Your October issue of Southbank Growth Advantage

4th November 2024 |

- Big rig nuclear is the key to our next big nuclear star

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

Big rig nuclear is the key to our next big nuclear star

Sam:

I’ve been in Australia now for about a month and a half. One of the things I have really noticed is the size of the trucks on the road.

They are, quite frankly, terrifying.

I got so used to quaint little lorries tottering about the British countryside that I forgot what real TRUCKS are like.

It’s hard to explain until you’re in a car next to one. The big suckers they call “B-doubles” that can stretch as much as 26 metres long, with a main truck, plus two extra trailers, and as many as eight or nine axles. They can carry two 40-foot containers in a cinch and can weigh over 78 tonnes.

Source: Australian Roadtrains

A few times when I’ve been alongside these giants of the road, I’ve wondered what’s inside them. Maybe just big pallets of products heading off to Bunnings (the Australian version of B&Q, but bigger!), maybe building supplies, maybe people (OK, probably not that one). But these things are of a size that you could pretty much put anything you wanted on the back and take it to any part of Australia.

And I do mean any part. If you get a chance (on Channel 5 and Discovery in the UK) try to watch a show called Outback Truckers and you’ll get a much closer flavour of what I’m talking about.

These trucks would be ideal for transporting something like… a small nuclear reactor to a community, city or data centre. As wild as that idea might be, maybe it won’t be too long before I’m pulling alongside a similar sized truck that looks more like this:

While the idea of driving next to a nuclear reactor might seem a touch… risky, the truth is that if this potential future comes to reality, you might have made so much in your portfolio from the company behind it that you won’t be bothered in the slightest.

Your latest recommendation: NANO Nuclear Energy (NASDAQ:NNE)

NANO Nuclear Energy Inc. (NASDAQ:NNE) is a company that’s working on bringing “advanced nuclear technology” to the world. Sure, that’s a bit “buzzwordy” but this is another up-and-coming nuclear company that could prove to be a vital cog in the US nuclear rollout.

I should say at the top that when it comes to nuclear opportunities, I’d love there to be a splattering of ones in the UK, but there isn’t. We’ve pretty much already covered those plays.

There is higher risk development around the technology. It’s all US based because clearly the US wants to a) secure its own reliable energy supply and not rely on Russia or China for anything, b) it desperately needs to help “the Magnificent Seven” fuel their ambitious AI data centre plans.

And that’s where NANO steps right into the mix.

What does NANO Nuclear Energy do?

At its core, NANO Nuclear Energy is all about making nuclear power safer, more efficient, and easier to move around. But there are two key areas (maybe three depending on how you look at it) that I think give this company much more potential to run higher in price.

- Microreactors, or as the company calls them, NANO Reactors

We’re talking here about a reactor that’s small enough to be transported on something like a B-double. NANO has its “ZEUS” and “ODIN” projects. Zeus is referred to as a “solid core battery reactor” and ODIN as a “low pressure coolant reactor”.

- HALEU and HALEU Transport

NANO isn’t just about building reactors; it’s also developing the specialised fuel for these reactors – high-assay low-enriched uranium (HALEU) – and ways to transport this fuel across country.

For me, I think that it could be the HALEU side of the business that provides the most upside potential.

|

What is HALEU? High-assay low-enriched uranium (HALEU) is a type of nuclear fuel that is enriched to a higher level than traditional low-enriched uranium (LEU) but still below the levels used in weapons-grade uranium. Specifically, HALEU is enriched to between 5% and 20% uranium-235 (U-235). This higher enrichment level allows for more efficient and compact reactor designs, making it ideal for advanced reactors that are smaller, more flexible, and less expensive to build and operate. HALEU is crucial for the US because it supports the development and deployment of advanced nuclear reactors. These reactors are expected to play a significant role in the nation’s clean energy future by providing carbon-free electricity. The Energy Act of 2020 directed the establishment of the HALEU Availability Program to ensure a domestic supply of this critical material, reducing reliance on Russian HALEU which traditionally has dominated the market. |

As we covered in our recommendation for Centrus Energy, the US Department of Energy has made a particular point of pushing forward the US development of HALEU fuel for new and high-tech nuclear reactors.

The US cannot meet energy targets and energy demands by building traditional nuclear reactors. Big Tech – like Microsoft, Amazon, Google and Meta – cannot power their AI-enriched data centres waiting for traditional reactors to get built (albeit they’re tapping into whatever existing ones they can).

Google, for example, though has already signed one power purchase agreement from SMR tech through Kairos Power. This is one example of Big Tech already signing up for SMR power, and yet the SMRs aren’t even built…

But they will be.

And they will rely on HALEU fuel. But of course, if there are reactors in Ohio that need HALEU, and then in Michigan that require HALEU and then in South Carolina that require HALEU, you can’t expect a HALEU plant in every US state now, can you?

That’s why the transportation of the fuel is also so important. But it’s not like you can just plop it into some barrels and head on over. No, it requires specialised transportation equipment. And thankfully, as NANO explains,

Through NANO Nuclear Energy Inc., [Advanced Fuel Transportation (AFT) a subsidiary of NANO Nuclear] is the exclusive licensee of a patented high-capacity HALEU fuel transportation basket developed by three major U.S. national nuclear laboratories and funded by the Department of Energy. Assuming development and commercialization, AFT is expected to form part of the only vertically integrated fuel business of its kind in North America.

I believe these factors, and the potential (as they say) of being a fully vertically integrated nuclear fuel business, makes it unique in this market. With ongoing demand for nuclear, it is the perfect stock to add to our buy list.

