Your December issue of Small Cap Investigator

21st December 2023 |

- If bitcoin “moons” 🚀 then you’ll want to own these two stocks

- Big breakthroughs

- Buy List update

- Inside the lives of James and Sam

- Crypto Corner

- What else we’ve been looking at this month

If bitcoin “moons” 🚀 then you’ll want to own these two stocks

Sam:

In the next few minutes or however long it takes you to read this next stock recommendation, I’m going to be talking to you mainly about one thing…

Bitcoin.

However, I won’t be recommending you go buy any bitcoin whatsoever.

If you don’t like bitcoin, if you think it’s a giant Ponzi scheme or as Warren Buffett has said, its “rat poison squared”, then don’t bother reading the rest of this.

Just move on to the next section.

But if you want to see a way to potentially profit at an accelerated rate should the bitcoin price “moon” over the next year (as I’ve repeatedly predicted it will) then read on.

Because you don’t have to own bitcoin to still profit from its meteoric rise. Even if you do have bitcoin and like me, see the huge, long-term potential it has, this is still for you. That’s because the two stocks you’re about to learn about are what I consider the best way to play the next crypto bull market cycle not just without having to own any bitcoin, but also as they could outstrip even the performance of the world’s premier digital asset.

It’s just a picks and shovels story

Let’s tackle the thing that gets in most people’s way first whenever we start talking about bitcoin: the volatility.

In no way shape or form am I saying that bitcoin and anything related to it aren’t volatile. It is part and parcel of this market.

But there’s a few things that you cannot deny. Let me show you.

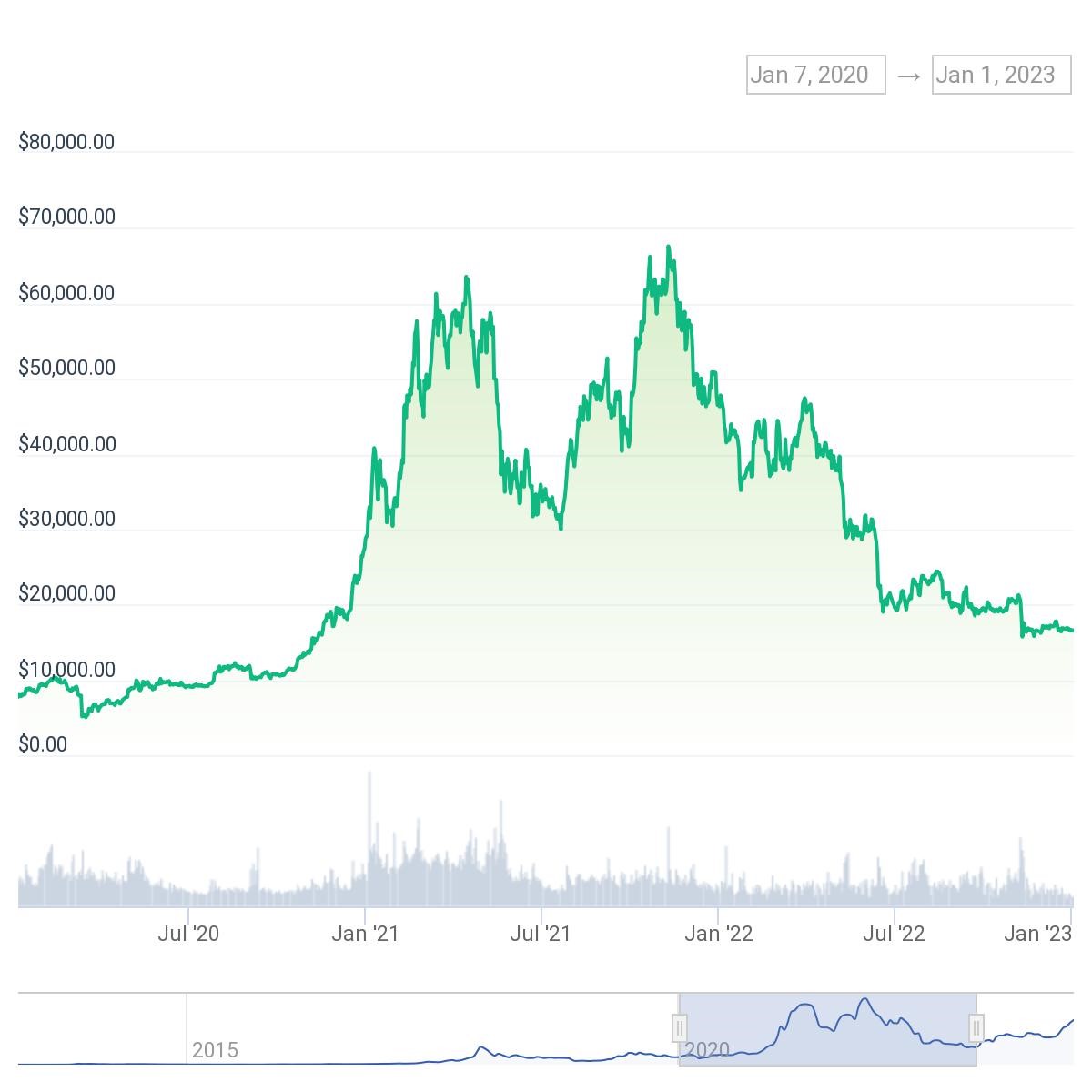

The last major crypto bull market cycle began in 2020 and launched into 2021. At its peak price on 10 November 2021, one bitcoin was worth US$69,044.

Source: Coingecko

Source: Coingecko

It had launched from a “Covid shock” low in March 2020 of around $5,000 to deliver an astonishing 1,280% return by November. Also note the “double peak” the market gave us in 2021, – the first around February, the second in November.

Now look at the next chart…

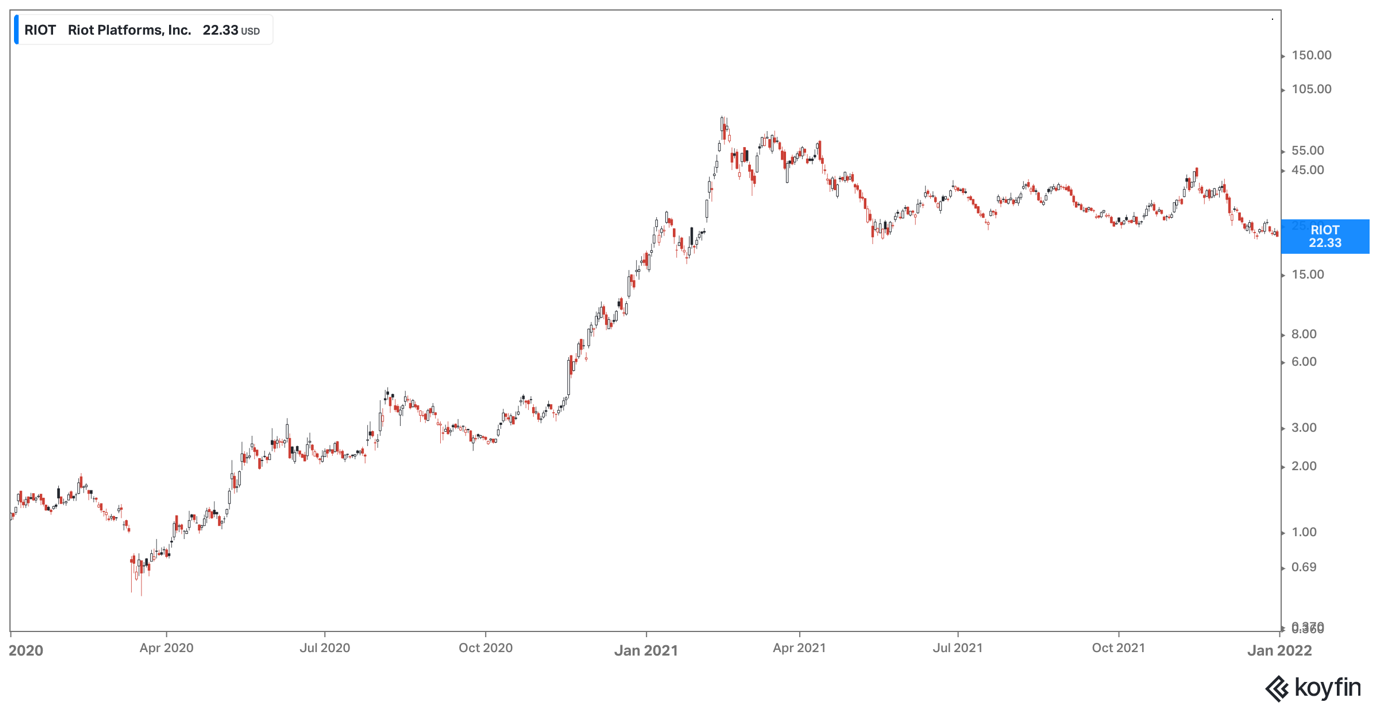

Source: Koyfin

Source: Koyfin

This is the chart of RIOT Platforms (NASDAQ:RIOT). RIOT is one of the longest standing publicly listed bitcoin mining companies. Its job is to mine bitcoin using high-performance computing resources. It’s not an overly complex business model: mine bitcoin at a cost-effective price, sell bitcoin, keep bitcoin, grow revenues and value.

