year for both ride numbers and bookings last year.

Some 156 million trips were taken on Lime’s e-bikes and scooters in 2023, with more than 9.2 million new riders using the platform and a doubling of usage in over 42 of its cities.

Gross bookings jumped 32% to $616 million (£487 million), helping full-year Ebitda reach in excess of $90 million, a more-than 500% year-on-year increase.

Although concerns have been raised over public safety with residents complaining that the devices have been dumped on pavements, this is growth that is certainly hard to ignore.

Although Lime is a private company, it’s rumoured an IPO may not be a too distant prospect.

This could certainly be one to keep an eye on!

My stolen e-bike!

Crypto Corner

Sam:

This week, bitcoin’s price dipped below $60,000.

And boy oh boy did the bears come out to play!

I mean, it’s a huge psychological number, right? We haven’t seen $60,000 forever, right?

Or was it just a bit over a month ago? And then wasn’t it only February when bitcoin was trading at $50,000? And this time last year… where were we at? Oh, that’s right, $30,000.

I even had a friend message me this week and say, “This sell-off it brutal!”

I replied with, “What sell-off?”

Then I chuckled because bitcoin is now 17.3% down from its all-time high just a short four months ago. Had we been 50% down four months after the all-time high… maybe I’d be rethinking where in the cycle we are right now.

But we’re not.

In fact, this kind of consolidation is not all that uncommon during an up cycle. Specially as the market has weathered a pretty full-on attack in the US from the incumbent government.

But now, the tide is turning, the bitcoin ETFs are in full flight and still pulling in capital. The Trump Party (also known as the Republicans) are as pro-crypto (and vocal about it) as any government I’ve seen – since El Salvador that is. And even the Democrats in the US are easing off their attack vectors because they know it’s going to cost them votes (it already has).

We’ve not heard a peep about any of it in the UK, which is nuts really, because if you wanted to get young British voters on side, a pro-crypto stance is an absolute slam dunk.

We do know at least, although not particularly vocal about it in his campaign, that Nigel Farage is pro crypto. We know this because for the last four years we’ve spoken at length with him about it from bitcoin to Ethereum to CBDCs and everything in between.

So at least even if the Tories, Labour, the Lib Dems and all the others won’t say anything about it, you know that Farage is all for an open and positive environment in the UK for crypto and digital assets – and to be fair, Reform UK’s manifesto did single out its opposition to a CBDC (again, none of the others even mentioned it).

That’s a positive at least, in the UK that is. And also, after months and months of frustration at the hands of regulators, there appears like there may be a pathway for us here at Southbank to provide more specific crypto investment recommendations and coverage as well.

I can’t say too much at the moment, but lawyers, compliance teams and a lot of other people have been trying to work their way through the minefield of providing crypto advice services in the UK in a legal, compliant, Financial Conduct Authority-friendly way – and that final destination now appears closer than it has since they decided to crack down hard on the industry in the UK.

Anyway, back to the market. Bitcoin is still holding up strong. In fact, when it dipped, I stacked sats – I bought more, added to the pile, my pile, my kids pile, all piles!

There’s a bunch of news flow suggesting that Germany, the US and the MtGox trustees are dumping bitcoin into the market. Maybe so – granted, I’ve still not seen my MtGox bitcoin hit my Kraken account yet… so we’ll see what happens there.

But the point is the market is holding strong. This base is where we lift off from as selling pressure is absorbed and “degens” around the world keep adding to their sat pile. Just take a look at MicroStrategy as an example of that. It went to raise $500 million to buy more bitcoin and add to its balance sheet.

MicroStrategy ended up raising $800 million and bought a truck ton of it over $60,000! That’s how selling pressure gets absorbed, and why long term if you’re not going to add to your bitcoin holdings, someone else will – and that means less to go around when eventually there is no more to go around.

In short, the market looks good, bitcoin looks good, keep stacking those sats and looking forward to the cycle lifting off into the stratosphere.