Potential and risk

The company is cased up, which is why now is a good time to add it to the portfolio. NANO just announced closing an upsized $40 million underwritten offering. This is both crucial money for expansion plans and also a vote of confidence from investors.

I note this “vote of confidence” because the company has been the target of short-seller reports, notably one form Hunterbrook, whose piece titled, “Fission Impossible: Nano Nuclear Has No Revenue, No Products, “Laughable” Timelines, Part-Time Executives, and a $600 Million Market Cap” helped the company on its way down from a high of $34 in July to $6.30 by mid-August.

Since then, the company has employed lawyers to more or less take on Hunterbrook. It’s also added a former commanding general of the US Marine Corp and the former chief financial officer of the US Department of Energy to its Executive Advisory Board. It has also got a grant from the US Department of Energy and of course the substantial capital raise.

The stock price is also now back around $20.

NANO is likely to be a rollercoaster ride. It will ride the nuclear momentum that is currently in the market. When our nuclear stocks like Oklo and Centrus are popping higher, NANO is likely to head in that direction too.

Risks

But as noted, the heat came right out of the market from July to August and the stock tanked. Add to this that it became the target of short-sellers, and the acceleration of sharp moves lower is a real possibility.

You need to be confident and comfortable with that kind of volatility in the stock. As well as the fact that it doesn’t have meaningful revenues. NANO’s August quarterly report (before the $40 million fund raise) had a net loss of $4.6 million. For the nine months ended 30 June it was a net loss of $7.6 million.

Admittedly, it’s not a horrific cash burn for the industry it’s in. NANO is now cashed up again and it’s got plenty of runway here. But again, there is no meaningful income at this point – so this is trading a lot of hope, hype and potential.

But there’s enough there, with support from the US Department of Energy, the development of both its NANO reactors and the HALEU development and transportation. I think there’s a strong case to be made that the company retests and surges past its 52-week (and all-time) highs of $37.51.

We will have a stop exit in place as usual if enough bad news flows through or the short sellers get their way and the stock craters.

Buying instructions

Action to take: buy NANO Nuclear Energy (NASDAQ:NNE). It has a current market cap of around $651 million and a stock price around $20. Buy up to $21. Set a stop exit under the stock at $10.

Be aware that as it’s a smaller stock, not all brokers may offer this for trading. We have checked some of the major brokers, of which some are offering NANO for trade, some do not. We can’t unfortunately ensure that all brokers cover all stocks, and we do try to ensure that there’s sufficient coverage.

Big Breakthroughs

James:

There’s been lots of justified talk – some of it by us – of Big Tech driving a nuclear power revival.

In the last two months, tech giants Amazon, Google and Microsoft have all penned deals to generate more power from nuclear plants in the US, helping to ignite a surge in stock prices in the sector.

Amazon has agreed with utilities in Washington state to support development of four next-generation small modular reactors (SMRs), with a similar deal in Virginia, and took a stake in X-energy, an SMR developer.

Meanwhile, Google agreed to buy power from SMRs to be built by a start-up, Kairos Power. Microsoft has also struck a 20-year agreement with Constellation Energy to restart a reactor at Three Mile Island in Pennsylvania, the site of the most serious nuclear meltdown in US history in 1979.

As you’ll know, the explosive growth of generative AI, as well as cloud storage, has increased tech companies’ electricity demands.

This has generated headlines around the world and helped propel some of our holdings, such as Oklo, to fresh heights.

But what has gone much more under the radar is Big Tech making similar if not bigger investments in renewables to also help power their data centres.

Just last week, a massive solar farm opened in Texas, adding 875 MW of capacity to the state grid to help power Google’s growing data centre presence in the state.

As per the article on E&E News: “The project from California-based SB Energy, named the Orion Solar Belt, includes over 1.3 million solar modules located in Buckholts, Texas, which is about 70 miles north of Austin. To harness the project’s electricity, Google signed its largest-ever solar power purchase agreement.”

This was by no means an isolated deal.

In May, Microsoft struck a landmark deal with Brookfield Asset Management, committing to back an estimated $10 billion in new renewable energy projects to address the ever-growing power demands of AI and data centres.

In fact, so far in 2024, Microsoft has bought 850 MW of new wind and solar just in Texas alone. The Seattle-based tech giant is also buying 12 GW of US-made solar panels from Qcells.

In addition to Microsoft, Brookfield has also announced power purchase agreements with Amazon.

Corporate power purchase agreements covering a record 46 GW of solar and wind capacity were announced in 2023, with Amazon the top purchaser, according to figures published in February by Bloomberg New Energy Finance.

Companies have now signed nearly 200 GW of corporate PPAs in total since 2008, more than the power generation fleets of countries such as the UK, France and South Korea.

You see, while Big Tech is certainly investing in nuclear, they are actually making even larger investments in wind and solar – and have been for years.

Of course, before you ask, they’re certainly aware that solar power doesn’t generate 24/7, but it hardly needs to in places such as Texas.

There is currently an excess capacity at night from wind that sees prices often fall near to zero. So Google, for example, can simply go to the market and purchase all the cheap nighttime power it needs – even before it starts thinking about pairing this abundance of cheap power with batteries.

But, yes, Texas is also building a whopping 30 GW of batteries that will help the grid provide generation when and where the grid needs it, including to power its data centres.

In fact, according to the federal Energy Information Administration (EIA), the US is now adding utility-scale batteries at a dizzying pace. It’s installed more than 20 GW of battery capacity to the electric grid, with 5 GW of this occurring just in the first seven months of this year.

This means that battery storage equivalent to the output of 20 nuclear reactors has been added to America’s electric grids in barely four years. What’s more, the EIA predicts this capacity could double again to 40 GW by 2025 if further planned expansions occur.