OK, there’s a bit more to it than just that. But RIOT’s primary focus is the mining of bitcoin. So when the value of bitcoin goes up, you would expect the value of a company like RIOT to go up too.

And that’s exactly what it did in 2021.

From a “Covid shock” low of around 51 cents in March 2021, RIOT tracked the rise in bitcoin’s value higher. But RIOT didn’t deliver a 1,280% return from low to peak.

RIOT’s price peaked in February 2021, the first bitcoin peak that year. At that point the price of RIOT stock was around $79.

That’s a low-to-peak return of 15,390%.

Not only did the performance of RIOT’s stock outpace bitcoin… but it did so by a factor of 12!

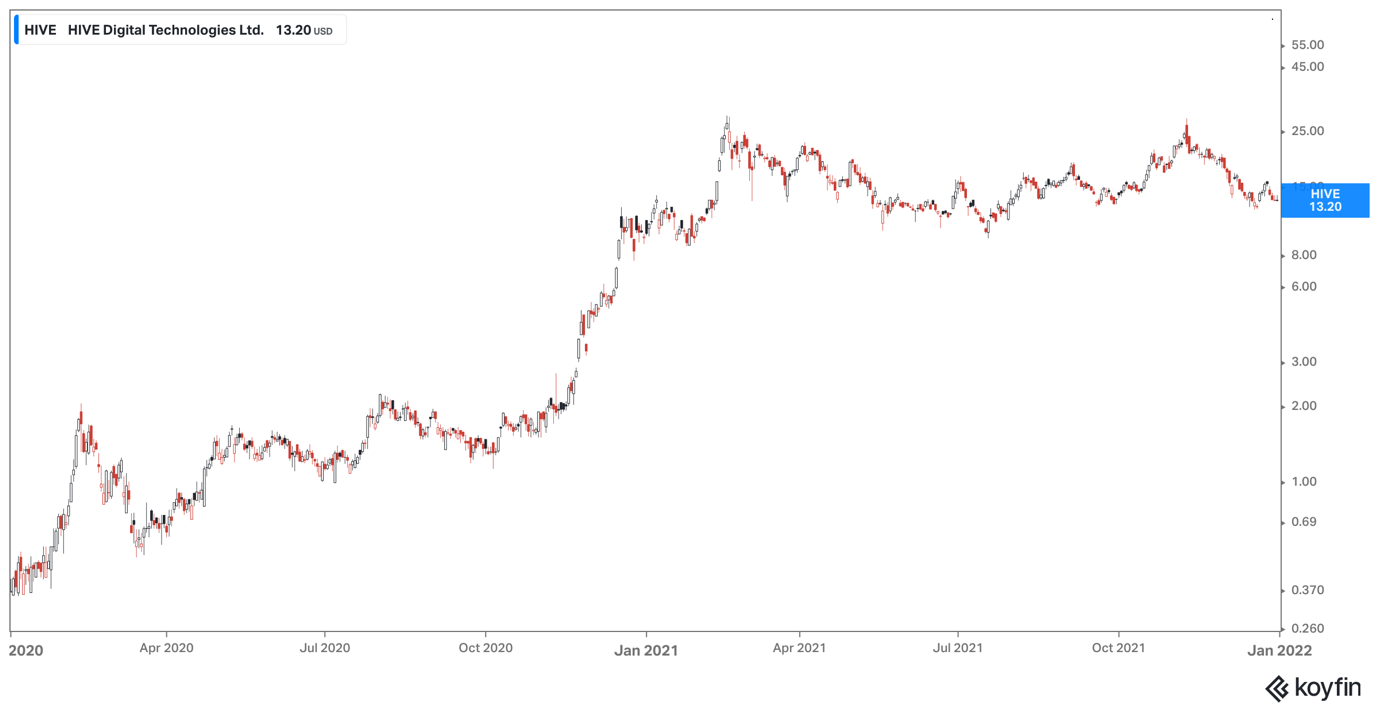

Here’s a similar chart, this time from bitcoin miner HIVE Digital Technologies. Again, it’s been around for some time and as you would expect, it too tracked the price of bitcoin higher…

Source: Koyfin

Source: Koyfin

HIVE’s low was before the “Covid shock” in March. The stock was trading around 35 cents in early 2020.

HIVE went on to follow bitcoin’s rise higher too. It peaked around the same heights in both February and November. Its peak price was around $28.

That’s a 7,900% return. Not quite the RIOT explosion, but still outstripping the rise of bitcoin by a factor of more than six times.

Of course these returns perfectly coincide with the rise in bitcoin’s price, as you would expect.

So when bitcoin’s price decided to take a turn south, so did the stock price of both these bitcoin miners.

By the end of 2022, the depths of the most recent “crypto winter” (a period in the cycle when prices crash) HIVE’s stock traded down to around $1.36 (a 95% fall) and RIOT’s price was down to $3.25 (also a 95% fall).

And for what it’s worth, bitcoin’s price was down to around $16,000 (a 76% fall).

As you can see, when they’re up, they’re up. But when they’re down… oh boy are they down.

So when we talk about bitcoin, we also always talk about price volatility. And when we talk about bitcoin miners, well you can see for yourself the kind of stomach you need for these stocks.

However, what is clear is that if you have some exposure to these stocks, which you can and which is easy to do through most brokerage accounts, then you can make hard and fast returns, if you’re of the view that bitcoin’s price is set for another massive price rise.

Again, it’s not an overly complex idea.

For example, if you’re a bitcoin miner and you’re mining around 200 bitcoin a month and the price of bitcoin is around $40,000 (which it is now) then you’re mining around $8 million a month.

Now, if bitcoin is at $69,000, then suddenly your monthly revenues (in terms of bitcoin) stand at $13.8 million.

However…

What if bitcoin is at 100,000? Or $1 million per bitcoin.

Hang on a minute… $1 million? Am I for real? Well, yes, I am, and here’s why.

$1 million bitcoin

Right now bitcoin’s price is around $40,000. Its all-time high is $69,000. So how does $1 million per bitcoin even become remotely possible?

Right now there are two imminent converging factors in play.

The first is a tidal wave of capital that’s about to be unlocked thanks to the world’ biggest financial institutions finally getting the green light to dive head-first into bitcoin.

The second is the next major constraint of new bitcoin supply to market, which is only around four months away.

That means a gigantic rise in demand and a slashing of supply. This kind of imbalance for a scarce asset like bitcoin suggests that its price is heading higher… a lot higher.

In January, just weeks away, the expectation is that the US will finally give the green light for as many as 12 new spot bitcoin exchange-traded funds (ETFs) to hit the market.

That’s bitcoin ETFs from the likes of BlackRock (through iShares), VanEck, Fidelity, WisdomTree, Invesco, Ark Invest, Greyscale and a slew of others.

Combined, these giants’ manage tens of trillions in assets. Regulated, listed, bitcoin spot ETFs could very well see tens of billions of dollars flowing into these funds within weeks of their launch.

For some comparison there’s around 34 gold ETFs trading on the US markets with combined assets under management (AUM) of around $115 billion. That same level of capital flow to bitcoin ETFs, which I expect there will be, works out at around 14% of bitcoin’s current market cap.

However, that’s based on current bitcoin supply which is at 19.57 million bitcoin.

We know, however, that a lot of bitcoin is lost, untouched, in places where it shall never return. We also know that 70% of bitcoin hasn’t moved in over a year. That means hodlers aren’t easily willing to part with their bitcoin.

The liquid supply of bitcoin in the market is only around 1.3 million BTC.

At current prices, that means if the BlackRock bitcoin ETF, for example, were to see capital inflows of $55 billion (which is not crazy considering the largest gold ETF is $57 billion of AUM) then it would need to hold 1.3 million bitcoin.

In other words, for a $55 billion bitcoin ETF to fill its coffers with the necessary bitcoin, it would need to buy all liquid bitcoin in the market.

That’s just one ETF. What about the other 11 that are expected to be approved? Simply put, there’d be no bitcoin left.

Unless… the price moves high enough that the 70% of hodlers are willing to let some of that bitcoin go.

How high? Well we simply don’t know. But for those who might have bought the top of the market at $69,000, then I’m guessing it could be multiples higher than that.

The reality is if these ETFs are approved, the capital flows and there just isn’t enough bitcoin to supply the demand, we would expect this to force prices higher.

Then predications of $1 million per bitcoin, which have come from the like of Cathie Wood (whose ARK Invest is one of the ETF applicants), isn’t as wild as you might think.

And just to make matters even tighter, in April the bitcoin block reward is set to drop from its current 6.25 BTC per block to 3.125. That means new bitcoin supply hitting the market, is cut in half.

The “halvening” event has historically seen the bitcoin prices cycles kick off and acts as one of the catalysts of the bull market cycles.

All it does in this next cycle is make it even harder again for liquid bitcoin to be accessible in the market. That kind of constricting supply, with that demand expected, leads me to think that we’re at the start of the next major bitcoin price run.

Back to the miners

Now if bitcoin hits $1 million and you’re a bitcoin miner pulling in 200 BTC a month, your monthly mining revenues are now $200 million.

It’s also worth noting that while these miners will mine and then often sell their bitcoin, they often keep some in reserves on their balance sheets.

If you’re a bitcoin miner with 9,366 BTC on your balance sheet at a price of $40,000, then your total BTC is worth $374.6 million. But at $1 million, you’re sitting on a bitcoin pile worth $93.6 billion.