What else we’ve been looking at this month

James:

We are creating an entirely new energy system right under our eyes

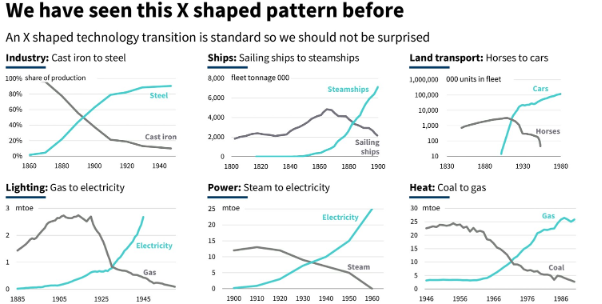

The cleantech revolution – it’s exponential, disruptive and it’s happening right now.

Don’t believe me? Then check out Rocky Mountain Institute’s annual presentation, released earlier this month, that looks in detail at the story for renewables, electrification and efficiency.

There are many nice nuggets in the report, including the charts showing that solar and wind enjoy cost learning curves that fossils simply don’t, allowing the renewable sources to grow faster, but maybe this section is my favourite:

Source: RMI

Let’s call this, well, the power of evidence.

As the RMI states in the report, “new energy comes from manufactured, modular, scalable, clean technologies,” and “design and technologies beat commodities because they enjoy learning curves and are limitless. So, costs fall over time, and growth is exponential.”

Certainly, we all need to wrap our heads around the fact that we are creating an entirely new energy system where decentralisation and demand response are central tenets. While solar and wind will provide the energy, batteries will max out the use of solar and wind while alleviating grid congestion.

If you want to understand the framework driving the clean tech revolution, this report – co-authored by Kingsmill Bond, who has consistently been one of the most prescient analysts on renewables trends – is a definite must-read.

Natural hydrogen is a thing

In December last year, we wrote about a global gold rush underway for a long-overlooked resource that could potentially play a significant role in the shift away from fossil fuels: natural hydrogen, sometimes referred to as white, gold or geologic hydrogen.

As you’ll recall, this refers to hydrogen gas that is found in its natural form beneath the Earth’s surface. It is thought to be produced by high-temperature reactions between water and iron-ich minerals.

Since writing about natural hydrogen, I’ve been keeping a close eye on developments, potentially with a view to making a stock recommendation in Southbank Growth Advantage.

So I was certainly interested to read this month of successful testing in Australia of an exploration well that flowed high purity hydrogen and helium.

The Ramsay project of Gold Hydrogen reported flows to the surface of both hydrogen and helium from drilling on the Yorke Peninsula across St Vincent Gulf from the South Australian capital, Adelaide.

The company said natural hydrogen with purity levels up to 95.8% hydrogen had been encountered across seven zones with the highest purity at a depth of 1,740 feet (531 metres).

“Natural hydrogen and helium flowed to the surface, achieving the primary objective before formation water encroachment impeded further flow testing,” Gold Hydrogen said in a statement filed at the Australian Stock Exchange.

Seismic testing of the company’s large land holdings on the Yorke Peninsula and south of Adelaide is now planned to start soon to help identify future drilling targets.

Without a doubt, this strengthens the case for producing hydrogen from underground reservoirs in the same way natural gas is produced.

Certainly, if natural hydrogen can be produced at a commercial level, and at a reasonable cost, it could imperil plans to manufacture hydrogen via electrolysis – so-called green hydrogen.

We’ll continue to keep you abreast of developments!

Cheapest source of fossil fuel generation is double the cost of utility-scale solar

Earlier this month, US investment firm Lazard released its annual report analysing levelised cost of electricity (LCOE), a critical measure of cost-efficiency of generation sources across technology types.

LCOE measures lifetime costs divided by energy production and calculates the present value of the total cost of building and operating a power plant over an assumed lifetime.

The report, though quite dry in parts, contains the fascinating conclusion that the cheapest source of fossil fuel generation is now nearly double the cost of utility-scale solar.

While the LCOE for solar at the utility-scale has now fallen to $29 to $92 per MWh, coal’s LCOE ranges from $69 to $169 per MWh, according to the report.

However, onshore wind ranked as the lowest source of new-build electricity generation, ranging from $27 to $73 per MWh.