In fact, with lithium-ion battery prices falling to their lowest level ever, it’s becoming increasingly clear that we can get a resilient, clean and affordable energy grid with solar, wind, storage and, where required, nuclear too.

What’s interesting is that the E&E News story on X has generated just 250 likes at the time of writing and seemingly wasn’t picked up by the mainstream press at all. This highlights that nuclear – and not renewables – is the current flavour of the month.

But it’s our job to tell you things the mainstream press might not tell you about.

And that is, despite what you have been led to believe elsewhere, Big Tech is not just looking to build AI with nuclear, but with other energy sources, too.

Buy List update

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF has gained by 3% over the month to trade last at around £6.05 at the time of writing, putting it around 32% below our £8.96 entry price.

The ETF allows investors exposure to the lithium and battery sectors.

It seeks to provide returns similar to those of the Solactive Global Lithium Index by holding shares in a broadly diversified cross-section of industries that range from lithium miners to battery producers, all the way to the producers of electric vehicles.

By owning mining, refinery and battery production companies in the fund, Global X has its fingers in multiple parts of the lithium industry.

Of course, battery stocks haven’t fared well for much of 2024, though the ETF gained more than 20% in September after Rio Tinto Group made an approach for Arcadium Lithium Plc.

The fund remains down by 16% year to date at the time of writing.

Lithium stocks have struggled amid excess supplies and tepid demand for the key battery metal used in electric vehicles (EVs). This has seen the lithium prices halve over the past 12 months, leading miners to curtail production.

Just this week, lithium miner Pilbara Minerals said it was suspending output from its Ngungaju processing plant at the Pilgangoora project in Western Australia.

The ongoing slump in lithium prices and the ramp-up of another processing plant at the project caused Pilbarao to place Ngungaju in care and maintenance from 1 December, the company said in a filing on Wednesday.

Pilbara’s decision follows a move by Albemarle in August, when it announced it was shutting half of its processing capacity in Australia and putting expansion plans on hold.

Curtailments such as these should eventually feed through to prices and help lithium and battery stocks regain their mojo. After all, battery demand for EVs is projected to jump tenfold in ten years, according to the International Energy Agency.

However, the ETF remains a HOLD in the portfolio while the market finds its feet.

Central Asia Metals (AIM: CAML)

Central Asia Metals (AIM: CAML), a mining company with operations in Kazakhstan and North Macedonia, has lost around 11% over the last month to 173.60p at the time of writing, still leaving it around 37% underwater in the model portfolio.

Earlier this month the firm reported stable production results for Q3 from its Kounrad copper recovery plant in Kazakhstan and the Sasa zinc-lead mine in North Macedonia.

The AIM-traded firm said copper production at Kounrad totalled 3,641 tonnes for the quarter, a slight decrease from 3,661 tonnes in the third quarter of 2023, bringing total copper output for the first nine months of 2024 to 10,248 tonnes, compared to 10,377 tonnes in the same period last year.

At Sasa, zinc-in-concentrate production for the quarter was 4,768 tonnes, down from 5,127 tonnes in a year earlier. Lead-in-concentrate production stood at 6,864 tonnes, a slight drop from 7,039 tonnes on the year.

For the first nine months of 2024, zinc production reached 13,782 tonnes, and lead production was 19,736 tonnes, both reflecting year-on-year declines.

Despite the slight decreases, the company said it remained on track to meet its full-year guidance for copper production at Kounrad, targeting between 13,000 and 14,000 tonnes.

At Sasa, zinc and lead output was expected to be towards the lower end of the guidance range, with zinc production forecasted at 19,000 to 21,000 tonnes and lead production at 27,000 to 29,000 tonnes.

“The third quarter is seasonally Kounrad’s strongest quarter, and the operation remains on track to achieve full-year production firmly within the guidance range given at the start of this year,” said CEO Gavin Ferrar.

“We look forward to maintaining this progress in the fourth quarter, which we expect to result in full-year production towards the lower end of the guidance range.”

Although copper is increasingly back in favour amid emerging supply concerns, falling inflation and lower interest rates that could see demand improve markedly in the months and years ahead, CAML’s price trend is against us – so let’s move it to a HOLD for now.

Volt Lithium (TSXV: VLT)

Volt Lithium, which entered the Southbank Growth Advantage on 2 August at C$0.37, has fallen around 14% over the past month to trade last at C$0.40, leaving it 4% up in our model portfolio.

The company has developed proprietary direct lithium extraction (DLE) technology aimed at extracting lithium from North American oilfield brines, contributing to a secure critical minerals supply chain for the region.

The shares rallied on 23 October after it announced it had produced 99.5% battery-grade lithium carbonate from its US field operations located in the Permian Basin in West Texas, using its DLE technology.

This is yet another significant milestone that Volt has achieved this year, putting the company on track to become one of North America’s first commercial producers of lithium from oilfield brine.

Volt has been operating its DLE system in the field since 17 September, when the company achieved its first lithium production.

Volt has been producing lithium chloride concentrate, a precursor to lithium carbonate and other lithium compounds, from its field unit, which enables the company to cost-effectively scale-up further to process commercial levels of oilfield brine.

According to the company, samples of lithium carbonate have been created and verified via third-party testing for review by potential offtake partners.

The company stated that it will continue to produce lithium chloride concentrate, as well as technical-grade and battery-grade lithium carbonate, in the field for the remainder of 2024.

The company aims to ramp up commercial production to 100,000 barrels per day of brine during the second half of 2025.