These numbers don’t seem real sometimes. I know first-hand that sceptics will say they’re not real. That it’s all just fake money, just numbers on a page. That these revenues and holdings are based on nothing and worthless.

I can’t necessarily change that view of people. I can’t change necessarily how they feel about bitcoin or whether they see value in it or not. But what is undeniable is that there are several stocks that trade mainly on the US stock market that absolutely rocket higher when bitcoin goes on a run.

That’s not made up or pretend. That’s legitimate opportunity to get into stocks that you can buy and then sell through your brokerage account which can transform your portfolio if you’re in and out at the right time.

Even if bitcoin doesn’t soar to $1 million, even if it only doubles or triples its previous all-time high, as you saw earlier, these miners do tend to outperform bitcoin as an asset on its own.

While I absolutely believe everyone should have some bitcoin on its own as an asset in their wealth strategy, I know that a lot of people simply don’t want to bother with the practicalities of that.

That’s why bitcoin miners make for a great proxy to play the rise of bitcoin’s price, but in stocks that you can jump into through your stocks trading app, and quickly and easily buy.

Before you dive in though, you need to know going in that these kinds of stocks are still risky, volatile and tied inherently to bitcoin’s price. So yes, they can rise astronomically faster, but if the market turns, they can absolutely wipe capital into the bin on the way down.

That’s why I say, if you’re investing in bitcoin miners, which is what this whole report is about, there are two things you need to do.

- Be money smart: only use a small amount of high-risk capital. This is not something you throw your whole portfolio at.

- Trade smart: set targets on the way up to take profit and use a stop loss to protect your backside.

If you’re disciplined enough to do that, then here are two bitcoin miners to add to your portfolio now, before bitcoin’s price explodes higher again.

Bitcoin Miner #1: Hut 8 Corp (NASDAQ:HUT)

Hut 8 Corp is a new company that is only weeks old. That’s because on 30 November, a merger between Hut 8 Mining (the old Hut 8) and USBTC (another bitcoin miner) completed after months of hurdles to clear.

This merger, which is now just called Hut 8 Corp, “is the largest merger and acquisitions (M&A) activity that has ever transpired within [the crypto mining industry],” according to the company announcement.

It is, as you would expect, a serious player in the bitcoin mining space. I think a key part of its strategy that fits in with the upcoming spate of ETF approvals is the fact that it’s fully US domiciled, with mining facilities in the US and Canada.

That might seem like it’s not a good thing considering a lot of the pushback against bitcoin and crypto from US regulators and politicians. But I think there will be growing demand from the ETFs in the US to “buy US bitcoin”.

Another way of looking at it, is that these US ETFs won’t want to hold bitcoin that’s perhaps come through Russia via Gaza, as a polite way of putting it. I think buying bitcoin from miners that are a known quantity will become increasingly important. In fact, it may become the only way that some of these US ETFs are allowed to add bitcoin if the regulators have their way.

Nonetheless, on top of its mining operations, Hut 8 – like many bitcoin miners – also utilises its high-performance hardware for the emerging AI and high-performance computing industry too.

Bitcoin miners typically use high-power, high-performance hardware like application-specific integrated circuit (ASIC) hardware that is dedicated to bitcoin mining. Many also use high-performance GPUs, like the ones that come from chip giant Nvidia.

This hardware needed to mine bitcoin is at its most basic principles, just really fast computers. That means they can be used to do other things that require really fast computers, like processing data needed for the artificial intelligence (AI) industry. This has already started to provide fruitful with a deal inked in June this year for Hut 8 to provide HPC infrastructure for Interior Health based out of Canada.

This kind of flexibility and adaptability adds a further string to the bow of these miners, as it means they’re not completely a one-trick pony.

However, it is the bitcoin mining we’re here for. What make Hut 8 valuable is the recent combination with USBTC, but also the huge holding Hut 8 has in bitcoin. As of its last quarterly update it held 9,366 BTC ($374 million at $40,000 per BTC).

Last quarter it mined 330 bitcoin as well. At $40,000 that’s $13.2 million in revenues from mining operations. The HPC revenues added another $4.5 million to the coffers.

It’s worth noting that these figures are all before the combination with USBTC completed, and we’re yet to get a full quarter of performance with the new entity.

You can see however, that if bitcoin’s price explodes higher, how Hut 8 (even without USBTC) stands to benefit. Its BTC holdings alone make the company excitingly placed for a new bull market.

Risks

In terms of risks, as outlined earlier, the key thing here is bitcoin’s price. If it skyrockets, then we know what to expect.

But if bitcoin’s price does nothing, or worse, falls, then you will lose money in this stock. Bitcoin’s price goes down so does Hut 8. And the volatility day to day, means you can expect to see big price swings, double digits in a day.

Also, it’s necessary to note that with the block reward halving in April 2024, that does mean miner revenues also fall as the expectation is that they will mine less bitcoin each month. That 330 bitcoin might not cut in half, but it will reduce.

This is partially offset by increases in bitcoin block transactions fees, but not completely. I would expect to see quarterly mining numbers closer to 200 after April. The expectation is though that with increases in price, that also offsets the dollar value of revenues generated.

Hence if bitcoin’s price is stagnant or lower come April 2024, then the decrease in mining dollar revenue may also drag the price lower.

Still, my view is that 2024 will see the crypto market and bitcoin’s price boom again, and thereby Hut 8’s stock price.

Action to take: BUY Hut 8 Corp (NASDAQ:HUT)

Market cap: 2 billion

Current price (20.12.23): US$12.15

Buy up to $13.75

Set a stop loss at $6

Bitcoin Miner #2: CleanSpark Mining (NASDAQ:CLSK)

CleanSpark is another bitcoin miner that is very similar to Hut 8.

We’ve already seen the company start to trend higher in line with the bitcoin rises in recent weeks, showing that as bitcoin’s value rises, so does CleanSpark.

What’s great about CleanSpark is that for its 2023 fiscal year it grew revenues year on year. That’s no mean feat considering the crypto market has been at the tail end of another of its “crypto winters”.

CleanSpark also has $762 million in assets (that’s cash, BTC and all its mining equipment, which in an AI and HPC world is very valuable).

But CleanSpark is clearly operating at an incredible efficiency with its mining operations. In its November mining update it noted it was its “second-highest monthly bitcoin production despite increased difficulty and without using more energy.”

For the month it mined 666 bitcoin, which at $40,000 equates to $26.6 million in bitcoin mined. CleanSpark also noted 6,671 BTC mined for the calendar year and it’s currently holding 2,575 BTC ($103 million at $40,000 per BTC).

While Hut 8 has a considerably larger BTC holding, CleanSpark has considerably higher efficiency mining operations. That’s why I like the look of CleanSpark in another bull market cycle and heading into a halvening event in April.

If the price continues higher for bitcoin, and CleanSpark can continue to improve efficiency and maintain this as a lower cost to mine (same and/or lower energy usage), then we could see it exploding higher in tow with bitcoin’s price.

Again, you don’t need me to tell you what kind of upside bitcoin at $1 million would be. But even if it was bitcoin over $100,000 then we’re looking at a fast rise in revenue and the value of CleanSpark as well.

Risks

Like Hut 8, the main risks here are bitcoin’s price – if it crashes, so does the value of CleanSpark. If after the halvening event its efficiency falls, and its mining falls harder than expected, it too could drag the price lower, particularly if bitcoin’s price hasn’t yet moved.

Volatility is the same as Hut 8. It will rise and fall sharply on any movement in bitcoin’s price.

Here you just need to understand it’s a significant asymmetrical play. The idea being a little capital risked for gigantic potential upside. But also that if things move against us in a way that burns the house down, you’re not out on your backside if the stock halves in price.

By complementing Hut 8, I think CleanSpark makes the perfect second addition to the bitcoin miners we will now have in our buy list.

Action to take: BUY CleanSpark (NASDAQ:CLSK)

Market cap: 1.7 billion

Current price (20.12.23): US$10.49

Buy up to $12

Set a stop loss at $5

PS We’ve got a bunch of new readers coming to Small Cap Investigator, as such we’ve put your latest recommendations, Hut 8 and CleanSpark into a special report, and also our top four rated crypto into another special report. Just to let you know these are available in the special reports section of your members login now also.

Big breakthroughs

In May this year, two scientists guided a small probe down a borehole half a mile beneath the ground of the Lorraine mining basin in northeastern France.

They were looking for fossil fuels, but instead discovered a resource that could be potentially much more valuable and certainly more important in global efforts to tackle the climate crisis: natural hydrogen.

Although Jacques Pironon and Phillipe De Donato, both directors of research at France’s National Centre of Scientific Research, were in the Lorraine basin to test methane levels in the soil, they had accidentally discovered between 46 million to 260 million metric tonnes of so-called “white” hydrogen – i.e. hydrogen that’s naturally produced or present in the Earth’s crust.

This is potentially the largest accumulation of natural hydrogen discovered to date. By comparison, around 70 million metric tonnes of hydrogen is produced commercially worldwide each year.

In the immediate aftermath of the Lorraine discovery, Switzerland joined the search, finding natural hydrogen in the Graubünden canton in spring before probing rocks in Valais for further deposits in the summer.

This feverish interest in the gas is surprising, given that, up until relatively recently, it was commonly accepted that naturally-occurring hydrogen simply didn’t exist – or, at least, not in places that humans could reach, or in large accumulations.