But utility-scale solar has had the most aggressive cost reduction curve of all technologies, falling about 83% since 2009, when new build solar generation had an LCOE of over $350 per MWh.

Meanwhile, natural gas peaker plants are highly inefficient in LCOE, ranging from $110 to $228 per MWh. Nuclear energy had the highest utility-scale LCOE with an average of $182 per MWh.

Of course, LCOE is a far from perfect metric to compare the “cheapness” of generation technologies with very different system characteristics.

To calculate LCOE, Lazard tallies up the expected lifetime electricity generation of proposed power plants and compares them to the costs involved in building and maintaining such facilities.

What it doesn’t do is include additional costs that the power system would have to incur to install and operate the plants themselves. For renewables, these include the cost of grid upgrades, dispatch, storage and backup.

There are plenty of articles online that go into some detail why LCOE is certainly not the perfect metric for renewables, including here, here and here.

My take on LCOE is that it is only ever a starting point to assess any technology or project. System-level analysis also needs to be taken into account, but that’s not perfect either: it is non-transparent, contended and changes over time as systems and demands evolve.

In fact, you might say that LCOE is the only possible starting point for understanding the underlying economics of any technology – but it needs to be supplemented with detailed, technology-neutral, non-partisan work on system costs.

Yes, saying the cheapest source of fossil fuel generation is double the cost of utility-scale solar is a headline grabber. But in this case it’s also true that the headline-grabber – utility-scale solar – is getting cheaper and cheaper each year.

And if you think these conclusions are theoretical and not based in the real world then perhaps also consider recent comments from the CEO of NextEra, one of the largest owners of gas power plants in the US.

When asked earlier this month if gas or renewables will meet the US’s growing electricity demand, NextEra CEO John Ketchum was unequivocal in his answer.

Renewable energy will meet most of the consumption boost because new gas-fired plants are much more expensive, take too long to connect to the grid and have to be supplied by hard-to-build gas pipelines, he said.

Ketchum said that adding battery storage to wind and solar farms can make those carbon-free sources almost as reliable in providing around-the-clock power as fossil fuels are.

“If I want to pay double, I can go with a gas-fired plant,” Ketchum said.

Sam:

The next decade of AI

Situation Awareness. This is an entire site, and massive document if you choose to download it about the future of AI.

It’s written from someone on the inside of the industry, a former OpenAI employee who gets around in San Francisco tech circles. That gives them a unique perspective into what AI is and what it looks like from am more recent standpoint.

It’s in depth, insightful, parts are a little overwhelming, but it’s absolutely worth your time reading this and checking out, as I’ve been doing this month.

You can access the full site (and download links) here.

AI for the grid or the grid for AI?

Amongst some of Southbank’s editors and some of our fellow editors back in Australia from Fat Tail Investment Research, there’s been an email thread about “dirty energy”.

I won’t go into full detail here, but the general take is the energy we do use in the grid is not fit for purpose. There’s a lot more to it than just that, it’s a very big and important idea.

And it’s something where I think we’ll see a lot of development and opportunity coming as we look to new technologies to fix the grid. And a big part of that will be how do we use AI to make our energy better and use it to fix the grid.

Or, perhaps the better question (and the one that’s looked at in this great podcast episode) is how to we remake the grid for AI.

Are we all Soviets?

I don’t like to give away too much when I write these little blurbs for the things we’ve been reading.

And for this one, I’m really not going to give anything away apart from what you see in the subheading above. But this is the kind of varied reading and thinking that I think is important to undertake.

It’s important to consider all takes as controversial and challenging as they might be, whether you agree with them or not. You need to see all sides of the debate to understand your own perspective and viewpoint.

I think humanity has lost a bit of that in recent times, and it’s particularly an issue with younger generations to be able to see all sides in the formulation of a reasoned and critical debate.

That’s why I thoroughly enjoyed this article and something I think asks the right questions, and doesn’t necessarily provide the answers, but at least makes you critically think about the world’s situation – and maybe we are just all Soviets now.

James Allen and Sam Volkering

Editors, Southbank Growth Advantage

{kind=link}