The stock remains a BUY under its buy limit of C$0.50.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation, the world’s largest gold miner, is trading around $47.01, over 12%down on the month. The stock is now 30% below our $65.39 entry point.

After rising from under $30 at the end of February to over $58 on 22 October, Newmont shares dropped as much as 19% on 23 October after the firm released Q3 results that did not meet investor expectations amid a gold rally not seen since 2011.

Newmont posted adjusted earnings per share of $0.81 for Q3, missing the consensus forecast of $0.85, while revenue came in at $4.61 billion, below expectations of $4.67 billion.

The company produced 1.67 million attributable gold ounces in the quarter, up 4% from the prior quarter. However, costs remained elevated, with gold CAS (costs applicable to sales) rising 5% quarter-over-quarter to $1,207 per ounce.

While production improved sequentially, higher costs and lower-than-expected revenue weighed on the results, despite the company posting its highest quarterly profits in five years, bringing in $922 million in net income, nearly a six-fold year-on-year increase.

In fact, the company is now on track to report the largest annual profit in its over 100-year history.

Newmont also maintained its full-year 2024 production guidance, expecting to deliver 1.8 million attributable gold ounces at an all-in sustaining cost of $1,475 per ounce in the fourth quarter.

The miner continues to make progress on its divestment programme, announcing agreements to sell assets in Ghana and Australia for up to $1.5 billion in combined proceeds. Newmont said it remains on track to receive at least $2 billion in gross divestiture proceeds.

What’s more, despite the earnings miss, Newmont declared a quarterly dividend of $0.25 per share. The company also authorised an additional $2 billion share repurchase programme over the next 24 months.

My take on the results? They’re not as bad as the stock market reaction would suggest.

The higher costs are disappointing, but it seems three mines – Lihir, Cerro Negro and Akyem – made up a significant portion of the miss.

In fact, costs were only up $37/oz, or about 2.5%, for the Tier 1 portfolio, which are the mines Newmont is going to keep. This doesn’t seem so bad.

The biggest jump in costs comes from its non-Tier 1 assets, which increased 11% from $1,770 to $1,967 quarter on quarter. But these assets are all for sale, including Akyem, which just sold for $1 billion in cash.

Meanwhile, production at the Tier 1 assets increased by over 7.5%, while production at the non-tier 1 assets – the ones that are up for sale – declined by 12.5%.

Remember, the company remains fully exposed to a rising gold price and has 50 years of resources in the ground in superb political jurisdictions. The company is guiding to a strong Q4.

Yes, the company missed earnings, but only slightly – and that was due to inflation driving up costs more than expected. But it also beat revenue expectations and increased its share buyback by $2 billion, which is the largest share buyback in the gold sector’s history.

The company certainly now seems decent value at a time. At current prices, NEM’s price-to-earnings (PE) ratio is below 16 compared to around 30 for the S&P as a whole.

We think much of the sell-off was in part due to speculators taking some money off the table after a near-100% rally since the end of February.

With the sell-off looking overdone, Newmont remains a BUY under $100.

Prysmian Group (IL: 0NUX)

Prysmian Group is now 35% up in the model portfolio to around €65.01.

The cabling giant continues to proceed with its share buyback programme that involves a maximum of 8 million shares, equal to around 3% of the company’s share capital.

As of 25 October, the company had purchased a total number of 3,271,686 shares for a total consideration of €199 million.

In other news, the company is one of three firms down to the last stage of tendering for the contract to provide undersea 150 kV AC cables for Aegean Islands interconnectors.

Prysmian, Nexans and Fulgor are now final offers for the tender process regarding submarine alternating current (AC) cables destined for Aegean Islands interconnectors.

Greece’s electricity transmission system operator (TSO) is set to pick one of Prysmian, Nexans and Fulgor to undertake the project under a six-year framework agreement with the initial budget of the project amounting to €1.72 billion or around $1.89 billion (plus VAT).

The stock remains a buy under its buy limit of €60.

SilverCrest Metals Inc (TSX: SIL)

SilverCrest Metals, recommended in the May issue of Southbank Growth Advantage at C$12.55, is trading at C$13.62, putting it 8.53% up.

As we wrote to you in an update earlier this month, the Canadian miner has agreed to be acquired by Coeur Mining in an all-share deal valued at US$1.7 billion.

The two companies said on 4 October that, through a subsidiary, Coeur will offer 1.6022 of its shares for each SilverCrest common share, implying a consideration of US$11.34 apiece.

The offer represents a premium of 18% over the 20-day volume-weighted average prices of both companies as at Thursday’s closing levels, and a 22% premium to SilverCrest’s closing price on that day on the NYSE American (where the company also lists its shares).

Once the transaction is complete, SilverCrest shareholders will own about 37% of the combined company, and Coeur shareholders will hold the other 63%.

As we wrote, the merged company will be a monster silver miner, bigger and better than before, and able to thrive as sentiment continues to improve in the sector.

Miners are desperately looking to secure reserves amid surging demand for silver and an increasing supply deficit.

Silver prices recently rose to a 12-year high of $34.86 per ounce amid rising demand for the white metal used in industries ranging from solar panels to electronics.

SilverCrest boasts low mining costs, little debt, and a strong cash position, making it a high-margin, financially flexible investment in the precious metals sector.

Indeed, the company reported a record-breaking revenue of $80.4 million for Q3 2024, marking a 10% increase from the previous quarter, driven by the recovery and sale of significant gold and silver quantities from its Las Chispas Operation in Mexico.

The company’s operational efficiency and favourable metal prices have positioned it to potentially exceed its annual silver equivalent sales guidance of 10 million to 10.3 million ounces.