But in 2012, a discovery was made in Bourakébougou in the West African nation of Mali. A borehole drilled for a well decades earlier was found to be emitting almost pure natural hydrogen.

Since then, geologists have increasingly been experimenting with extracting supplies of this natural gas from beneath the Earth’s surface.

Unlike fossil fuel stores, which take millions of years to form, natural hydrogen is continuously replenished.

And unlike hydrogen produced from natural gas or wind or solar power via electrolysis – “grey” and “green” hydrogen, respectively – its natural counterpart requires no water and little energy to extract while taking up very little land.

These advantages make natural hydrogen a much cheaper resource than green hydrogen, certainly. The cost of natural hydrogen is estimated at €0.50 per kilogram, while green hydrogen costs roughly €5 per kilogram.

According to estimates, there could be tens of billions of megatonnes of white hydrogen globally, vastly more than the 100 million tonnes a year of hydrogen that is currently produced and the 500 million tonnes predicted to be produced annually by 2050.

Although most natural hydrogen is likely to be found in unreachable locations, either too deep or too far offshore, geologists state that if just 1% was recoverable, that would be enough hydrogen to keep the world going for at least two centuries, even if there was a surge in demand for hydrogen.

Already deposits have already been discovered in Australia, eastern Europe, Oman, Spain and the US, as well as in Mali, France and Switzerland.

However, challenges remain, not least in finding the stuff. Fairy circles, which appear across landscapes where hydrogen is present, are a giveaway, but in hundreds of other locations hydrogen has been seeping unnoticed out of the ground for decades.

It is also not yet clear exactly how white hydrogen forms deep within the Earth, how it migrates to the surface and how best to extract it. No one really knows yet whether it will really be commercially exploitable. Certainly, white hydrogen could quickly become more expensive if large deposits require deeper drilling.

But what is clear is that more and more companies are now entering the space, all eying up a natural hydrogen industry that could be worth $75 billion industry by 2030.

Koloma, a US-based natural hydrogen company, recently received $91 million from a group that includes Bill Gates’ Breakthrough Energy Ventures.

In Australia, Gold Hydrogen, an independent energy company, is digging for natural hydrogen near Adelaide after unearthing historical papers from two oil wells drilled in the 1930s that showed vast amounts of high-purity hydrogen in the area.

In northeast Spain, exploration company Helios Aragón says it has located a reservoir of over one million tonnes of hydrogen, which it aims to start drilling in 2024.

A British company, Getech, is adapting software developed to find oil to locate hydrogen deposits.

Up until now, the industry has largely been the preserve of small companies, venture capital funds and individuals with deep pockets and an appetite for risk. But it’s likely that bigger companies will soon start to put larger amounts of money in, accelerating the development of natural hydrogen significantly.

Back in France, Pironon and De Donato’s next steps are to drill down to 3,000 metres to get a clearer idea of exactly how much white hydrogen there is.

But, certainly, the find in Lorraine has added to a trail of clues that a holy grail of clean energy may be lying in the earth for the taking.

There’s a long way to go, but it seems that the discovery in Lorraine – once one of western Europe’s key coal producers – could just become the epicentre of a new white hydrogen industry.

Buy List update

James:

Ashtead Technology Holdings PLC (AIM: AT)

Subsea equipment rental company Ashtead Technology Holdings, recommended at 374p in the July issue of Small Cap Investigator, has risen around 30% over the last month to trade at 610p at the time of writing, putting it 63% up in the model portfolio.

Ashtead has a history of supplying subsea services to the oil and gas sector but has diversified into the fast-growing offshore wind market.

As we wrote in the last issue, the stock jumped at the end of November, after the company announced it had expanded its mechanical solutions service offering with the acquisition of ACE Winches for £53.5 million in cash.

Ashtead said the deal is expected to be “materially” earnings enhancing in FY2024 and beyond. Return on invested capital will also be “materially” ahead of the group’s weighted average cost of capital in year one, it added.

The stock remains a HOLD while it trades above 395p.

European Metals Holdings (AIM: EMH)

At the time of writing, European Metals Holdings (AIM: EMH) is trading around 25.50p, 22.26% down in the model portfolio, with the stock falling 15% over the last month.

As you’ll recall, European Metals owns the Cinovec lithium asset in the Czech Republic that is primed to become the largest hard-rock lithium deposit in Europe – a region where there is little domestic raw material production and a region with a huge demand as it battles to achieve a carbon-neutral future.

The Cinovec project has significant support from the Czech government and has been deemed strategic by the EU, bolstered by a €50 million grant. What’s more, it is anticipated to receive continued financial and legislative backing.

Of course, investors have seen the price of lithium fall by around 80% this calendar year on the back of increasing supply and inventory drawdowns at cathode companies and concerns over demand for electric vehicles (EVs).

But there are certainly reasons for optimism in the lithium sector as demand could materially exceed supply as soon as 2025.

In the case of European Metals Holdings, the company is expected to deliver a definitive feasibility study (DFS) on the project by year-end.

Although prices have moved against us, I think we can remain extremely optimistic – given the project’s importance to the EU’s lithium production ambitions – about the project’s progress and the forthcoming final investment decision.

The stock remains a BUY below its 45p buy limit.

Central Asia Metals (AIM: CAML)

Central Asia Metals (AIM: CAML), a mining company with operations in Kazakhstan and North Macedonia, has risen 10% over the last month to 182p at the time of writing, still leaving it 34% underwater in the model portfolio.

The group’s principal business activities are the production of copper at its Kounrad operations in Kazakhstan and the production of lead, zinc, and silver at its Sasa operations in North Macedonia.

Amid a lack of news, the stock continues to take direction from a copper market, where mine closures and disruptions have started to change the landscape for copper supplies. This has prompted analysts to lower their forecasts for surpluses in a positive signal for prices of the industrial metal.

Copper prices on the London Metal Exchange are hovering below recent four-month highs of $8,640 a metric tonne seen on 1 December, partly due to Anglo American (AAL.L) lowering its production guidance.

Macquarie Bank now expects copper market surpluses of 100,000 and 287,000 tonnes for 2024 and 2025 respectively, down from previous forecasts of 203,000 and 369,000 tonnes.

With CAML proceeding well operationally, the stock remains a BUY under 310p.

Foresight Sustainable Forestry Company (LON: FSF)

Foresight Sustainable Forestry Company (LON: FSF), which invests in UK forestry and afforestation assets, has fallen 11% over the last month to 60.20p at the time of writing, putting it around 44% down in the portfolio.

In announcing its annual results for the year ended 30 September 2023, FSF said a decline in land values was the main reason behind a 6.3% decline in net asset value (NAV) for the year.

“The board is currently acutely aware that the company’s shares have fallen and moved to a discount to NAV over the last six months,” said FSF Chair Richard Davidson.

“The share price move during the period aligns with the broader pattern in the real assets investment trust sector, which has shown a notable sensitivity to higher interest rates,” said Dawson.

The share price would return to levels that “reflect the development of the company’s NAV and the company’s outlook and prospects more generally in its core markets of land, natural capital, timber and voluntary carbon,” he added.

As we wrote last month, although the performance has been poor, we’re certainly willing to give FSF more time. What we said last month bears repeating:

Remember, there is a global shortage of sustainably sourced timber. Current World Bank data shows that there is a base of billion cubic metres of global timber supply deficit, with the numbers expected to triple by 2050.

Meanwhile, the forestry situation in the UK is particularly poor, with only 13% of the country forested compared to an average of 45-48% across the rest of Europe.

Through expansive afforestation projects and sustainable timber production, FSF – the only forestry and natural resource fund on the London Stock Exchange – is tackling the global long-term structural supply imbalance of timber, as well as bolstering the UK’s timber supply.

Since its initial public offering (IPO) two years ago, FSF has already invested in over 1.5 million trees at six new forests, which adds up to around 289,500 tonnes of sustainable timber for sale, while it also plans on planting circa 9 million trees between 2023 and 2025.

In addition to timber, FSF is on track to produce 1 million carbon credits that are produced when trees are planted, removing carbon from the atmosphere. Demand for carbon credits is predicted to increase a hundredfold by 2050.

FSF remains a BUY under 150p.

Global X Lithium & Battery Tech UCITS ETF (LON: LITG)

Global X Lithium & Battery Tech UCITS ETF (LON: LITG) has fallen 4% over the month to trade last at around £6.95 at the time of writing, putting it around 22% below our £8.96 entry price.

The exchange-traded fund (ETF) invests in the full lithium cycle, from mining and refining the metal through battery production. It seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Global Lithium Index.

LITG certainly provides asset diversification across different parts of the lithium supply chain, which can provide cushioning against lithium price volatility. For example, if prices fall, that’s a negative for producers but a positive for companies that buy lithium to make value-added products.

By owning mining, refinery and battery production companies in the fund, Global X has its fingers in multiple parts of the lithium industry.

As we wrote last month, it should certainly benefit from heavy demand for lithium. After all, without lithium, we can’t build EVs or have the green future that countries are demanding.

LITG looks considerably oversold. As such, it remains a BUY.

Newmont Corporation (NYSE: NEM)

At the time of writing, Newmont Corporation (NYSE: NEM), the world’s largest gold miner, is trading around at $41, up around 11% on the month. The stock is now 37% below our $65.39 entry point.

As you’ll recall, Newmont has now concluded the AU$26.2 billion takeover of Newcrest Mining, leading to the formation of what it claims to be the globe’s leading gold miner.