SilverCrest’s robust financials are further bolstered by a 29% increase in treasury assets, now totalling $158.2 million.

The stock remains a BUY up to C$16.

Ashtead Technology Holdings PLC (AIM: AT)

We entered into a new recommendation of subsea equipment rental company Ashtead Technology Holdings in the last issue of Southbank Growth Advantage after our original holding returned 125% in the ten months to early May.

The stock was last seen at around 550p, down 7% from our latest entry point of 590p.

Ashtead has a history supplying subsea services to the oil and gas sector but has diversified into the fast-growing offshore wind market, specialising in renting out equipment crucial for the operations of installations throughout their lifecycle.

The company’s technology offerings include surveying equipment, sensors and robotics essential for installation, operation, maintenance and decommissioning of assets.

Since our most recent recommendation, the company has acquired underwater rental businesses Seatronics and J2 for £63 million in cash.

The deal is funded by a £70 million increase in Ashtead’s revolving credit facility.

Seatronics and J2 were owned by Acteon Group. They provide subsea electronics and ROV tooling rental services, complementing Ashtead’s existing portfolio.

This acquisition will expand Ashtead Technology’s survey and robotics rental fleet and services, adding more than 7,000 proprietary assets and increasing its rental portfolio by 30%. It will also bring in a workforce of 110 employees.

Seatronics and J2 operate in key offshore locations, including the UK, US, UAE and Singapore, and generated revenues of £51.5 million in the trailing 12 months to September 2024.

The purchase of Seatronics and J2 Subsea will be Ashtead Technology’s ninth acquisition in seven years, signalling a strategic expansion of its capabilities.

A flurry of M&A deals helped Ashtead see a surge in revenue in its 2023 full-year results, with revenue growing 51% to £110.5 million compared to £73.1 million in 2022.

The stock remains a buy under 700p.

Oklo (NYSE: OKLO) and Centrus Energy (NYSE American: LEU)

Oklo has been a tough stock to work with in the last nine months. Our first foray into the stock was before it was even Oklo and traded as a special purpose acquisition company (SPAC). Nonetheless, the conversion to Oklo and the conviction we had that it would be one of Sam Altman’s biggest successes didn’t waiver.

Then Oklo’s price headed south, and didn’t stop. So much so that it crossed our lower stop level, forcing us out of the stock. That was painful. But prudent risk management suggests most of the time stocks don’t recover from heading that far south.

But we were convinced Oklo wasn’t being fully appreciated by the market. Particularly because of the demand for nuclear energy coming from data centres and AI. It’s a big part of why we’ve been beating the drum of nuclear energy stocks for almost three years now.

That’s why we re-entered Oklo. Once it turned its nose higher and showed that forward momentum, we wanted it back in our buy list. Our conviction thus far has proved right. From our second entry back in, the stock is now showing a 145% gain.

There will be temptation to sell. That’s fine if it’s hit the targets you set out for yourself or you just want to take some profit off the table. I get that. But my take is that the story has only just begun for SMR tech and the nuclear industry.

This is a long conviction play on the insatiable demand for carbon-free energy from Big Tech and the requirement for that nuclear energy to come directly out of the US. And the need for that energy sooner rather than later.

These are only things that SMR tech can provide. It’s why Big Tech is ready to spend up big so they can sure-up their supply of energy. Companies like Oklo may still be early stage, but I expect big deals to start soon, hitting their news flow.

That means I’m expecting more profit from here. Therefore, we’re not looking to take profits on this yet.

That said, we still want to employ smart risk protection here. As seen this last week with a bit of a selloff in the tech sector, you never really know what’s around the corner. That’s why we’re going to put in a 50% trailing stop exit on Oklo at current prices. This will allow us to run up with the stock but ensure a minimum profit is maintained.

Actio to take: set a trailing 50% stop exit on Oklo.

The same case for Centrus Energy. It too has run higher because the need to secure supply of enriched uranium, particularly HALEU, in the US is evident. SMRs and new nuclear reactor designs require HALEU. Its production needs to come from the US. Centrus is in such a unique position to capture that demand it makes it one of the most promising stocks on the market.

Again, temptation would be to sell with a 171% return in the coffers, but I just see more upside from here. I think that with both Centrus and Oklo, we could be looking at two of the elusive 10-baggers in our stables here.

But we must also be rational. So to protect downside on Centrus should our conviction be wrong, we will set a 50% trailing stop on Centrus too, guaranteeing profit should the stock price dramatically turn against us.

Action to take: set a trailing 50% stop exit on Centrus.

Volex (LON: VLX)

Volex is one of those stocks that has been on our buy list for a few years now. It’s been up, down, down a lot, and is now in a profit position for us.

It’s not really got the momentum we’ve expected over the last couple of years. I think now it is lacking that big explosive potential to soar to those heights we first expected.

It may continue to grind higher, but we think there are better, more explosive opportunities in the market now. So, while it’s not a horrible outcome, it’s not as good as we’d expected. It’s been with us for some time, so we think now is a good chance to exit the stock and take the small win.

SELL: Volex Plc (LSE:VLX)

IOTA (IOTA)

As a cryptocurrency, IOTA has been in the buy list as a legacy recommendation from many moons ago, late 2019. In those five years it is still at a 57% loss. Now, it should be said I think a big crypto cycle is going to kick off and that will deliver a splattering of big rises in a number of crypto, IOTA included.

But this is not the service for IOTA to exist as a recommendation as we don’t make crypto recommendations here; that is exclusively reserved for our crypto service, Alpha Crypto, which has further requirements on us to ensure that people receiving that information and recommendations are appropriately qualified.

As such, we won’t be covering IOTA in this service anymore. But what I will do is give you defined hard targets for the exit level that I think you should aim for and where it’s just time to let it go.

Target sell price: $2.52

Stop exit price: $0.10

Pod Point (LON: PODP)

If Oklo and Centrus are the poster children of the nuclear surge higher, Pod Point is the poster child of the EV crash back to reality. For all the government promises of funding and the push to EVs and a cleaner and greener future, none of it has materialised in Pod Point’s stock price.

If anything, the rollout of EV infrastructure in the UK to a meaningful and widespread domestic market seems further away now than it ever has. And Pod Point just isn’t going to get back to the heights it was once at.

It’s also a stark reminder that regardless of growth stock volatility, hardened stop exits are a necessity on all positions, which we’ve been utilising more of recently. That said, it’s a hard and heavy loss but it’s time to cut Pod Point away and turn to more fruitful opportunities.

Action to take: SELL Pod Point Plc (LSE:PODP).

Inside the lives of James and Sam

James:

The Allen family WhatsApp group has been dominated in recent weeks by lots of chat about our ancestry.

My 10-year-old nephew was recently tasked with learning about our family tree as part of a school project, so his dad – my brother Tom – signed up to ancestry.com on his behalf.

The joke before Tom started was that he would find a secret baby lurking somewhere in the family tree. Although that hasn’t (yet) proved the case, he has discovered a lot of other very interesting material that we had no clue of this time last month.

For starters, he found the name of my paternal grandmother’s first husband, who she married and divorced before marrying my grandfather, Ronald.

Apparently, my granny, who died aged 98 in 2009, always kept this secret from my dad, who only found out about it by chance just before she died, though he never knew his mother’s first husband’s name – until now.

So a belated welcome to the family, Peter Ralph Quixano-Henriques!

Perhaps the most poignant thing we have discovered is the location of the gravestone of my granny’s younger brother, Philip, my dad’s uncle. Philip was a pilot in WW2 and was shot down over the Netherlands in July 1944, much to the life-long distress of his elder sister.

Up until now, my dad and his siblings had no idea where their uncle Philip had laid to rest, so it’s been heart-warming to see a photo of his gravestone in Woensel, Eindhoven. I’d really like to visit one day.

What else have we discovered? Well, we have also learnt that my dad’s third great-grandfather was – ahem – kind of a big deal. William Stancomb was his name and he was the High Sheriff of Wiltshire in 1879. In fact, according to ancestry.com, there is a portrait of him and his wife Margaret that hangs today in the BritishTrowbridge Museum.

Speaking of glamour, one of the key tasks we gave my brother when he started his voyage of discovery was to find the link to someone we have long been told sits somewhere on my dad’s side of the family tree: Sir Thomas Bond (1620-1685), an aristocrat and property developer whose estate included what ended up being a famously well-to-do street in London that was eventually named after him – Bond Street.

As my partner can testify, I have dined out on this story for years, not allowing a trip to Bond Street to pass without a comment, nudge or knowing wink in her direction, so I for one have been eagerly awaiting official confirmation that this story wasn’t some family myth passed down the generations with no basis in truth.

The good news is that Tom has indeed traced the Bond name in the family – but only as far back to the suitably-named James H Bond (1844-1905), my dad’s great grandfather on his father’s side. Tom says he still needs more information to go further up the tree to find Sir Thomas, but he tells us he is on the case. Fingers crossed on that front.

But balancing out these somewhat tenuous ties to grandeur, we have also discovered that, amongst the West Country farmers and cheese makers going back a few generations on my dad’s side, there were – how shall we put it – not the unoccasional instance of Allens marrying other Allens whose respective families sit remarkably close to each other in the family tree. I’ll take no further questions on that one.

Although my brother has so far mainly concentrated on my dad’s side, we were pleased to learn that the branches of the family tree on my mum’s side were somewhat further-reaching, even extending to the United States.

Indeed, Mum’s great great grandmother, Mary-Ann Randall, was a bonafide American. Remarkably, she was born in Norfolk, Massachusetts, in 1812 and died in Norfolk, England, in 1896.

This has been, more or less, the limit of what we have discovered so far, although there is certainly much more to learn. What’s clear is that Tom has certainly got his money’s worth from his membership to ancestry.com. You can also see why genealogy is big business, with a global market valued at $5.4 billion in 2023 and projected to reach $15.8 billion by 2033.

As some of you might know, ancestry.com used to be a public company, with its shares traded on Nasdaq, but in 2020, 11 years after listing, it was taken private by the Blackstone Group for $4.7 billion.

Today, the company operates in over 30 countries and has more than 3.6 million subscribers, making it one of the largest for-profit genealogy companies in the world. With annual revenues apparently in the region of $5 billion, it’s fair to say Blackstone struck a good deal.

Although the genealogy sector is not one I’ve looked at before, my new found enthusiasm with family trees means I’m certainly interested in finding other good deals in the market. If I find something suitable for retail investors, you will, of course, be the first to know.

Sam:

Lessons learnt from being a foreigner

After 11 years of absence, I returned to Australia. A decade in the UK, a year in Portugal, a long time away, but also no time at all.

The inevitable questions come thick and fast, but most notably people here ask, why?

Ultimately it matters little as to why. The thing, however, is that there was no singular reason, but stacked up, a bunch of smaller things adds up to a lot.

One big thing was the ridiculousness of legal immigration. You’d have thought that after ten years in the UK, paying a lot of tax, having two children and a wife that are all British citizens by birth, my pathway to permanent residency and then citizenship myself would be a bit of a slam dunk.