The merged entity will also have a “robust” production of copper, stated Newmont.

But the stock has largely moved on the gold market, where prices recently hit an all-time high above $2,110 per troy ounce.

Bullion’s ascent has been driven by a weakening dollar as investor confidence has grown that the US central bank, the Federal Reserve, will lower borrowing costs early next year.

Certainly, the outlook for potentially lower interest rates bodes well for gold, given that it makes returns on the yellow metal appear more attractive.

Newmont remains a BUY under $100.

DS Smith (LON: SMDS)

Recycled-content paperboard and packaging producer DS Smith has traded flat over the last month to around 311.60p at the time of writing, now around 1.7% below our entry price.

Earlier this month, the company issued half-year results that paint a rather downbeat picture that points to a deteriorating macro-economic environment.

The London-listed company reported a 15% drop in half-year pre-tax profit to £268 million in line with analyst expectations, while like-for-like box volumes fell by 4.7%.

DS Smith said the macro-economic environment remained challenging, but there were signs of improvement.

Despite the headwinds, an interim dividend of 6p is being maintained.

“Encouragingly, with destocking amongst our customers now largely over, we are seeing signs of volume improvement, with the second quarter performance being better than the first,” the company said in a statement.

“Despite the fall in volume, our margins have actually gone up slightly over the last year,” said CEO Miles Roberts, who also announced his plans to retire after 13 years.

The company said it remains on track to deliver against full-year expectations, with sluggish sales as a consequence of customers having been savvy in reducing their own inventory.

With this destocking phase now over and signs of volume improvement now emerging, the stock remains a BUY.

Kraneshares MSCI China Clean Technology Index UCITS ETF (LON: KGRN)

The Kraneshares MSCI China Clean Technology Index UCITS ETF, recommended at $24.83 on 12 October, the day it listed on the LSE, was last seen at $21.16, putting it 14% down in the model portfolio.

KGRN, which tracks the MSCI China IMI Environment 10/40 Index, is the only UK-listed ETF to specifically tap into China’s cleantech industries.

China’s state-guided economy spent nearly $80 billion on clean-energy manufacturing last year, around 90% of all such investment worldwide, according to BloombergNEF estimates.

Not only is China the world’s largest manufacturer of solar panels and wind turbine, but it is also installing green power domestically at a rate the world has never seen.

Indeed, this year alone, China built enough solar, wind, hydro and nuclear capacity to cover the entire electricity consumption of France. Next year, we may even see China’s first ever drop in emissions from the power sector.

The ETF is a BUY below $26.83.

NET Power (NYSE: NPWR)

We recommended carbon capture company NET Power at $9.49 in the last issue of Small Cap Investigator. At the time of writing, it is fetching $10.05, putting it 5.90% up in the model portfolio.

As you’ll recall, NET Power has developed a natural-gas power plant that makes it easy to capture carbon dioxide released by the burning of natural gas.

Since the recommendation at the end of November, NET Power has announced a new strategic agreement with Lummus Technology – a company providing process technologies – to design and supply recuperative heat exchangers (HXR) for NET Power’s power generation process.

The HXR recovers energy from the turboexpander exhaust and air separation unit to reheat recirculated CO2, making it one of the most important equipment components in the NET Power Cycle.

The stock remains a BUY up to $11.

Sam:

Rolls-Royce (LON: RR)

Rolls-Royce has been in our buy list for quite some time now. It is one of the larger companies that we have. This is mainly because when it first found its way into our buy list, we occasionally looked at larger stocks.

However, the initial recommendation came right before the world’s market capitulated and industries like aerospace and aviation took an absolute pummelling on the market. So much so that in October 2020, Rolls-Royce undertook a rights issue to shore up their balance sheet and ensure it could keep the company’s head above water.

We recommended that rights issues at the time for investors who could participate as the long-term view of Rolls-Royce was still strong. Those rights were at 32 pence and those eligible were able to buy ten for every three Rolls-Royce shares held. It was a great deal.

Just how great a deal is now evident, with Rolls-Royce now trading up around £2.90. That means not only has Rolls-Royce almost completely bounced back from its price lows of 2020, but those rights-issued stocks are actually sitting on a gain of 806%.

Of course, when you take into account the initial entry, the overall gain comes back down a bit. But it goes to show that the period of 2020 was an anomaly of the highest magnitude, and that a company as diversified, robust and important to British industry like Rolls-Royce can still deliver long-term value potential.

Our original entry price is almost to break even, and when you factor in the rights, it’s a tidy gain. We are only tracking the price of our original entry in the buy list, but we’d expect that if you’d taken up the rights issue as recommended, you’ll have a handy profit on Rolls-Royce in your brokerage account.

Cyngn (NASDAQ: CYN)

Cyngn has been on a wild rollercoaster in the last few weeks. At one point, the stock jumped over 120% in a day off the back of a new patent announcement.

The very next day, the company decided to announce a capital raise at just 15 cents, over half of what the stock had risen to the day prior.

As you’d expect, the stock then tanked down to the capital raise price and has bounced off that low in the days after. It’s still a big whack to our initial entry and sees the position in the red.

Having said that, what the patent announcement shows us is that this is a stock that, in the blink of an eye, can explode out of the gates and recover the red in an instant. That’s why we got into the stock – we were acutely aware of the financial position and the explosive potential that it brings when it has a tailwind behind it.

We stick with the stock and expect that a series of positive announcements, without a ridiculously priced capital raise, will see us quickly return into the black.

Argo Blockchain (LON: ARB)

Argo is still languishing deep in the red for us for the time being. However, it is still showing some signs of life, particularly as we look to step into the next big crypto bull market.

The company has kept afloat and even late November appointed a new CEO, the former Head of CBOE Digital, Thomas Chippas. It looks like a solid appointment. Argo is getting itself into a position where if we do see the expected hard rally and bull market in bitcoin and crypto, then Argo can recover into a profit position and reach its former glory highs again.

With that in mind, and at least looking to a bull market again, we have Argo as an active buy recommendation. And if you haven’t got any, then like the newly introduced bitcoin miners, it’s worth adding to your portfolio. If you’ve got Argo already and are showing red on the return so far, it’s a good chance now to add to your holding, reduce that cost base and look for Argo to strongly perform in a new bull market for bitcoin, which we expect to hit in 2024.

But we will bring its buy limit down to 16p from here.

Inside the lives of James and Sam

Sam:

It’s Christmas time which means a bit of time off, a bit of time with family and a bit of time in front of the BBQ!

I only found one problem. I’ve got the Christmas stuff sorted, check. I’ve got the family stuff sorted, check. My Dad is visiting for Xmas, check. The BBQ however… slight problem.

I didn’t have one.

When we moved from the UK, I ditched my old crappy BBQ but I hadn’t got around to getting another one yet. That needed to change as I plan on doing a big seafood Xmas dinner on the BBQ.

So I jumped online and found myself a new “barbie”. I opted for a new Weber Genesis II. Big enough for my needs and, let’s face it, there was a great discount on Weber BBQs on the shop I found. In fact, it was around at a 28% discount.

The BBQ arrived. But like everything these days, that wasn’t the end of it. Nope. I had to put it together didn’t I?

Here’s the before shot…

And about an hour and a bit later, the after shot…

I am pretty happy with it to say the least. But I was also curious as to whether Weber was a listed company or not. It is, after all, a huge company in the BBQ world.

The thing is, it was public, but only fleetingly. The company listed on the Nasdaq in August 2021…

Oh dear. I don’t think it could have picked a worse time to list. Trading under the ticker WEBR, its IPO was at $14 (with an implied valuation around $5 billion) but the stock traded at the open up at $17.

All good so far… until… by the end of 2021 the stock was under $12. And by October 2022, it was closer to $5. And then by December 2022 it was taken private again in a $3.7 billion deal with private equity company BDT Capital.

Literally a blink and you’ll miss it stock listing. And a nice little 26% discount for BDT Capital.

Yes, BDT got a steal I reckon. But I’m laughing last because of the two of us, it was me who got the bigger discount on the Weber purchase!

James:

I’ve long talked up the advantages of driving an electric car, though one of their plus points – their nippiness – helped land me in trouble one evening in the late summer.

That’s when, completely unbeknown to me, I was caught speeding by a camera on the side of the A316 in west London.

I had been driving back from the west country, where my family and I had spent a week’s staycation, when the camera caught us doing a little over the permitted 40mph.

Although I don’t think I was flashed and can’t recall specifically speeding, I do remember the roads opening up either side of Chiswick Bridge so I obviously took full advantage – after a particularly slow journey up to that point.

A few weeks later I received a stern letter from the police that “invited” me to attend a national speed awareness course (NCAS) as an alternative to penalty points and a fine – an invitation I accepted by way of forking out £95 to spend nearly three hours with a trainer and around a dozen other similarly shamed drivers on a Zoom video call a week or so ago.

I can’t say I enjoyed the course but neither can I say it was a terrible experience. It certainly held my attention and was, at times, even quite enlightening. There was plenty to take on board.

Some of the things that I didn’t know (or, more likely, didn’t remember from doing my driving test back in 1995) included the fact that streetlights dictate a 30mph limit on a road (unless indicated otherwise), a dual carriageway is identified by a central barrier rather than the number of lanes and, statistically, motorways are by far the safest roads.

Moreover, going 35mph in a 30mph zone requires an extra 27ft to stop, potentially making the difference between injuring someone and causing a fatality.