No. Not at all. When time came (five years) to apply for those things, apparently my original entry into the country was on the “wrong kind” of visa. A perfectly legal visa, yes. But the “wrong kind” to enable permanent residency. Hence my application was too early.

Therefore, in the infinite wisdom of UK Visas and Immigration (UKVI), instead of just saying, apply again in a month, they bumped me onto a ten-year pathway to staying in the country long term. That of course required an extension of 2.5 years (plus all fees and charges and “health surcharge” payments which each visa renewal/extension tallies into the thousands of pounds) plus another extension (plus all fees and charges and “health surcharge” payment).

And these are all still in addition to the regular taxes that I, like you, are required to pay. Of course, the threat that looms over my head in such situations of noncompliance is deportation.

I don’t want to slide down the pathway of whingeing. But Holy Moses, getting legal permanent residency as a higher rate tax payer, who’s deeply entrenched in the British culture and lifestyle, is contributing to society, trying to carve out a positive life for the family is far too filled with BS red tape, government bureaucracy, expenses and complexity.

And that’s just the visas and immigration department. Then you get to the fact that you pay more and more and more in taxes every year and get less and less and less and less. But the real kicker (I won’t go into excessive detail here because it’s a highly private matter) is that when you need the NHS in one of life’s most precious moments (like the birth of a child) and they fail you, not just in a little way, but in a serious wa,y it’s hard not to be filled with extreme frustration, disappointment and, yeah, a bit of anger.

I’m lucky enough that when you’re failed time and time again by the system, be it immigration, taxation, healthcare, I can pick up stumps and go somewhere else. So we did. But when you read in the paper that there’s a drain of people from the UK who you’d think on the balance are a net positive to the country, you can count me as one of them.

I’ll keep the Portugal part of this tale for another time, but parts were very much the same, parts much better. I know that people will also say that Australia is very much politically heading down the same path as the UK. To an extent it is, and it’s sad to see.

But there are also some things that work. Like the healthcare system (where around 2% less is spent as a share of GDP than the UK, but life expectancy at birth is around eight years higher), immigration (so long as you’re trying to get here legally) and housing where you get more bang for your buck (so to speak).

[Side note: the IEA did a balanced research paper on the Australian healthcare system, if you want to understand a bit more how it works and why it works, this is worth a read.]

Sure, there are shortcoming here in “Oz” too, but when kids are involved in the decision-making process (i.e. about what’s best for them) it’s sad to say but the UK kind of pushed us out. My kids are still British, my wife is too, and I genuinely love the country and the people. But by-jingos (I picked up the lingo back here quick-sticks) I’m very glad we left because it’s hard to see all the reasons we left getting any better anytime soon.

Crypto Corner

Sam:

The Crypto IPO could be great or the biggest top signal of all…

In 2021 the crypto market was going through another of its infamous blow-off-top, FOMO-induced cycles higher.

It was wild, fun, terrifying, exhilarating and depressing (out the other side). Money was made, money was lost, as is the case with the crypto market.

Amidst the mania of NFTs, P2E gaming and altcoin-szn, there was another story playing out, but in the traditional markets.

Coinbase, one of the most long-standing companies in the entire crypto world, had over time raised a truck tonne of capital to grow and become a stalwart of the industry.

Even today, while it gets a fair share of backlash (mostly unfairly in my book) it keeps trucking on, innovating, developing and being a net benefit for the crypto industry.

I like Coinbase because when I first came across it, I think it was around a decade ago now, I had always wanted to invest in it whilst it was a private company. But I didn’t have the hordes of capital of a VC and as such, I had to wait like most people.

And then in 2021 Coinbase did its IPO – and it was HUGE.

Coinbase had a reference price of $250 per share on the first day of trading and then traded up to like $330. Then the arse fell out of the crypto market, the stock market and devastation ensued.

Coinbase has not yet reached the highs of 2021 and its IPO since. I expect it will, but it’s still a little way off yet – at least, I reckon, until bitcoin heads past $100K (more on that in a second).

But Coinbase is also around six-times higher than the low it hit in 2022. So, things are at least trending up.

However, this is all relevant now, not for Coinbase, but for one of its biggest competitors, Kraken.

You see, I have an account with an equity funding platform. And recently an opportunity popped up to invest in Kraken. It’s worth noting that offer is still open. I have not yet invested, and I’m not sure if I will or not.

But the expectation is that this might be the final round of private investment in Kraken until it goes public.

There is talk that Kraken is looking to IPO off the back of this round of investment, so you’d expect some time in 2025.

If that is true and it’s on the hunt to IPO, then I think the market is going to really fire up and shoot higher. Because these companies have a knack of timing their IPOs to maximise existing investors’ portfolios… just not so much the public market.

Therein lies the downside. While Kraken might be a HUGE IPO like Coinbase, doing great things for early investors, it may also be a raging sign of a market top – like Coinbase was.

Or maybe I’m being too harsh on Coinbase – that it wasn’t the top signal, it was just an unfortunate passenger on a ride always destined to be rocky?

Point being that if a company like Kraken is ready to IPO or is seriously considering it, then I’m mega-bullish on the market into 2025.

That brings me to bitcoin. It’s doing what we expected. It’s ever-so-close to its all-time highs. While it is not exactly perfect timing, it’s right back to where we said it would get to. I still expect it to break into $100,000 and then higher towards $500,000 and higher again.

A million dollars? Possibly, but if not this cycle, my view is at some point in the next few years, yes. If you don’t believe me about it, then look at what Michael Saylor continues to do at MicroStrategy. The company is now planning on buying as much as $42 billion of bitcoin in the next three years.