The trainer also encouraged us all to think about the real reasons we feel the need to speed. I acknowledged that I tend to speed when running late or when stressed or distracted either by other occupants in the car or by other drivers nearby. I was told that practising “commentary driving” – i.e. noting the various potential hazards on the road out loud as you drive – helps enhance concentration.

Although it’s only been just over a week since I attended the course, I have already felt pangs of guilt when I’ve felt tempted to edge the speedo up a little, so the course has so far been beneficial. I certainly think it was a wise decision to take the course rather than accepting a fine and points.

Perhaps that’s why courses like the one I attended are thriving. Last year saw a record number of participants, with 1,478,444 drivers opting to undertake a NCAS instead of accumulating points and risking a ban. The figures have more than tripled since 2010, when a little more than 467,000 drivers attended a course.

It’s certainly big business: 1.478 million times £95 equates to £140.1 million just generated from courses last year alone.

On the other hand, as we were told on the course, the national cost of all road traffic collisions is £36 billion per year, so you like to think the courses serve their purpose.

According to a government study, after taking a speed awareness course, those who had participated were less likely to re-offend in the following three years than those who paid a fine and had penalty points added to their licence.

In fact, three years after completing the NSAC, there was a 6-18% estimated reduction in the number of drivers caught speeding again, the study showed.

Of course, when you consider that around 50% of drivers caught speeding take three penalty points and a £100 fine then you can start to appreciate just how much revenue speed cameras generate in total.

You can certainly do worse than invest in speed cameras, that’s for sure. The global high-speed camera market size was pegged at $3.78 billion in 2022 but is poised to reach a valuation of $6.39 billion by 2031.

The market is also seemingly ripe for disruption for any entrepreneur looking to shake things up a little, but if you want to invest in a company already in the business then you could do worse than check out Verra Mobility (NASDAQ: VRRM).

Verra is a US-based smart mobility technology solutions company with a presence in over 15 countries. In addition to speed cameras, the company also provides automated toll and violations management and title and registration services to rental dealerships.

The firm has grown rapidly since going public in 2018. This is not only due to sales of its road safety hardware but also after closing several major acquisitions.

For the most recent Q3 quarter, VRRM saw its revenue increase 6% to $209.9 million, while adjusted EBITDA (earnings before interest, taxes, depreciation, and amortisation) rose 7% to $97.4 million from $90 million a year ago. Year to date the stock is up nearly 60%.

This is certainly a stock I’ll keep an eye on, potentially with a view to recouping my £95 back at the very least.

Crypto Corner

There is no doubt in my mind that we’re entering another crypto bull market cycle. And as it stands, that’s looking increasingly like it’s coming in 2024.

With major catalysts on the horizon, like the approval of massive spot bitcoin exchange-traded (ETFs) in the US and the impending bitcoin halvening in roughly April next year, we’re looking at a supply and demand imbalance that could ignite the market.

And as we’ve seen in previous cycles, if bitcoin runs hard, the rest of the market tends to follow.

That’s no guarantee, of course, but another massive cycle could leave the previous ones for dust. That means I think we need to help with some further information about what you should be looking at in this market as we approach another potentially game-changing bull market cycle.

So this month, you’ll find below four top-rated crypto that we think you should be familiar with in anticipation of what we see coming. Information about each, what they do and why they’re important is all below.

I also suggest that you get your hands on a copy of my latest book, “The Crypto Handbook” which, if you haven’t read it already, is a must before doing anything in this market and before the bull market ignites.

A free digital copy is available to you under the “Special Reports” section of your members log-in. So read that, and then check out our top four-rated crypto for 2024 below…

#1 top-rated crypto for 2024: bitcoin (BTC)

In 2009, a white paper was published to a cryptography mailing list. The title of the white paper was “Bitcoin: A Peer-to-Peer Electronic Cash System”. Its author was the mysterious and elusive Satoshi Nakamoto.

The core premise of this electronic cash system was an online payment system that would “allow online payments to be sent directly from one party to another without going through a financial institution”.

That sentence is incredibly important to everything else I’m about to explain and tell you about in this explanation of why bitcoin is our #1-ranked crypto for the new bull market.

As you continue to read on, I want you to keep this in the back of your mind: bitcoin, in its first instance, is to be a payments system that avoids going through financial institutions.

It’s an alternative financial system to the one we currently use to buy and sell things, transfer money around the world, and build our financial wealth.

The white paper by Nakamoto is a must-read for anyone thinking about involving themselves in bitcoin. I implore you to read it after you’ve read this report and before you consider getting bitcoin for yourself.

It’s only eight pages long (plus references) and is actually quite simple to read and understand. This is the foundation – the beginning of bitcoin. And it’s where everything took off.

As Nakamoto explains in the white paper, it is an electronic coin, by definition, which is just a “chain of digital signatures”. For example, I transfer you one bitcoin and that creates a digital signature. It’s then secured with cryptography known as a “hash”.

However, this new digital signature is added to a whole long line of digital signatures from all the previous bitcoin movements that have ever taken place. Think of it as a giant notebook that holds every record of every transaction ever made.

When a new transaction is added to the notebook, the wider community of “nodes” (which I’ll get to shortly) verifies this new transaction and it’s confirmed. In approving the latest transaction, it’s assumed instantly that every record that comes before it is also approved (which it is).

Hence, this distributed leger – known as the blockchain – is one giant automated verification system that proves and confirms every single bitcoin transaction that has and will ever take place. This verification process, known as “confirmation”, underpins the entire bitcoin system.

It also then enables transactions, like the payment of goods and services.

Bitcoin is also decentralised in this manner. It doesn’t operate with a centralised authority and its purpose is to avoid that outcome. Its features are all hardcoded into bitcoin’s core code. Trust is in the mathematics and code that govern bitcoin.

Anyone operating a bitcoin wallet or buying, spending, or mining bitcoin is part of this decentralised network. This decentralised nature, and the underpinning technology of blockchain, and the confirmation process called “proof-of-work” bring reliability and stability to the system.

Now, this can get complex, but it’s important at this point to know that the technology works. It is reliable and has never failed since its genesis in 2009.

The digital gold rush

Since its inception, bitcoin has always been convertible into fiat currency – in particular US dollars. In early 2010, a bitcoin was “worth” around three cents – a bitcoin block would be worth around US$15 (50 BTC reward).

At this point, in late 2010, I first began to get curious about this “bitcoin thing”. I couldn’t quite get my head around the fact that you could use a computer at home to “mine” this digital currency and that it was worth money.

Surely that wasn’t possible. You could literally make money out of thin air. I continued to watch it, trying to figure out how to set up my own “mining rig” to mine bitcoin.

But building a computer with the necessary mining graphics processing units (GPUs), and then understanding the programming language to mine bitcoin, all just became too hard. The mining would have to wait.

In 2011, though, I introduced a colleague to bitcoin. We considered putting in $1,500 each and buying a high-spec computer to have a crack at it.

But then, after doing the calculations on cost, energy expenditure and time required to achieve one block, it didn’t make sense economically. More miners were coming online, and the probability of mining a block was reducing all the time.

We also thought about just buying $1,500 worth of bitcoin. However, even in 2011, that proved very hard. Getting small amounts wasn’t too bad. You could peer-to-peer buy it, but that posed its own difficulties and risks. Not something I enjoyed really. Also, by this stage, bitcoin had spiked to a price of $10. This was from just cents months earlier.

This had all the hallmarks of a bubble. We decided to pass on anything more and save our money for stocks instead. We were vindicated (short-term) as bitcoin rose north of $20 by June and then tumbled back to around $2 by November.

1,500 bitcoin would be nice today. But in all errors of judgement, or in this case, missed opportunities, there is always a lesson to be learned. In my case, it was a failure to appreciate not just how impactful this new technology could be but also how broken the traditional system was.

How bitcoin gets to $1 million

By mid-2011, bitcoin was already becoming harder to mine. People were starting to use bitcoin-dedicated rigs (called ASICs) with eight, 12 or 24 GPUs.

In short, it was an arms race for miners – the more GPU power you had, the better at mining you were. Through 2011, bitcoin, and bitcoin mining, was like a gold rush. There were even a few businesses that began accepting payments in bitcoin.

Things were moving fast.

In late 2013, when bitcoin hit an equivalent price of US$1,242, the world stood up and took notice. The same day bitcoin hit US$1,242, the spot price for physical gold was US$1,240.

This digital currency was worth more than gold. For many, it was digital gold. This has been a strong narrative of bitcoin ever since – that it is a store of value, not a currency. I argue that it’s both.

Early in 2014, I was a guest on The Rick Amato Show on the One America News Network TV station. Amato was interviewing me as their technology expert. Little did I know that they were also bringing in (at the time a nominee for Governor of California and the Mayor of Laguna Hills) Andrew Blount.

I was explaining the long-term benefits of bitcoin as an alternative monetary system, that it could be used to pay for a whole range of goods and services in time. We had a bit of a debate as to the legitimacy of bitcoin.

Blount likened bitcoin to bubble gum wrappers at the time. That was all they were worth, in his eyes. He forecast that, by the end of 2014, bitcoin wouldn’t exist. As you’d expect, I disagreed with him.

My position was, and still is, that bitcoin will be around far longer than either he or I would be alive. In fact, I personally don’t envisage a day in the future when there isn’t bitcoin.

I’m also of the view that the fiat currency value of bitcoin is unimportant for the future. It matters little long-term what bitcoin is worth in USD, CNY, AUD, GBP or whatever currency you choose.

Presumably one day, you will be able to freely spend bitcoin as you do the currency you’re paid your wages in. However, there is a transitional period to this day where the fiat value is important, giving us perspective as to the purchasing power of bitcoin. For example, while the current price of bitcoin is US$40,000, long-term, I can see it being the equivalent of US$1 million and more.

That’s not a stretch, considering that when I first started covering bitcoin for Southbank Investment Research it was at just US$747. The likelihood of that outcome is enhanced if we continue to see more severe, ongoing financial turmoil in economies around the world. But there is also an increasing demand for bitcoin from the entire global wealth system.

The existing expectation is that the US will greenlight as many as 12 new spot bitcoin exchange-traded funds (ETFs).

That’s bitcoin ETFs from the likes of BlackRock (through iShares), VanEck, Fidelity, WisdomTree, Invesco, Ark Invest, Greyscale and a slew of others.

Combined, these giants manage tens of trillions in assets. Regulated, listed, bitcoin spot ETFs could very well see tens of billions of dollars flowing into these funds within weeks of their launch.

For some comparison, there’s around 34 gold ETFs trading on the US markets with combined assets under management (AUM) of around $115 billion. That same level of capital flow to bitcoin ETFs, which we expect there will be, works out at around 14% of bitcoin’s current market cap.

However, that’s based on the current bitcoin supply, which is at 19.57 million bitcoin.

We know, however, that a lot of bitcoin is lost and untouched in places where it shall never return. We also know that 70% of bitcoin hasn’t moved in over a year. That means hodlers aren’t easily willing to part with their bitcoin.

The liquid supply of bitcoin in the market is only around 1.3 million BTC.

At current prices, that means if the BlackRock bitcoin ETF, for example, were to see capital inflows of $55 billion (which is not crazy considering the largest gold ETF is $57 billion of AUM) then it would need to hold 1.3 million bitcoin.

In other words, for a $55 billion bitcoin ETF to fill its coffers with the necessary bitcoin, it would need to buy all liquid bitcoin in the market.

That’s just one ETF. What about the other 11 that are expected to be approved? Simply put, there’d be no bitcoin left.

Unless… the price moves high enough that the 70% of hodlers are willing to let some of that bitcoin go.

How high? Well, we simply don’t know. But for those who might have bought the top of the market at $69,000, then I’m guessing multiples higher than that. And if we’re only looking at around 1.3 million liquid bitcoin available, and a market cap of over $820 billion, we’re already looking at value-per-liquid bitcoin of over $630,000 – the leap to $1 million from there isn’t far.

The reality is that if these ETFs are approved, the capital flows and there just isn’t enough bitcoin to supply the demand, we would expect this to force prices higher.

Then predictions of $1 million per bitcoin, which have come from the likes of Cathie Wood (who’s ARK Invest is one of the ETF applicants) aren’t as wild as you might think.

And just to make matters even tighter – in April, the bitcoin block reward is set to drop from its current 6.25 BTC per block to 3.125. That means the new bitcoin supply hitting the market is cut in half.

I could go on and on, but the point is that bitcoin today looks primed for another big cycle, perhaps one that smashes all the others to pieces.

The demand-supply story building is powerful, and that imbalance with TradFi companies all ready to dive in makes it our #1 top-rated crypto for a new bull market cycle.

#2 top-rated crypto for 2024: Ethereum (ETH)

Ethereum and its native token, Ether (ETH), are just as important as bitcoin, though for different reasons.

“Cryptocurrency” isn’t quite the right term to describe Ethereum. That’s because Ethereum isn’t really a “currency” at all – it was never intended to be a unit of exchange.

Ethereum and bitcoin have entirely different goals. Instead, Ethereum is an entirely new form of digital infrastructure. It is quickly becoming the foundation for an entire new generation of digital assets, digital businesses and digital wealth that’s being built on the Ethereum blockchain.

The new internet

So, what actually is Ethereum? Think of Ethereum as a better version of the internet – the second internet, the world’s computer – the way the internet should have been created in the first place.

To understand just how significant Ethereum is, we need to go back a few decades. In the late 1980s, the World Wide Web (WWW) began to proliferate around the globe. Inventor Sir Tim Berners-Lee had developed a globally interlinked information system that existed on “the internet”.

By 1990, a more formal version of the WWW was in development. This resulted in the publishing of the first-ever “webpage” on 20 December 1990. In just 30 years, the WWW and internet have gone from obscurity to becoming almost as important as electricity.

I say “almost as important” because, without electricity, there is no power to make the internet and the WWW work. The energy source that powers the internet – electricity – is as important to its existence as all the hardware and software that actually make it work.

Electricity is the fuel of the internet – it’s vital. Remember this notion – the “energy” of the internet – as it will help you understand a vital concept about Ethereum.

It’s no exaggeration to say that the internet powers the world. And it has created an untold number of millionaires and billionaires, too. If it wasn’t for the internet, Mark Zuckerberg couldn’t have created Facebook, and he certainly wouldn’t be at the helm of a company worth over $800 billion.

Ethereum is a global platform that future industry will be built upon – it is the cornerstone of what we call “Web3”.

While I believe that bitcoin could be the future of finance systems, I also believe that Ethereum is the future of the new internet. Its native token, ETH, is important as a “fuel” for the future digital world, for which Ethereum is the Web3 infrastructure.

Another way to think of ETH is a bit like “digital oil”. Oil was the lifeblood of economic growth throughout the 20th century. To do almost anything – whether transporting goods or manufacturing products – required oil.

I believe that Ethereum has the potential to be the foundation of every major new digital – and even physical – application for the next 100 years, and if the ETH token is the “energy” source powering all that, it puts the whole infrastructure in prime position for another big crypto market bull run.

Think about a city full of skyscrapers, with thousands of companies and millions of workers. Ethereum is the land and the buildings. ETH – the coin that powers the Ethereum blockchain – is the same as the electricity that powers the city.

While I view Ethereum as the world’s most important system for future digital business, we also need to make sure that we don’t dismiss this as just some kind of software platform.

Ethereum is developing with such momentum that it’s almost taking on its own life force.

There’s an entire ecosystem of new applications based on it. Think about this like the Apple App Store. On its very first day of existence, it was populated by just a few apps. But it wasn’t long before developers began to create more apps, which quickly created the thriving ecosystem of applications we see today.

The more enterprises build and develop on Ethereum, the more powerful it becomes. And in order for Ethereum to flourish, it requires “energy”. As the Ethereum white paper explains, ETH is the internal crypto fuel of Ethereum and is used to pay transaction fees.

ETH is to Ethereum what electricity is to the internet.

It is more like a commodity – a resource that the entire system relies on but which is in limited supply. As Ethereum grows in size and stature, and begins to attract major global corporations, the value of its fuel, ETH, could rise… and rise… and rise. The bigger it gets, the more it needs ether.

What makes me even more confident about Ethereum is that major businesses are already getting involved. Early on in Ethereum’s journey, the Enterprise Ethereum Alliance was formed. This is an “alliance” between giants of the corporate world, such as Microsoft, Intel, JP Morgan, BNY Mellon, BP, ING, Thomson Reuters and others.

And now today, we know that big traditional finance is very keen on Ethereum’s development and decentralised finance (DeFi) applications built on Ethereum. It’s also why, not long after its bitcoin ETF is approved, it is expected that BlackRock will seek approval for its Ethereum spot ETF.

Today, the Ethereum ecosystem is growing at a rapid pace. Everything from FinTech to decentralised computing, gaming and gambling – and even something as kitsch as generative NFT – exist on Ethereum’s blockchain.

It could be the world’s computer, decentralised and economically tilted towards users, not a few large, siloed organisations. This is why I think now is the time to get involved in Ethereum and understand just how big the potential here could be.

With its long-standing history and incredible development as an infrastructure layer for crypto, Ethereum is my second highly rated crypto that I think is primed for another bull market.

#3 top-rated crypto for 2024: Cosmos (ATOM)

Cosmos and its ATOM token promise to be the “internet of blockchains”. Its view is to connect and allow for blockchains to talk to and work with each other.

In a sense, it is like the internet protocols that connect everything, and also potentially the WWW but for crypto.

In the words of the project, Cosmos is an ecosystem of blockchains that can scale and interoperate with each other.

Before Cosmos, blockchains were siloed and unable to communicate with each other. They were hard to build and could only handle a small number of transactions per second. Cosmos solves these problems with a new technical vision. The view is to enable developers to build applications using a set of blockchains that speak to other blockchains.

The key element of connecting the blockchains is a protocol it calls Inter-Blockchain Communication (IBC). You can think of this as being like the transport layer of the internet.

The way IBC interacts with different kinds of blockchains gets technically heavy. The project goes into some detail about the use of bonding tokens and token vouchers as well as “peg-zones” for probabilistic-finality chains like bitcoin, which is a proof-of-work blockchain. All a bit much? It is.

But it means that Cosmos functions as Grand Central Station for potentially all other crypto trains and their blockchain rails. The important part of IBC that I see, however, is the idea of using hubs and zones.