Maybe I’m not bullish enough!

What else we’ve been looking at this month

James:

CATL announces EV battery with 600,000 miles warranty

We might just have heard the last of the “how long do the batteries last?” type of arguments.

In September, Contemporary Amperex Technology (CATL) – the world’s largest battery maker – announced it will supply an EV battery that can last 15 years and nearly one million miles.

CATL is selling the battery with a 10-year or 600,000-miles warranty, guaranteeing it will have 85% capacity retention at that stage (and close to zero battery degradation in the first 1,000 charge-discharge cycles).

In fact, CATL’s R&D labs have shown that the lithium iron phosphate (LFP) batteries of this type can actually last 16 years before their capacity drops to 85% of the original, so more than on the warranty. The batteries’ life expectancy is 900,000 miles.

As per an article in Battery Industry: “For comparison, current batteries in Teslas and other EVs only come with eight-year warranty and 70% capacity retention. This means that CATL’s new battery can nearly double the worry-free lifespan of an EV.”

The long-life batteries in question are now moving from the R&D and prototype stage to the launch phase. The LFP battery will operate in buses, light trucks and heavy trucks.

This, truly, is a game-changer – one that shows the now unstoppable pace of progress in batteries.

Man who accidentally sent £440 million in bitcoins to dump now suing local council

The decade-long saga of a man who accidentally discarded a hard drive containing 8,000 bitcoins worth over half a billion dollars has taken a further twist.

A mix-up saw James Howells’ hard drive dumped at a recycling centre in 2013 causing him to lose access to cryptocurrency coins that have since rocketed in value.

He said it was worth £4 million when it was mistakenly binned, though current market estimates value the coins at around £440,000.

Howell – now 38 – has spent the subsequent years petitioning Newport council to grant him access to the dump to search for it.

He even assembled a team to carry out a £10 million excavation of the landfill – at no cost to the council – which would take between 18 and 36 months to carry out with a further year of remediation work.

But Newport council has steadfastly refused his requests out of environmental concerns, despite Howells offering them 10% of the coins’ value if recovered.

In the latest twist, Howells is now suing the council for £495,314,800 in damages, which was the peak valuation of his 8,000 bitcoins from earlier this year.

The case is due to be heard in December this year, but Howells said that his aim is to “leverage” the council into agreeing to an excavation of the site in order to avoid a legal battle, according to a report by WalesOnline.

“I’m still allocating 10% of the value for the council even though they have been problematic throughout,” he said.

“That would be £41 million based on today’s rate but in the future it could be hundreds of millions. If they had spoken to me in 2013 this place would look like Las Vegas now. Newport would look like Dubai. That’s the kind of opportunity they’ve missed.”

Howells says this is his “final shot” to try to locate his hard drive and I for one am rooting for him.

There’s a new natural gas top dog in town

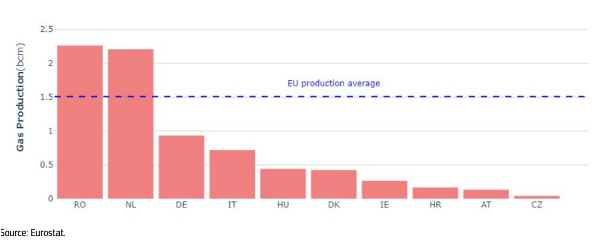

You might be surprised to read that the largest natural gas producer in the EU is not Germany or the Netherlands, but – as of Q2 this year – Romania.

According to a recent report from the European Commission, the eastern European country became officially the EU’s biggest gas produce between April and end-June, producing 2.3 billion cubic metres, a rise of 1% year on year.

In doing so it surpassed the Netherlands, which produced 2.2 billion cubic metres, a fall of 17% from the same quarter in 2023.

The third largest producer remained Germany (0.9 billion cubic metres), followed by Italy (0.7 billion cubic metres) in fourth place and Hungary (0.4 billion cubic metres) in fifth place.

Source: European Commission

The increase in Romania’s production is attributed to strategic investments and new drilling projects in the country.

Meanwhile, Netherlands’s drop reflects the fact it closed down its massive Groningen field in October 2023 due to concerns over earthquakes.

Romania’s growth is particularly notable given the overall decline in gas production across the EU, which saw an 18% year-on-year decrease in 2024.

It’s likely Romania’s rise to the top is no flash in the pan. The country is set to become an even more significant natural gas producer from 2027 when the Neptun Deep field becomes operational.

Sam:

Earnings and more earnings

It’s earnings season, and while it’s notably good for short-term noise, it doesn’t change much of my long-term view on AI and nuclear energy. But still, it’s important to read because you very quickly realise how massivethese companies could get if their big and expensive bets on AI actually pay off down the track like they think it will.

So, here’s what I’ve been reading…

(Note you’ll probably need to add your email to get all these.)

Google – seekingalpha.com/article/4730692-alphabet-inc-goog-q3-2024-earnings-call-transcript

AMD – seekingalpha.com/article/4730678-advanced-micro-devices-inc-amd-q3-2024-earnings-call-transcript

Meta – seekingalpha.com/article/4731243-meta-platforms-inc-meta-q3-2024-earnings-call-transcript

Microsoft – seekingalpha.com/article/4731223-microsoft-corporation-msft-q1-2025-earnings-call-transcript

And just because this guy is a full-blown bitcoin maximalist…

MicroStrategy – seekingalpha.com/article/4731304-microstrategy-incorporated-mstr-q3-2024-earnings-call-transcript

It’s not glamourous work but it sure is fascinating!

James Allen and Sam Volkering

Editors, Southbank Growth Advantage