As Cosmos notes, let’s say there are 100 blockchains. To connect IBC to every blockchain, every blockchain has to connect to every other. That’s 4,950 connections. Using hubs, it is able to let blockchains connect to other blockchains that are connected to that particular hub, rather than having to connect to every blockchain specifically. See what I mean about Cosmos being Grand Central Station? The hubs are important because it’s within these hubs that the Cosmos token ATOM plays its economic role as a proof-of-stake token.

The first hub launched in the Cosmos Network was the Cosmos Hub. This is a public proof-of-stake blockchain whose native staking token is called the ATOM, and it is where transaction fees are payable in multiple tokens.

The ability to utilise ATOM tokens as staking tokens is a significant reason why I believe that as the Cosmos hub expands and blockchains “plug in”, the importance and value of the project may increase.

Another feature of Cosmos is the ability to stake the tokens, earning more ATOM tokens as a reward for delegating to the blockchain validators.

Over time, the “IBC” gang, all different crypto that are built connecting to the IBC protocols or with the Cosmos software development kit (SDK), have been growing in scale and value. At the core of it all is Cosmos. As this IBC ecosystem expands, I think that Cosmos rates highly as another crypto set to ride the next bull market higher.

#4 top-rated crypto for 2024: Dogecoin (DOGE)

Look at the image below…

Source: X.com screenshot

Source: X.com screenshot

It’s a screenshot of Elon Musk’s Twitter profile.

What do you see on it? What do you notice?

There are a couple of things worth pointing out. First is the space theme – very clearly, he loves the work he’s doing with SpaceX. Second is that the weblink on his profile points to X.com.

We know, and have known for some time, that Elon has been keen to build and develop his idea of an “everything app” that he calls “X”.

As I said in an edition of Fortune & Freedom on 19 April 2023:

Elon Musk admitted that he’d stepped down as CEO of Twitter. In his place, he’d appointed his Shiba Inu dog, “Floki”, as Twitter’s new CEO.

Sometime before this interview, Elon had even posted a picture of Floki at the helm. You can see that here.

If you’ve been in crypto longer than a minute, you’ll know that the Shiba Inu dog is popular in crypto circles due to its representation in the “Much Wow” meme.

Subsequently, Doge (as a popular meme) became the inspiration for the Dogecoin cryptocurrency when it launched in 2013. Dogecoin was originally launched as a joke. But as of its market peak in 2021, Dogecoin had a circulating “market cap” of US$85 billion.

A big part of this has been due to Elon’s love of a meme, silliness and subsequently Dogecoin. This has more recently culminated in the series of tweets about his dog, Floki, and even saw the Twitter logo online changed for a period to the Doge…

Here’s where it sometimes pays to embrace the silliness and be a little stupid. In the 2021 crypto boom and bust cycle, not only did Dogecoin hit all-time highs, but a spate of other “dog coin”-related crypto also hit the market.

One was the Shiba Inu crypto, another the Floki crypto and more recently a whole host of “CEO” Doge-related crypto.

Right now, you may be thinking, “Holy Moses, this guy is flat-out bonkers.” And maybe so. But at the same time, massive money was and has been made in these “Doge crypto” for those who did embrace the craziness and took a punt that Elon would continue his love affair with the Doge world.

Therein lies the point about the crypto market being like no other. Elon’s love of his dog, Doge and just being silly can put a crypto portfolio into a healthy profit position.

Considering Elon’s grand plans to make an “everything app” he’s referred to as “X” that could integrate Twitter, payments and crypto, there’s a pretty good argument for some Doge-related crypto in the mix.

This is important because this year, Elon officially rebranded Twitter to “X”.

The domain X.com points back to Twitter.com, but the company, the platform, is now just X.

This is another step towards Elon’s “everything app” – and I think that the next step will be the integration of peer-to-peer money transfers, payments and remittance.

Imagine if X.com becomes the world’s largest money remittance and transfer service. I believe he will make it free to send money to anyone, anywhere in the world. How he subsidises that with the traditional financial system is anyone’s guess.

But there’s also something else to note. Something relating to Elon’s Twitter profile and to that piece I wrote in April.

Look closer at his profile. What do you really see?

Right in the middle there, next to the location icon, is the “X” logo – and it’s followed by a strange-looking capital D.

That’s the symbol for Dogecoin.

Here’s what I expect: Elon is going to make Dogecoin the primary cryptocurrency in the X app. He might integrate bitcoin, but I’m of the view that he will integrate Dogecoin.

If he does, as a crypto bull market gets firing, then Dogecoin is another highly rated crypto that could shoot higher.

Bear in mind, though, that Dogecoin, while a pillar of crypto for a decade now, was originally a joke. And as much as Elon loves DOGE, there’s also a good chance that he’s more pragmatic when it comes to integrating payments and crypto into X and the “everything app”.

For a start, he may just go with traditional payments first and crypto integration may be years away. But all these things aside, Dogecoin tends to pump in a bull market anyway, but now with some billionaire friends in the background, it’s another highly rated crypto primed for the next bull market.

What else we’ve been looking at this month

James:

BYD makes huge bet on sodium for electric vehicles (EVs)

Back in May, I wrote about the potential of sodium-ion batteries, declaring that they hit “the holy trinity of being affordable, feasible and scalable”.

“Analysts have been slow to realise that sodium-ion is different, but it is emerging from the pack as the next best alternative to lithium for EV batteries,” I declared, noting that sodium – found in rock salts and brines around the globe – is cheaper and far more abundant than lithium.

Well, sodium-ion batteries have continued to play catch up with their lithium-ion peers.

At the end of November, Chinese EV maker BYD – the biggest EV manufacturer in the world – announced it was investing $1.4 billion into a 30 GWh sodium-ion gigafactory in China. That’s big enough to make around 1 million sodium-ion EVs a year. The announcement was more or less ignored by the mainstream press, but you can read more about it here.

I am personally very confident that sodium-ion will be 50% of the Chinese EV market by 2030!

An “extremely rare” stock market signal points to record highs in 2024

The stock market is likely to see record highs in early 2024 after an “extremely rare” signal just flashed.

That’s according to Carson Group Chief Market Strategist Ryan Detrick, who highlighted in a 7 December note that more than 60% of all components in the S&P 500 recently hit a new 20-day high.

This runs counter to the idea that mega-cap tech companies are driving the bulk of the gains in the stock market, he says:

Last week, we saw a very rare breadth thrust, which suggested many stocks were surging, which tends to be a signal of impending strength,” Detrick said. “This is extremely rare and showed a lot of buying has taken place recently, not just in a few large stocks.

Analysts observed that since 1972, this rare signal has flashed 15 times, not counting the latest signal. The S&P 500 was higher a year later, 100% of the time after the signal flashed, generating an average return of 18%.

If a similar gain occurs over the next year, the S&P 500 would trade at just above 5,400, up from around 4,720 at the time of writing.

Noting that the S&P 500 hasn’t hit a record high since January 2, 2022, nearly two years ago, Detrick said he expects a record high to be hit in early 2024, and if that happens, it would be one more bullish signal.

This is certainly extremely positive for investors, though it’s worth stating that longer-term signals aren’t normally based on just 20 days of price action, however rare they might be.

What’s more, while Detrick questions the premise that mega-cap tech companies are driving the bulk of the gains in the stock market, it’s also true that Big Tech is still leading year-to-date, up around 50%, while the Dow Jones Industrial Average is up less than 10%.

My take? The signal that Detrick bases his prediction on is short-term bullish, for certain, but for 2024? We’ll see!

The state of play of the EV industry

In recent months, lots of headlines have been written about how EV demand is faltering, yet is it really? The data definitely doesn’t support this – at least not yet.

According to BloombergNEF’s Zero-Emission Vehicles Factbook, global EV sales are actually on pace for a record year, heading for around 14 million sold, up 36% from 2022. In the US, where most of the concerns about demand have been raised, sales are growing even faster and will be up 50% this year.

Although sales might be short of what some manufacturers were hoping for, most industries would be very happy with this kind of growth rate.

What’s more, according to the factbook, pure-play EV automakers now account for 7% of global vehicle sales. A slowdown could still be coming, of course, but for now, it seems we’re seeing a winnowing down of who is actually competitive in the market than any general drop-off in demand.

(Or, to put it another way, the supposed “slow-down” in EV sales is really shorthand for “not actually slowing down, but incumbent car manufacturers being out-competed by new entrants”.)

Elsewhere in the factbook, you’ll find over 70 charts summarising the state of the EV market, covering everything you need to know about where the world is on the journey to cleaning up road transport. Enjoy!

Sam:

Zuck’s $100 million compound

I mean, if I were a multi-billionaire, I’d probably have a sprawling $100 million compound too. In fact, show me a billionaire who doesn’t have one. And if I had one near the beach, I’d have a massive bunker too. Why? Well, I currently live near the ocean. And I’ve already planned out my “tsunami” route if the event ever takes place. If I had a $100 million house right smack bang in the wake of a tsunami, if one should ever hit, I’d rather just pop into the bunker until things settle down, rather than make it for the hills. So frankly, everything Zuckerberg has at this compound makes perfect sense, really.

I can foresee the HBO future

Only a few weeks ago, I was writing at my artificial intelligence (AI)-specific free Substack about how the Y2K dramas of the late 20th century were weirdly similar to the AI revolution taking place now. Unbelievably, it seems that HBO had been working away on a whole new documentary on Y2K. And judging by this trailer, it’s going to be fantastic, wild and funny. I can’t wait for the whole show, but until then, check out the trailer.

The dark gold rush